Dear Esteemed Community Members,

I am excited to share my portfolio with this admired community, eager to receive your valuable feedback and insights. While my early investing endeavours may not have yielded significant success, I skilfully harnessed some profit opportunities that arose during the unprecedented Covid pandemic.

It was fortuitous timing that one of my closest friends introduced me to this forum shortly before the outbreak of Covid. Since then, this platform has proven to be an invaluable resource in shaping my investment approach and bolstering my decision-making process. The collective wisdom and expertise shared by the members here have played a pivotal role in refining my investment strategies.

With great enthusiasm, I now submit my portfolio for your review. I invite you all to engage in high-quality discussions, sharing your observations and providing constructive comments. Your expertise and perspectives are instrumental in fostering an environment of growth and refinement.

Furthermore, I aspire to make my own humble contribution to this community. I am eager to share my insights and knowledge, believing that collaboration and knowledge exchange are the catalysts for individual and collective advancement.

As I eagerly await your feedback and engage in meaningful discussions, I extend my sincere gratitude for your time and consideration.

With warm regards,

Investment rationale are as follows:

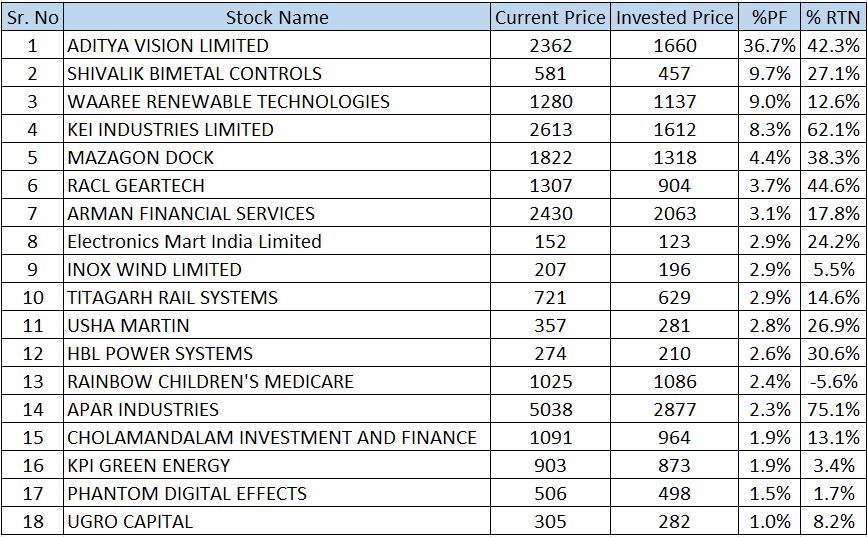

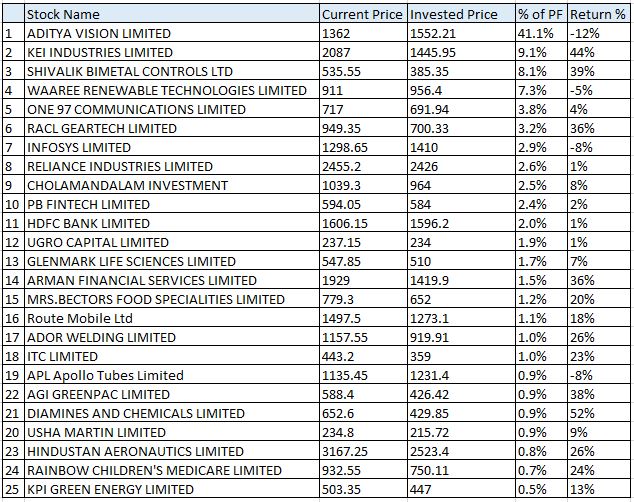

ADITYA VISION LIMITED:

The company aims to increase its store count to 150 by 2025, with the current number of stores at 105. They have opened 5 stores in the current fiscal year (as of May 2023). They expect a minimum growth of 20%, although historically they have achieved growth rates of 27-28%. The poor sales in March 2023 and the impact of higher taxes due to the changed tax system (IND AS) affected their performance in Q4 of that year.

KEI INDUSTRIES LIMITED:

KEI is a debt-free company experiencing a projected 16-17% growth in the next few years, primarily driven by a strong momentum in cable demand. There is expected demand in real estate, the solar industry, and other central government infrastructure projects. The export and brownfield capex in their Silvasa plant will contribute to a 17-18% growth rate.

SHIVALIK BIMETAL CONTROLS LTD:

The company is expanding in the global market due to changes in demand. They operate in three segments, with EbitDA ranging from 22-25% in two sectors and 9-10% in one sector. Currently, their capacity utilization is at 35%. The company expects similar and sustainable growth in the future. They face no domestic competition in the shunt side segment, but there are competitors in the international market. In the medium term, the company believes their current margins are sustainable, and they anticipate further growth with increased volume. Sales Potential post expansion may grow up to INR 1,600 Crores.

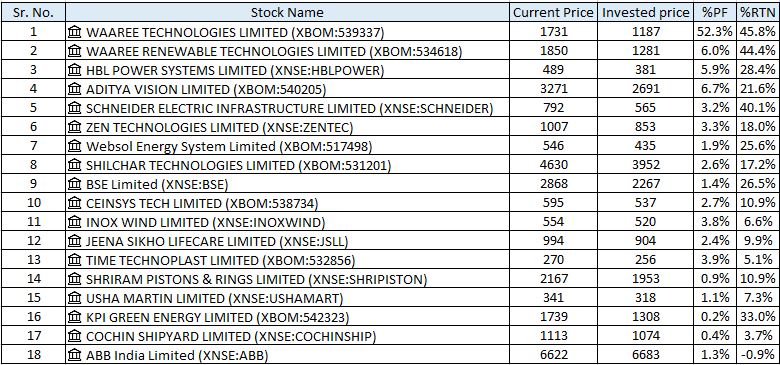

WAAREE RENEWABLE TECHNOLOGIES LIMITED:

According to Hitesh Doshi, founder of the Waaree group, the revenue is expected to grow from 6,821 to 21,000 within 2-3 years, which represents a significant increase.

ONE 97 COMMUNICATIONS LIMITED:

The company also experienced growth in its loan distribution, indicating the success of its lending services. Furthermore, Paytm’s commerce business gained momentum during this period, contributing to its overall revenue growth.

RACL GEARTECH LIMITED:

Company provides guidance for the next two years, with a benchmark growth rate of 20-25% based on past organic growth. It’s has very strong management.

INFOSYS /Reliance:

I have already invested in many small caps. Investing in these companies will provide me base. I expect even it falls, it will come back. Doing SIP with small amount per month.

CHOLAMANDALAM INVESTMENT AND FINANCE COMPANY LIMITED:

It’s from one of most ethical group. Price of this stock can be 800-1600 in few years based on bull and bear case. It is 68% into vehicle finance.

PB FINTECH LIMITED:

They have given guidance for a PAT of ₹1,000 crores in the financial year 2026-'27. While the company expects a normal seasonality pattern, they anticipate a larger drop in savings due to tax changes. They are optimistic about achieving a positive PAT in the current year and expects the same for the next year.

HDFC BANK LIMITED:

This stock fits on principle “purchase and hold for long term”. HDFC Bank has consistently shown strong performance in terms of credit growth, maintaining a stable asset quality, and achieving superior return ratios even during various credit cycles.

UGRO CAPITAL LIMITED:

FY24 should be completely free of any abnormal tax, and they’re expecting around 200-220 Cr. of PBT in FY24. PBT for 2023,2022,2021 are 84,20,12 respectively. My thesis in Ugro is that it’s quite cheap for the business model that they’ve built, and in my view, it is as cheap today as RACL and Shivalik were in the past. If they can execute and prove themselves on asset quality, if RBI continues to have a favourable view towards co-lending, and there isn’t a black swan event in MSME lending, a business that can generate 5% RoA at scale shouldn’t trade at book value. The thesis suggests that the business’s Return on Equity (RoE) will increase to 18% in the next two years due to previous hard work. With expertise in multiple sectors, the business could potentially trade at a market capitalization of 5000 Cr, offering a chance to earn 2-3 times the investment in around two years.

GLENMARK LIFE SCIENCES LIMITED:

The company has a positive outlook for the next few years, expecting to achieve growth of 15% or more. For the next year, they have provided guidance of 12-14% growth. The management has visibility into the company’s performance for the next two quarters and aims to maintain Operating Profit Margins (OPM) around 33%.

ARMAN FINANCIAL SERVICES LIMITED:

Good set of results in last few quarters. They target to grow 25-40% in AUM. They have immense opportunities due to government’s emphasis

on rural and semi-rural India.

ADOR WELDING LIMITED:

Results for March 2023 looks good. EPS is 16.58 compared to 9.70 for same quarter in last year. Yearly results are also good.

APL Apollo Tubes Limited:

December and March quarter could be good for us. Primary vision of Sanjay Gupta is to raise it to 5 million by 2025; the second vision is how can they go to 10 million tons in 2030.

AGI GREENPAC LIMITED:

The company supplies glass bottles to various industries, including alcohol and medicine. Management has set a growth target of 15% to 18% for the next financial year. The company’s net debt is approximately 500 crores with 700 crores in debt and 250 crore in cash reserves. They have acquired Hindustan Glass, which is valued at 3000 crores. However, they need to invest 500-700 crore in capital expenditures (capex) for this acquisition. It will take 6-9 months for the company to break even with Hindustan Glass.

KPI GREEN ENERGY LIMITED:

It’s in business of solar power generation. As per Q4FY23 concall, they are expecting 50-60 % top line growth at least next 2 years.

I request @hitesh2710 @sinha124 @vikas_sinha and other community members to review. Thanks in advance for your effort.