I made a list of the stock I’m interested in and I track them with a google sheet

Company

CMP

Industry

Today’s FY

Target Year

Target Metric

Profit/Ebidta/Sales/Book value in Target year

Target Multiple

Exp Market Cap

CAGR

FLUOROCHEM

3231

Chemicals

2023.7

2025

P/E

1300

35

45500

21.1%

ANGELONE

3253

NBFC

2023.7

2027

P/E

2500

25

62500

28.5%

TANLA

1091

IT Services

2023.7

2025

P/E

650

25

16250

8.1%

DEEPAKFERT

658

Chemicals

2023.7

2026

EV/EBIDTA

2900

8

23200

38.9%

So bassed on this kind of list I see where I can get most return in CAGR terms and invest accordingly. So, wherever I allocate more where the odds are in my favor. In addition to this I follow a few more things

Reduce the weightage where drawdowns could be bigger

Keep allocation to each sector less than 20% (Chemical and Agrochem is still less than 20%)

Exit gradually where the risk reward is diminished or keep stoploss. (exited Angelone and MCX partially because of this reason)

Follow what my mind says in addition to the numbers in the sheet

IT and ER&D:

I pay lot of attention to valuations and PEG. So, I didn’t find many good bets in IT cos here. All the big IT cos are trading at >25x PE for grwoth of 10-20% and same for ER&D. So, didn’t invest much in IT cos

Cigniti tech is an IT co which is still available at 17x P/E and I’ve invested here a few months ago

Mold Tech Technologies is in Engineering services work and supports customers mostly in NA. So, you can say I have some weightage to this ER&D co

From both these cos I expect >20% CAGR revenue and profit growth and found the valuations attractive at my buying price and even at current price

Auto Anc:

Mayur Uniquoters is the only Auto Anc in my PF

Chemical cos:

As I’ve mentioned already I pay attention to the price I pay. IMO chemical cos are at good valuation and the drawdown would be very small from here. In fact after very bad results in recent quarterls the stock prices didn’t fall much. I expect the cycle to return to normal atleast in next 3 years and with the earning improvement and valuation rerating I expect to double the money in next 2-3 years. Shortly better Risk reward

Total no, of stocks held: 107

This is the total no. of stocks I see when I look at the Combined (Realized and unrealized P&L for the year). This includes all the stocks that I held atleast for one day including the stock carried forward from CY2022 and stocks that I’m carrying forward to CY24. This number is looking high and I should control the no. of stocks I trade in and out of so as to reduce churn and charges. I’ve subscried a smallcase and also participated in multiple buybacks/OFS which may have added ~30 to this number. Else this number could’ve been around 70, which is not too good either. I would consider it a win if I could keep this no. below 70 for CY2024

Winners: 67

Losers: 40

Total sum of Win/Total Sum of Loss: 7. This is a result of the whole year being good for the smallcap index. The Profit and Loss includes the unrealized Profit and loss existing at the end of last FY. So, all the profit can’t be attributed to the current year and same goes for the loss.

XIRR: 82%

Biggest Losers and Assessment in abs terms:

Stock

Assessment

NAZARA

Averaged down during fall from peak in 2022

PPLPHARMA

Though it’s cheap after listing post demerger. Kept averaging and didn’t hold it through recovery

SOUTHBANK

Sold when the CEO resigned.

MOLDTECH

10-15% loss. Still holding. See good prospects

SYMPHONY

Bought for buyback. Mistake in judgement.

AGSTRA

Uncertainity on profitability and lack of conviction

IGPL

10-15% loss in % wise. Eventhough the plan was to hold till the cycle turns upward. But couldn’t hold as I got swayed away by better opportunities

KAMAHOLD6

Small loss in % terms. Still holding for recovery in Chem cycle

STAR

Lack of conviction and inability to understand the pharma cycle

ALLCARGO

sold with stoploss. Could’ve given + ve returns if held. No regret

Biggest Winners in abs terms

Stock

Assessment

ANGELONE

Bought during lows of Mar23 at criminal undervaluation

REDTAPE

Value creation with demerger. Still holding

PITTIENG

Bought at lows of the cycle in Mar 23

KERNEX-T

Bought at lows of the cycle in Mar 23. Holding for TCAS orders

UJJIVAN

Bought during lows of Mar23. Cycle played out

XPROINDIA

Bought at lows of the cycle in Mar 23. Plan to hold till Fy27-28 for Capex to come live

EQUITASBNK

Bought at lows of cycle

KRSNAA

Held though CY22 and added in FY23. Holding as I expect earnings to improve

MCX

Low Risk and High uncertianity regd the New trading platform

PDSL

Bought 3 months ago. Strong business model and management

NIITMTS

Demerger opportunity

GOODLUCK

Bought when Pref issue was done at ~600 rs. Not holding

CIGNITITEC

One of the cheapest IT cos with good growth guidance. But Prom selling

Most of the ideas came from twitter and some from VP. Thanks to Sahil sharma, SOIC Finance, Chinmay (chins) and VP community. I have made my own study in limited capability to invest in these cos

Observations:

BIggest winners came where starting valuations are cheap along with improvement in earnings (Angelone, Ujjivan, Equitas, Pitti, Krsnaa)

Biggest learnings came where I didn’t respect the valuation like Nazara tech, Symphony. Some other reasons are cyclicality of earnign and my inability to hold the stocks through. So I should either limit my allocation where the it’s difficult to predict (Chemicals, Pharma, cyclicals) or should have the discipline/gut to hold the stocks through the recovey in earnings/stock price. After all I believe the best returns could be made in cyclicals

Evaluate more cos to improve returns. Take more ideas from twitter, VP and do own research to make better returns.

Areas to improve:

Allocate higher where I could predict the earnings (difficult to do so in Chem, Pharma etc.). Undervaluation to start and growth in earnings are the key for good returns

If allocated to cyclicals buy during bottom of cycle or at the start of upcycle and hold till the cycle recovers

Evaluate more opportunities to find better opportunities and make better returns. Currently most of these ideas are coming from twitter and VP. Could use some technical screener to find opportunities to start with

There’s no substitute for hard work. Work hard and smartly. Spend time where it matters

Readings for CY2023:

Read Buffet Partnership Letters

Spent significant time on VP reading. Started writing as well. Long way to go

Joined a Whatsapp group with like minded people (based out of pune). Have people to discuss ideas

Targets for next years (CY2024):

Read Berkshire Hathaway Letter to shareholders (ongoing)

Read Bulls Bear and other Beasts

Read Masterclass with Super investors

Read Secrets from profiteering from bull and bear markets

Look at the charts posted by Chartist and VVV on twitter. Learn and improve the understanding of technicals

Start sharing thoughts and learnings on twitter. Helps to network with people and work better

Targets for Tracking Universe and Portfolio:

Reduce the no. of holdings in the PF to close to or below 20

Alreadyb have a list of cos I track and have estimates on earnings and fair P/E or P/B multiple for most of the tracking universe. Cross check the estimates against the actual results when after the target time frame (Fy25, Fy26 etc.)

Evaluate and participate in short term opportuniteis llike OFS, Buyback etc… (started in early 2023 had fair success)

Maintain better returns over Nifty smallcap 250 index

Create a Paper trading momentum portfolio as a combination of technical and fundamentals or either of them (Create one technical based recently. Need to keep working and improving)

Learn and implement technical based exit system for portfolio stocks. Could have helped with Angelone, MCX etc

Writing this post helped me make some observations on my PF and investment process. I believe this would help me understand the areas where I need to improve, Make plan for improvement with set targets and hold myself accountable for future progress

I recommend fellow VPers to consider writing a similar post, Learn and grow

Thanks for reading

Praveen

Disc: Have/had positions in almost all the cos mentioned. No reco to buy or sell

Portfolio Update:

Currently I’m writing the updates on my PF as and when I can without any specific frequency. But now onwards I’ll try to update this topic on 1st day of each month. This is would help me later to go look at my PF at a particular time and assess how it could’ve played out if I didn’t change weightage of any co.

It’s possible that not many people appreciate the presence of high churn in the PF and so the update on PF would be unnecessary. But in my case as I’m still learning I may have high churn. Also, I mostly add and exit stocks in a gradual way, so making the weights in the PF to have consistent small change instead of sudden big changes. The top 5-7 constituents always remains the same as I take view of few years (2-3 years)

Coming to the point now, this is how my current portfolio look as of today

Instrument

Weight

XPROINDIA

8.0%

FINOPB

7.3%

PDSL

7.1%

KRSNAA

6.9%

MAYURUNIQ

6.5%

KERNEX-BE

6.4%

CIGNITITEC

5.4%

REDTAPE

5.3%

KAMAHOLD

5.0%

MOLDTECH

4.5%

DCMSRIND

4.1%

VISHNU

3.8%

SHREEPUSHK

3.7%

MCX

3.4%

MTARTECH

3.3%

ANGELONE

3.0%

SAIL

3.0%

CONFIPET

2.4%

DEEPAKFERT

2.2%

ULTRAMAR

1.9%

LAURUSLABS

1.7%

SBCL

1.5%

SHARDACROP

1.4%

GLS

0.9%

AARTIDRUGS

0.8%

AMBIKCO

0.5%

WIPRO

0.1%

Few actions that I plan to take soon:

Partially or Fully exit MTAR tech. In past few weeks, the promoters of the co have been selling heavily in the open market making me nervous and I feel that the upcoming quarter results and the guidance for FY25 would be not so good. So, I plan to exit this co and allocate somewhere else

Participate in Buybacks: I see decent opportunities in ongoing buybacks with a possibility to make 5-10% profit (buyback profits are not taxed to the investor, the co pays) in 2.5 to 3 months which is decent considering the market valuation

Raise allocation to DCM Shriram Ind: I see opportunity to make good returns here with ongoing demerger which may take 1.5 to 2 years to conclude. I would be comfortable increasing my allocation from current ~4% to bit higher and upto 8% if I see good correction or any positive developments in the business ( If I find any)

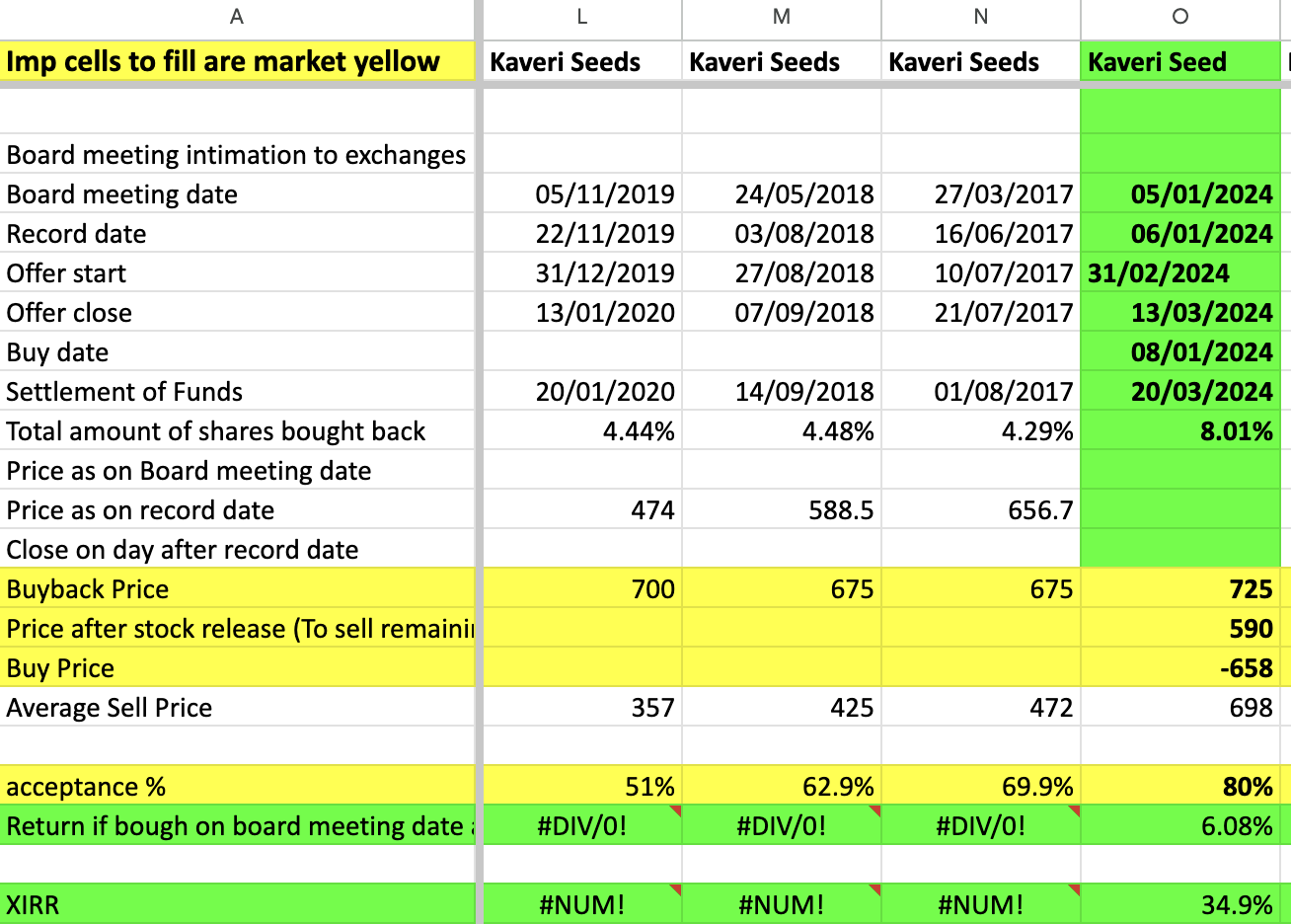

The column marked in green is my estimates and already available data for current buyback. Other 3 columns contain the data for previous buybacks

Observations:

For last 3 years the co bought back ~4% equity shares and the buyback premium varied between 4% to 50% (price as of record date)

For current year the co is buying back upto 8% and the buyback premium from CMP is ~10% which is not too attractive.

So, I expect to get 80 to 100% expectance in this buyback and that would mean 6-10% returns in 2.5 to 3 months, which is pretty decent. Also, here I’m assuming that I sell the unaccepted shares in open market at 590 Rs (10% below CMP)

Hope this example helps.

Disc: Please don’t take any action based solely on this data. This is just for illustration and learning purpose. I plan to take position and participate in this buyback

The data mentioined may have inaccuricies and I also made some assumptions to arrive at my thesis

Added Mufti (Credo Brands): Trading at 20x P/E and seemed like a good opportunity in Fashion and apparel space. Industry growth is in double digits and the management expects to double the sales in 4-5 years. There is chance for operating leverage. Anti thesis: Need to see if the margins could sustain above 30%

Added NHPC: Bought via OFS as the allotment was below then CMP. Stock price has good momentum and so holding half the quantity of the allocation and sold the other half. No strong fundamental view expect that the power sector sees tailwinds in near future . Holding as there’s good momentum

Sold ANGELONE after the results (~3400 rs) as I see the margin pressure could continue in near future. May turn out to be a bad decision for me, but won’t regret

Added small qty of Kaveri Seed Co. Ltd (KSCL) to participate in buyback as I see opportunity to make 6-8% in 2-3 months for small shareholders (investment < 2 lakhs)

Added small qty of DCMSRIND as I see value unlocking coming out of demerger… Expected timeline of 2 years (may take more time depending on NCLT hearings and postponements)

Please feel free to share your views or ask questions on my PF or any of the cos mentioned

Great to see you adding this. I am also tracking this company since its IPO. The low valuation and a very decent looking Management attracts me here. But why would someone value their company at a good discount to listed players in such a roaring bull run? This has been stopping me from entering this company. I could not find much to read about the company either. Any theses you have to add?

I think it’s valued same as peers like cantabil retail, TCNS clothing killer and other brands (excluding retailers like pantaloons, etc). For whatever reason, the stock didn’t do well at listing.

I’ve looked at this as an opportunity instead of worrying about why it’s not priced higher at IPO and didn’t list with good premium.

Anti thesis :

Margin improvement from 10% to 33%. Margins may or may not be sustainable

Wage hikes for lbaour could hit gross margin and so ebidta and profit margins

These are the only major risk I could see

Other risks could be not growing in 14-15% but as the industry is growing in this rate. This growth rates are within reach

Thesis:

Not a asset heavy business, as the manufacturing is outsourced

Operating leverage will play out as Same store sales growth continues

Valuation rerating upwards is a major part of investment thesis for me (in addition to 14-16% growth and operating leverage)

Moldtech is into Infra Eng services business. Most of their clientele is from USA and Eu. Currently due to high interest rates, the business is going through headwinds. However I consider this a good opportunity to buy. Few things that may work in favor of the business

Reduction of interest rates in US in near future

Acquistion is expected sooner than later. The acquisition will help the co. move up the value chain and enter into the high margin business of design

Inherent low cost humanforce advantage of the co, as it serves clientele in developed countried from India

Corporate governance is good (same management as Moldtech packaging)

Mechanical Engineering Services is expected to contribute to the growth whereas historically most of the revenues came from Civil Eng Services

These are the few qualitative thesis points, I have in mind. For management guidance on growth of Revenue and Profit, you can refer to the recent concalls

Thanks Praveen for an elaborate answer. Those pointers matches with my thesis as well. I started learning about engg services sector recently but couldn’t find listed competitors. If you have it please do share. A P2P analysis would also give a perspective of sector trend

I don’t think there are any comparable listed competitors.

The management gave KPIT as one of the peers. But, it’d be futile to take it as a fair comparison.

Valuation wise we may value them on par smallcap IT cos. But, the growth rate has been good with operating leverage playing and would do so in future. So, may be 20-30x P/ E depending on general market conditions.

@praveen_potnuru KPIT majorly focusses on Automotive software and it’s definitely not a peer to Mold tech.

TAAL deals with Engg design services and one vertical of Axiscades also focussess on mechanical design. Don’t you think these are comparable peers to Mold tech?

Hi Hemanth.

Not sure about TAAL.

Coming to axiscades: Axiscades is well diversified and does more value added work. What Moldtek Tech does is plain Vanilla work in Just stuructural Eng (CIvil and Construction). The Mechanical Eng Division of Moldtek is relatively better (IMO) but still a long way to go. So, overall I don’t think Moldtek is as good as Axiscades but the growth rates have been good in recent past and the management indication that they are closing in on an acquisition (mentioned in Q2 concall) is a step in right direction. In addition to this, seasoned management (proven track record in Moldtech pack) and good addressable (global) market with Cost advantage (working out of India) forms my thesis.

As per Q3 concall managment commentary, they were asked by clients to serve them in Press tool

The co is moving into Press Tool, Dies, Wiring Harnesses etc. So, they have onboarded some employees to increase the capabilities. This would be the thing to watch out for in near future

I’ll check TAAL and keep an eye on axiscades as well.

Hi Ram

There could be multiple reasons for MUFTI to fall.

Momentum: The co has so many shareholders who has bought in IPO and they may be going out of patience and selling the stock. I have seen the same thing happen earlier in newly listed IPOs

Fundamental Reasons: Whole industry (look at peers like Arvind has seen good margins and profits in recent quarters. While this may seem good, We could be at top of the earning cycle (peak margins).

Since the co. is recently listed, The financial figures are avaialble only for last 3 years and so growth has been good as we came out of COVID

My thesis:

Managment commentary suggesting the co cold double revenue in 5 years (14% CAGR)

I expected some rerating in P/E multiple combined with Pofit growth (bcz of Operating leverage)

Currently I don’t know how things could turn out from here. But if the co can keep growing at 10-15% the downside could be limited. Currently trading at 15x P/E. But not sure E (earnings) are normal or one off

Portfolio update for month of March 2024. I couldn’t update this earlier in the month to some business travel.

This is how my current PF looks

Company

Weight

XPROINDIA

8.3%

FINOPB

7.8%

MAYURUNIQ

7.1%

PDSL

6.9%

REDTAPE

6.9%

KERNEX

6.6%

KRSNAA

6.2%

DCMSRIND

5.7%

MOLDTECH

5.4%

KAMAHOLD

4.5%

SAIL

4.1%

NSE:MCX

4.0%

Vishnu

3.4%

Shreepushk

3.2%

CONFIPET

2.7%

ULTRAMAR 506685

2.5%

LAURUSLABS

2.2%

SHARDACROP

2.2%

DEEPAKFERT

2.2%

MUFTI

1.5%

NHPC

1.5%

SBCL

1.4%

KSCL

1.4%

AARTIDRUGS

0.8%

EKC

0.8%

AMBIKCO

0.4%

WIPRO

0.1%

GRWRHITECH

0.0%

Changes:

There are no major changes in the PF this time. The recent fall in market has impacted the PF. The fall was not worrisome. I’ve added ~2% of PF value (used cash to buy the dip).

Added some qty of Modltech technologies, Fino PB to the portfolio

Participated in buyback of KSCL which gave ~6-7 % returns in 1-2 months time. 67% was the acceptance and that amount to available as cash to buy other stocks.

Confusion: Most of the PF stocks have corrected significantly in this fall. But some of them held strong. Which means, some of the stocks have become better valued and some of them are showing strength (Kama holding, Laurus labs, Mayur Uniq). This makes it difficult to decide what to buy

My top picks to buy currently:

Krsnaa diagnostics

Moldtech tech

Sharda cropchem

PDSL

Ultra Marin pigments

These are based on 2-4 years view point.

Thanks for reading. Please feel free to quiz me on any of my Portfolio cos or suggest any improvements needed in PF or my thesis

While this may be true, there’s no way to confirm that.

In addition to this, the earning performance needs to be tracked.

In Q3 Fy24, the management said that the drop in PAT because of increase in marketing expense ~8cr. This may also mean that the co. has cut down costs just before IPO to inflate the profit. So, we need to wait and watch how the earnings pan out in next few quarters.

Currently no plan to buy or sell. I may decide based on future earnings or price action or If I find any trigger

I also have added mufti in my radar because I like its clothes, mostly jeans.

All my jeans are of Mufti.

I have few questions.

Have you visited mufti showrooms?

Do you like mufti clothes?

How would you explain their revenue growth in recent years?

Any comparative studies that you have done with other companies terms of footfalls or average revenue per store?

Any comments on managements?