I am new to ValuePickr and Donald has encouraged me to participate in the community from where I have learned a lot in the last few weeks. I thought what better place to start then putting my holdings and investment rationale for everyone’s review. I appreciate your time and consideration and looking forward to learning from you all.

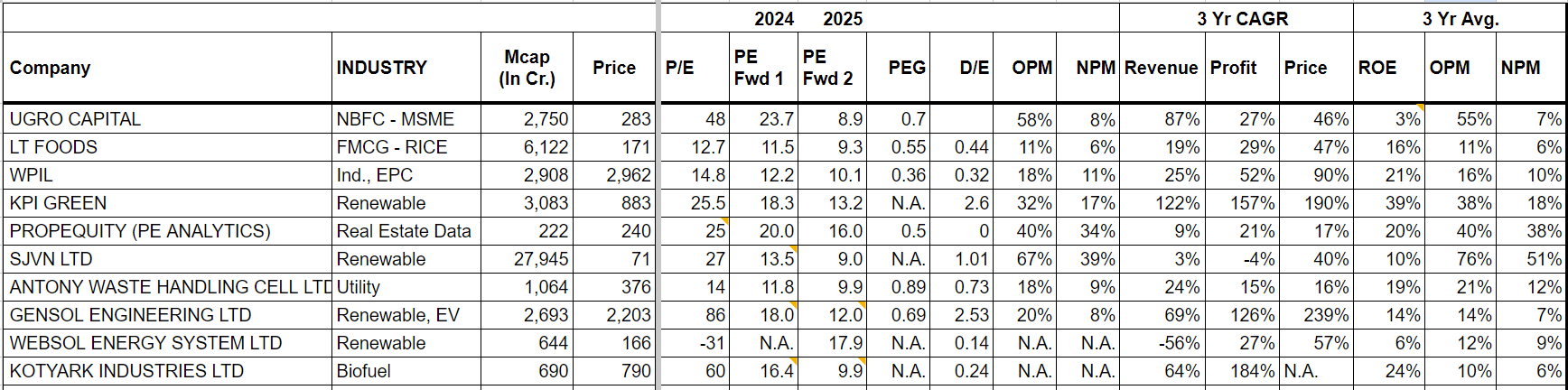

Here is a summary of my portfolio and investment rationale follows the summary table:

Cashflow based MSME Lending (INR 85 Trn Credit Gap; only 20% formal credit availability),

Fintech: AI based Digital Underwriting to allow significant scaling at minimal incremental costs

Co-Lending Space (push from RBI)

Available today at <2x of Book Value vs 4x for most NBFCs with stable metrics

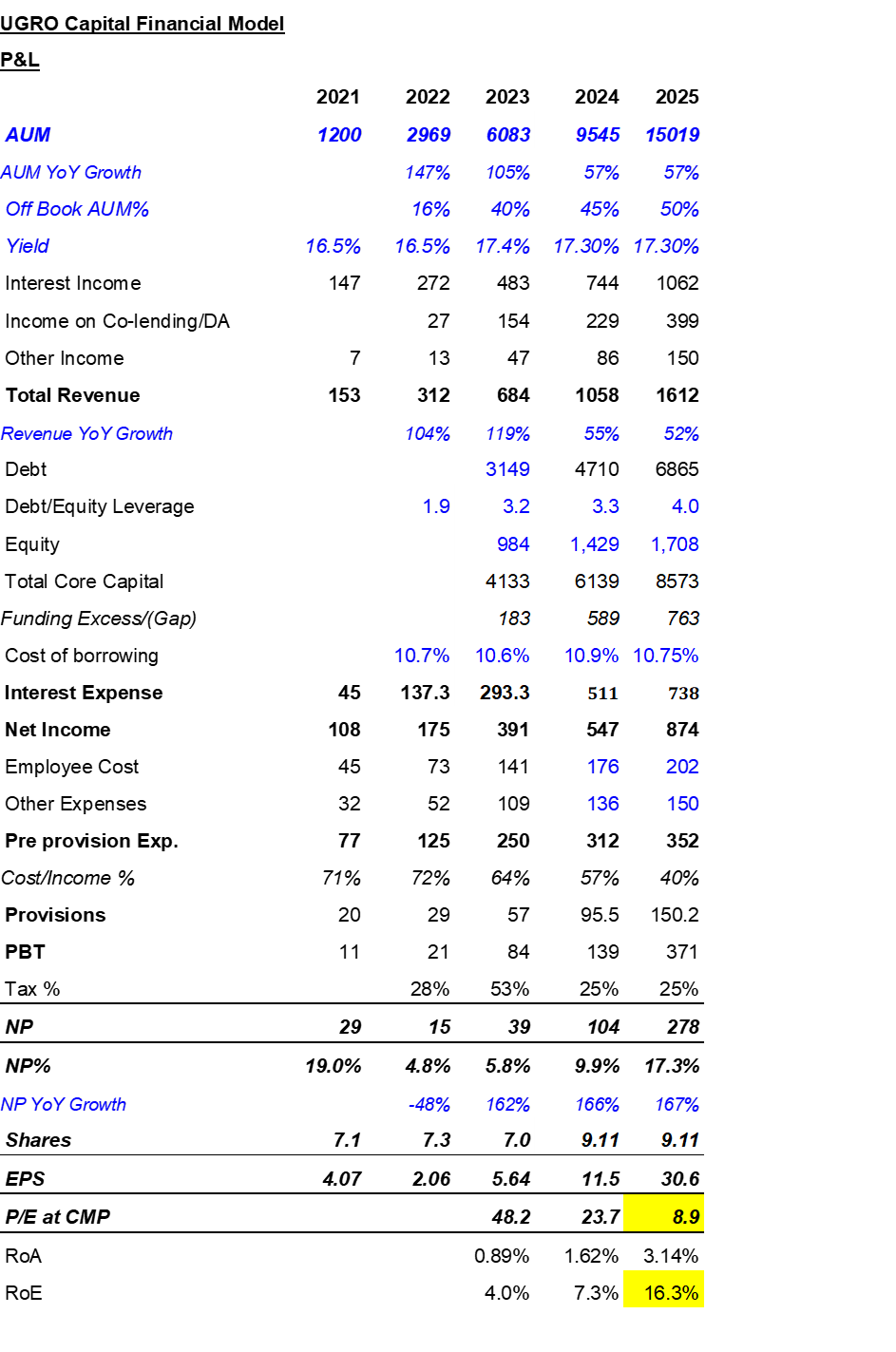

Re-rating expected from significant improvements in financial metrics. AUM should cross INR10,000cr/INR16,000–17,000cr in FY24/FY25 (50% off the Balance Sheet). The management is targeting a RoA of 3.1%/4.5% and a RoE of 10%/18% in FY24/FY25.

Enjoys leadership position in the market of Basmati Rice (India MS @29% and America @ 50%); continuously Gaining Market Share

Multiple optionalities (Organic food, Convenience food, Middle East Market)

Strategic partnership with kingdom of Saudi Arabia - The Middle East has the largest basmati rice consuming population as it accounts for almost 80% of total basmati consumption worldwide

Higher disposable income in India to boost consumption of premium rice

Management’s Target ROE/ROCE 20%/23% for 2025

At PE of 12 with annual PAT growth of 30%

WPIL –

WPIL is engaged in the entire value chain of Pumps & Pumping Systems from concept to commissioning and execution of water supply projects on a turnkey basis for industrial units, power utilities, irrigation departments

Government Push (Jal Jeevan, Amrut), 2.5 year earnings visibility, Order book capped due to execution match principle

Co. has developed new products for the navy and is looking positive for good growth in the short-medium term

PE< 15 with 3-year sales growth of 25%, PAT growth of 52%, and 21% ROE

KPI Green –

Company provides solar power, both as an independent power producer (IPP) and Engineering, Procurement, Construction (EPC) services to Captive Power producers(CPP) customers.

Capacity Energized since inception till H1FY24: 346+MW. Business in Pipeline: 541+MW. Seems ahead of 1000MW target by 2025

Two big orders recently: 240 MW under GUVNL tender and 145 MW from Ayana Renewable Power Four Pvt Ltd

Promoter target of annuity income per day at 1cr by 2027

PropEquity/ P.E. Analytics –

PropEquity is the largest and most comprehensive Online Real Estate Data & Analytics Platform covering Residential/Commercial/Retail/Hospitality

Added 52 new clients in subscription business, highest since inception of the company, increasing to 180 net clients

Entered Valuation Business - Clients increased from 8 to 35 clients (Banks, HFCs and NBFCs)

Huge potential to grow in this segment from lower base. Current MCap of 225cr (~30% in cash)

SJVN Ltd. –

SJVN is targeting a operative capacity of 5,857 MW by FY24 which is 2.4x of the current operational capacity

Has a shared vision of 25,000 MW by 2030 which is already locked-in in terms of identified projects

Antony Waste Handling –

2nd largest domestic player. Various initiatives taken by government like Swachh Bharat Mission, to keep India clean and focusing on hygiene has led to a multifold increase in the spending on solid waste management by various municipal corporations.

Revenue growth for FY24 is expected to be around 18% in core operations. Anticipates EBITDA margins of 23% to 25% going forward.

Waste-to-energy plant in Pimpri-Chinchwad inaugurated by the Honorable Prime Minister in Aug’23, generating revenue of INR65 crores annually.

Bid for a large C&T contract in North India and bio-mining tenders in South India, expecting positive outcomes.

Possibility of transport ministry finalising policy for using municipal waste in road construction

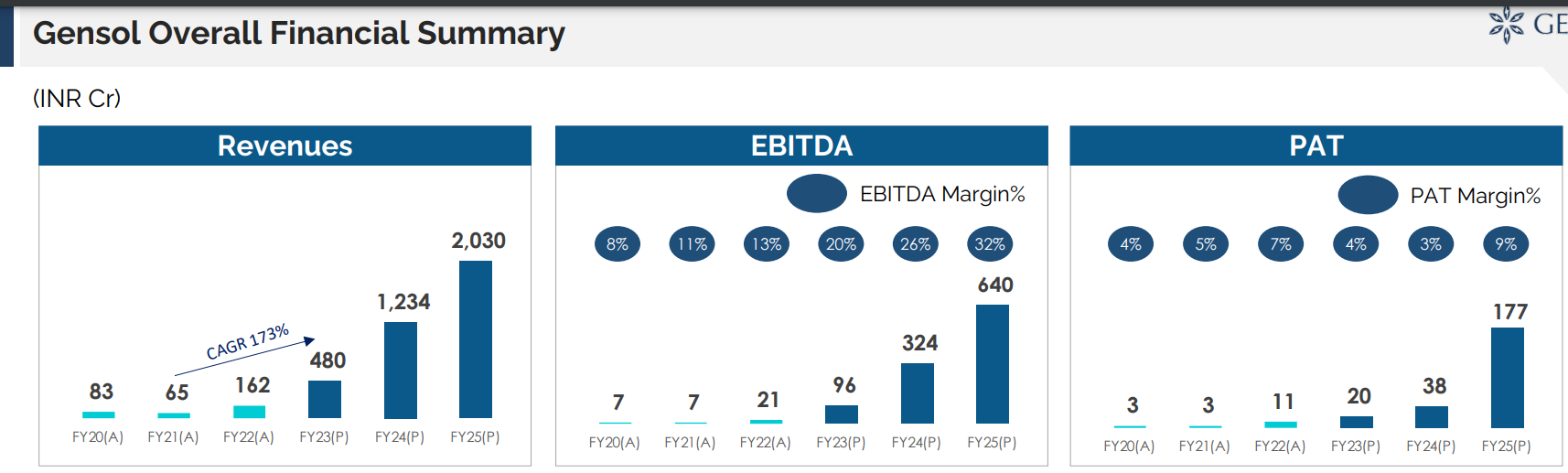

Gensol Engineering –

Solar Business – 1500 (minimum) to 2000 crore revenue for FY 2023-24. Trading at ~1.5 Mcap/Sales multiple of Solar business

EV and EV leasing business optionality. EV production to commence in 30 days with first 8 month supply to group company Blu-Smart

2024-2025 potential: EV Segment revenue potential of 2000 cr with 2 shifts in 2024 (if successful). 400cr revenue from EV leasing business. Solar EPC could be another 2000 cr. revenue if minimal YoY growth assumed.

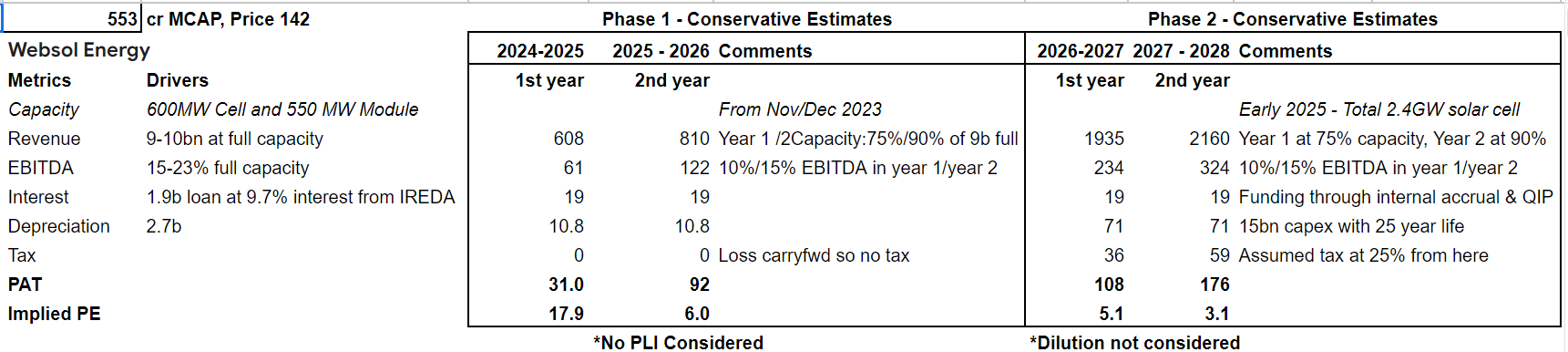

Websol Energy –

Discontinued solar cell and module manufacturing on old tech (FY 23 impacted) and now launching capacity of 600 MW cells and 550 MW modules (go live in Q3 2023) with latest technology. Phase 2 of expansion will take solar cell capacity to 2.4 GW.

Preferential infusion by promoter at INR 112 for Phase 1

Revenue at full capacity for Phase 1; 900-1000 crore with 15-23% EBITDA;

The government of India has set a target of blending 5% biodiesel with diesel. This is likely to lead to a significant increase in demand for biodiesel in the country.

Last year capacity utilization was at 8%. 10X Revenue potential in short time horizon.

Been awarded 194 cr order for Q1 FY24. Has been awarded another tender in Q3 for supply of Bio Diesel for the period of October 2023 to September 2024 having estimated order value of Rs. 569 Crores approx. Similar requirement tender by OMC is expected to be released.

Upside from Glycerin plant and Carbon credit

Of course there is a lot more analysis and research behind all these stocks but wanted to keep it concise here. VP threads have been very helpful to research and analyze these stocks as well. Thanks again!

List of interesting companies you have in your portfolio but it seems like your portfolio is too much in to power/energy sector. Don’t you see it as a risk or you have investment in some other asset to hedge your investments.

I would rather diversify into few more companies into consumer durable, ems, chemical sector etc.

Thanks Mohit. Yes, I do have other asset exposure for diversification. Exposure to renewable energy stocks is by design to capture the growth India is looking at in achieving a target of 365 gigawatts (GW) of installed solar capacity by 2031-32 from 67 GW in April 2023.

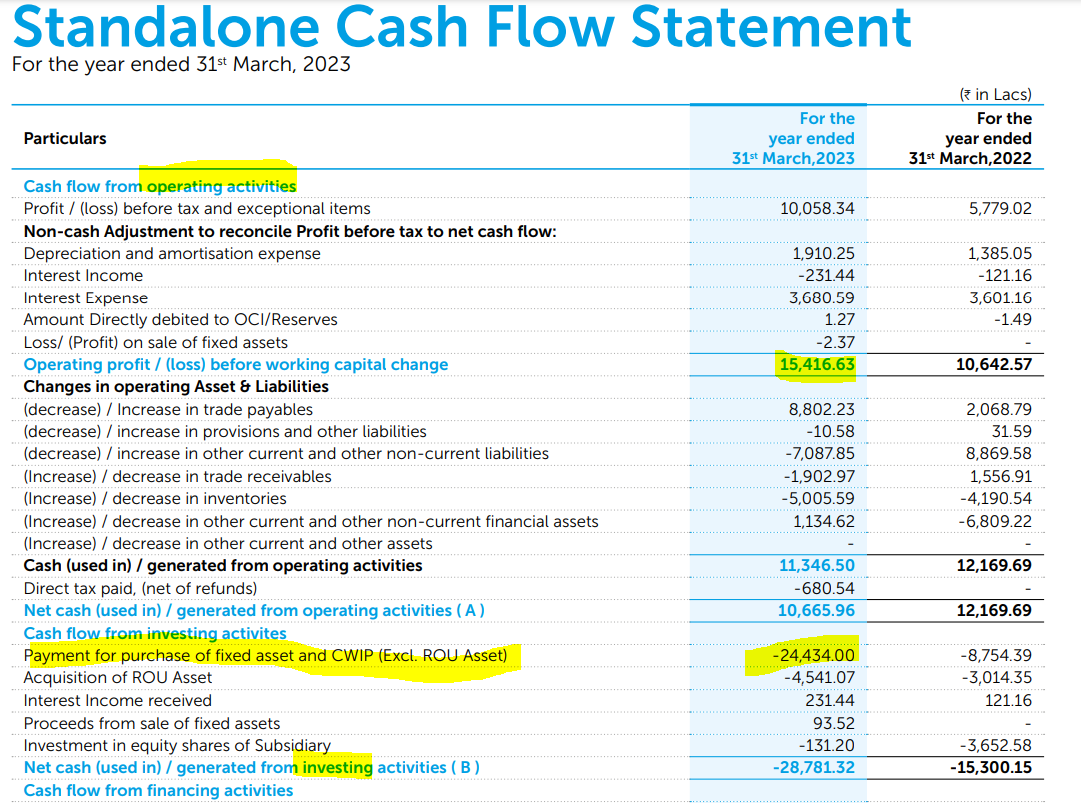

Hi Pratik , I am not pro into valuation but do have some basic knowledge. I have posted one query in KPI Green energy thread that company Free Cash flow has been negative since last 5 years. I like the sales and profit they making but just because negative free cash flow I would like to monitor it further. Also no guidance on that given by management. I am also not sure if I am over concern about FCF.

They have positive operating cash flows. They are investing in IPPs which is causing the cash out flow. IPP is high margin but capital intensive portfolio. Not too worried about it as these IPPs have long term contracts providing annual income. Let me know if you still have any questions on this.

This is really good to see. So the Cash flow is going back into re-investments. Your information looks far better than screener , Where do I can get this information , this will help in better decision making ? thank you sir.

This is directly from KPI’s annual report. Screener also has cashflow broken down between Operating, Investing and Financing, if you scroll below P&L and Balance Sheet. And no “sir” please

Because of low PE , L T food was on my radar list too but I didn’t find any MOAT in the business. It is commodity business and we have have existing players in same business. Margins has been in range of 10-11% from long time. Any rational behind selecting L T food ? asking purely from knowledge perspective only.

Interesting set of companies, Pratik. For Kotyark Industries, what is your take on competition? Given the size of the opportunity, I do not understand why there are not many players making bio-diesel.

As per the investor presentation posted by company. They expect total revenue from all three segments for 2024-2025 at Rs.2,030 Cr. Am I missing something?

Despite that with Rs. 270 projected EPS for FY25, its still is a great buy provided they can deliver. There is a lot that they are trying to chew in my honest opinion

The numbers I have quoted above is based on a recent promoter interview. Revenue from EV segment is not concrete yet and is dependent on them being successful in selling EV closer to 2 shift capacity (commercial production not yet started but close). Revenue from Solar segment seems more or less certain.

Promoter commented that they are market leader and they might have more than 50% market share. He couldn’t comment on why others are not in the business yet. It didn’t seem like there are significant barriers to entry here but they seem to have an early mover advantage as supported by recent orders.

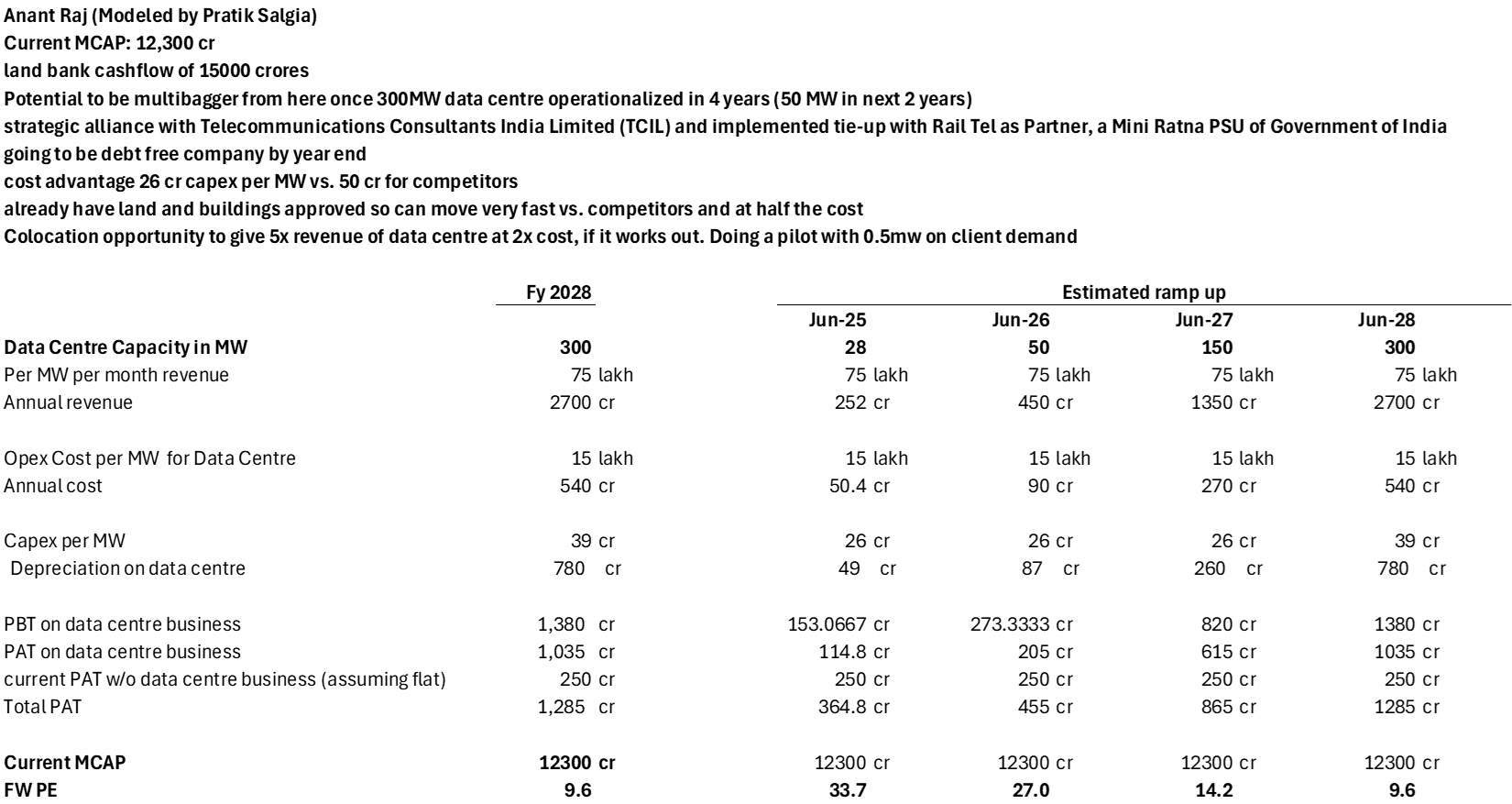

Thanks for this. So assuming that their current business’ PAT remains stagnant, PAT from Data center business alone can go up 9x in the next 4 years. This looks promising. However, could you please clarify a couple of things for me. On the valuations front, when you say current PE of 55 is cheap, are you saying this from a future growth potential perspective or on the basis of comparison with other peers who are in the same business? Secondly, given that it gone up 9x in the last 24 months, how much of this future growth do you reckon is already factored in the current stock price? Thanks.