I think they have a JV with them

1 Like

PPAP Concall Summary:

- Achieving an all-time high in quarterly sales, the company has seen a year-on-year improvement in EBITDA, standing at 9.4% for the standalone and 8.12% for the consolidated level.

- Maruti Suzuki, the company’s largest customer contributing 52% of revenue, experienced its highest monthly sales in September and surpassed the 1 million mark in the first six months of FY 24.

- The growth is attributed to new premium model launches, where PPAP benefits from higher per-car revenue.

- To counter cost increases, the company has passed some onto customers, engaged in discussions about inflationary costs, and implemented internal cost-cutting measures.

- Raw material price inflation significantly impacted margins but is now stabilizing.

- The lithium-ion battery vertical continues to face challenges, affecting overall profitability.

- With a Pan India network of 120 distributors for 700 products in aftermarket services, the company plans to expand internationally.

- The joint venture started making positive contributions in Q2 24.

- Aftermarket business experienced a 50% growth in FY 2024.

- Strong order books for commercial tools are expected to contribute positively this year.

- The company will export industrial products for the first time this year.

- Manufacturing parts for Honda Elevate, the per-car component cost is between Rs. 6000 and Rs. 8000.

- Premium SUV products are in development, with mass production expected in Q4 2024.

- Current capacity utilization is at 80%.

- The company’s products are engine-agnostic, securing business with customers launching electric vehicles.

- Obtaining AIS 156 approvals for two and three-wheelers showcases compliance with automotive industry standards for electric safety.

- The company aims to develop solutions for mobility, including ESS and robotics applications.

Takeaway from Concall: Capacity utilization stands at 80%, tariff revisions are underway, raw material prices are stabilizing, the JV is profitable, a strong order book is in place supplying parts to premium SUVs, contributing to higher per-car contributions and margin increases. Despite robust demand, sustainability requires achieving double-digit EBITDA margins, a target expected to be met this year with further increases in FY 25, a key milestone to monitor.

Disclosure: Have a position in around 220. No recent transactions.No sell buy recomendation.

4 Likes

There tariff revisions are underway since more than a year now. I too am invested from 150-180 levels, it will be almost two years now. Every concall they just keep on saying that this year would be an year of reckoning. According to me it seems there is a lot of competition here. Saurabh Mukherjea took a good call when he exited from this. I think it was around 2018-2019. There are auto Ancillaries like Rane, Varroc who have really displayed remarkable business performance and then there is this. Lets see how it goes.

1 Like

Looking back, the company reached its peak valuation and margin in 2018-2019. Presently, it faces its lowest margin, with raw material costs rising from 50-55% in 2019 to 62% now . A softening in raw material prices might boost the margin to 12-15%, especially given the substantial increase in revenue, indicating customer retention. The current valuation appears cheap, might remain like this unless execution improves on margin front.

2 Likes

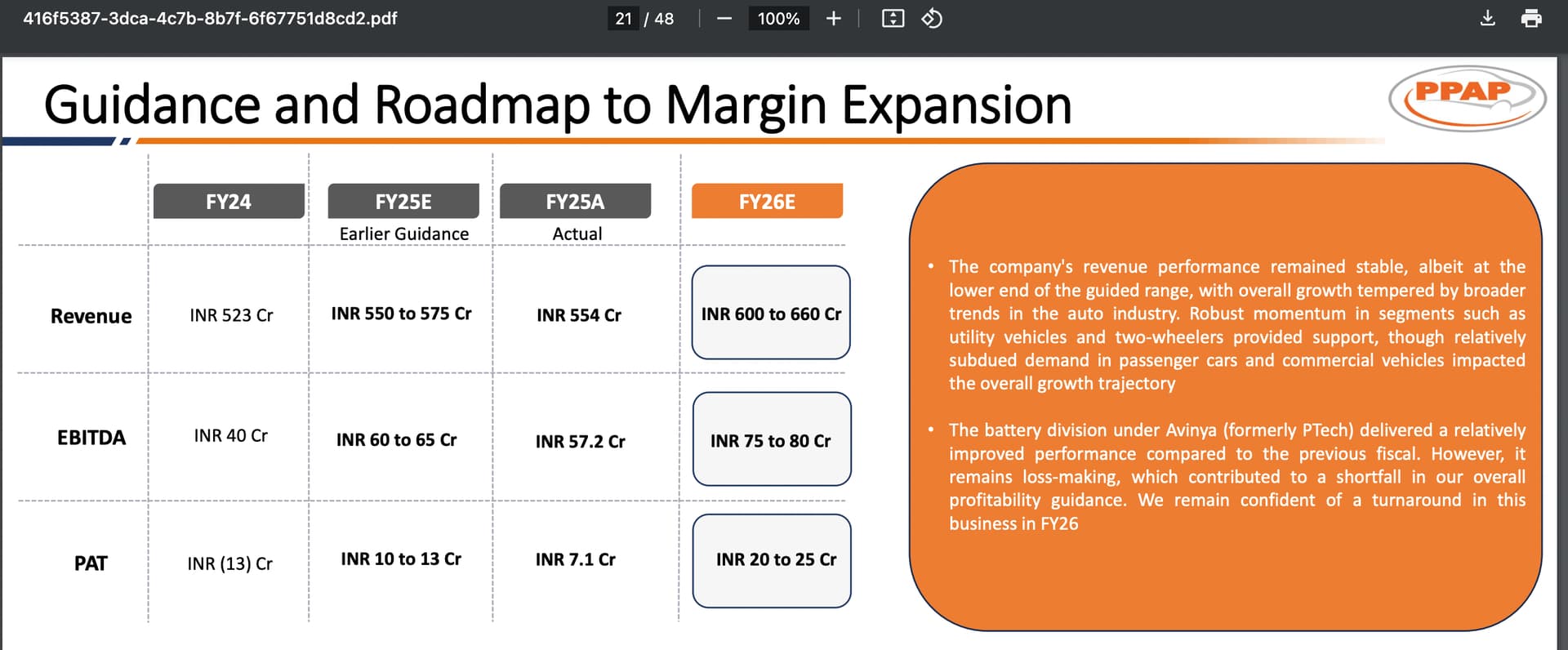

Anyone tracking PPAP closely? What is your view on management guidance from your past experience? The guidance for FY26 is pretty solid compared to the current valuations.

1 Like

PVC prices have more or less bottomed out and are remaining stable. ADD is the key overhang. Also company has rationalized its capex and now is focusing on execution and increasing capacity utilization. Maruti sees increase in small car sales due to GST cut. Company should benefit from it.