Q4FY18 Conf Call Q&A and Notes

Q: What is the Part sales for last Q3FY18

A: Part Sales 87.37Cr, 7.16Cr for Tools

Q: Growth of Part sales is less. Why?

A: Industry growth itself is 5.5%.

Q: Update on Hyundai. Starting to cater to Creta? How much revenue has come in this Qtr

A: Less than 1% to topline - only from EON. Expecting this to grow to 3-4% of revenues with addition of 2 more models.

Q: No CAPEX for FY19?

A: Yes only maintenance CAPEX this year… Mainly for maintenance. Range of 25-30cr. But this may change depending on the customer/new business

Q: Broader thought process on the JV and other collaborations front

A: Aim is for Growth prospects in expanding the existing products. Increase the business per car

Q: Gross margins and EBITA margins sequentially YOY basis has contracted significantly. How much tax is owing to outsourcing costs coming to raw material or how much from increase in actual raw material costs?

A: Tools are contributing significant to raw material costs. Material costs in general have not changed and at 50%.

Q: EBITA Margins at 21.3%. Do we intend to maintain this or will improve this and what will be the levers for it.

A: Can maintain these margins, fairly confident. Headwinds are in terms of crude and currency, which we are watching but not impacting as of now. Also our efforts in improving the efficiency of material utilization will balance any impact from head winds.

Q: How much of raw material imported

A: 25-27%

Q: Some more light on new customer MG Motors OEM. How are we going to supply it from which plant

A: This OEM will launch one model currently. Will be supplied by Gujarat location. Will start with Injection parts, customer has shown interest in ceiling systems as well. We will be supplying around 11 parts for them. Content per car is not finalized as we are still at preliminary drawings.

Q: Status of new plants: Gujarat plant and ramp up of Chennai

A: Gujarat: 2 facilities, one is own and other is rental. Currently supplying to swift from rental plant and plan to move to own. Will be supplying to Baleno as well. End of this year we will be supplying all parts of MSI from this plant.

Revenue guidance from Gujarat plant: Injection business will give 13-14Cr. This number is expected to go up as some more new parts are in discussion

Chennai plant: Currently supplying from Noida to Chennai. First priority is to localize this in Chennai. Hyundai and Kia will be serviced later by this plant as second priority.

Q: Scaleup plan for JV for 2-3 years.

A: Supplying to Toyota Yaris now. Growth is going to be fairly good. Existing infra can meet 100Cr topline target. Utilization at this point at 55-60% and comfortable. Once we reach close to full utilizations we will have similar margins as standalone.

Q: Are you able to pass on the increase in raw material prices to customers?

A: Gross margins has come down due to high tool cost in material cost. On part business, the material cost will remain similar to what it was earlier. In terms of passing the costs to customers, we think we can maintain the same costs by improving the material utilization efficiency (no clear answer)

Q: Employee costs is high compared to similar industry. Why?

A: We are print to build company where the whole activity in taken up in house. Special purpose machines, design team etc - complete integrated player. Also the company has expanded from NCR to PAN India - so employee costs is growing at a higher rate than before… All these factors have resulted in growing employee costs. As our business stabilizes, we expect the rate of growth of employee costs as a percentage of sales should come down

Q: Will the profit growth sustain at 10-15%?

A: As we demonstrated so far, we will continue to grow at a rate higher than industry as business grows.

Other Notes

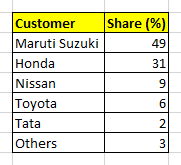

Existing OEMs: Maruti, Honda, Nissan, Toyota, tata, GM, Ford, Mahindra

New additions: Hyundai for EON, MG Motors India (owned by China based Sia Corp)

Segments

Currently in PV Segment

Expanded to : LCV and 2 Wheeler

• LCV: ISUZU, Bharat Benz

• 2 wheeler: Suzuki, Honda

10% of the products are exported by OEM customers

Facilities

Greenfield facility in Gujarat supplying to New Swift& Baleno

New facility in Chennai supplying to Suzuki (target to localize the parts being shipped from Nodia)

PTI (JV Company) - shown growth of 33.8% in FY18 - Sealing products

Open to Inorganic expansion to de-risk the business - Suzuki 2 wheeler is an example

Official SIAM Industry Figures

FY18 numbers of overall market

• 5.5% YOY increase in PV vehicles

• 10.2% YOY increase in CV

• 16.1% YOY increase in 2 wheeler

FY19 forecast - PV grows at 7-9% on back of continuing rural demand

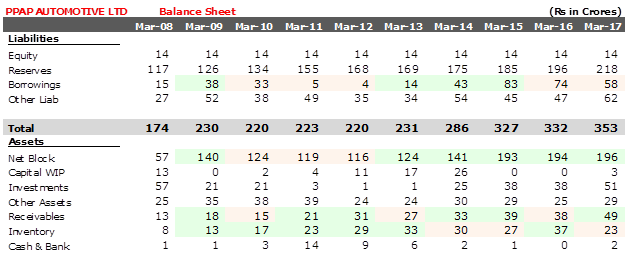

Expansion/Capex Plans

• 75-80% Capacity utilization - room to grow without new CAPEX

• Capex is being met by internal accruals

• 50.75 Cr CAPEX in FY2018. Now new requirement in FY2019

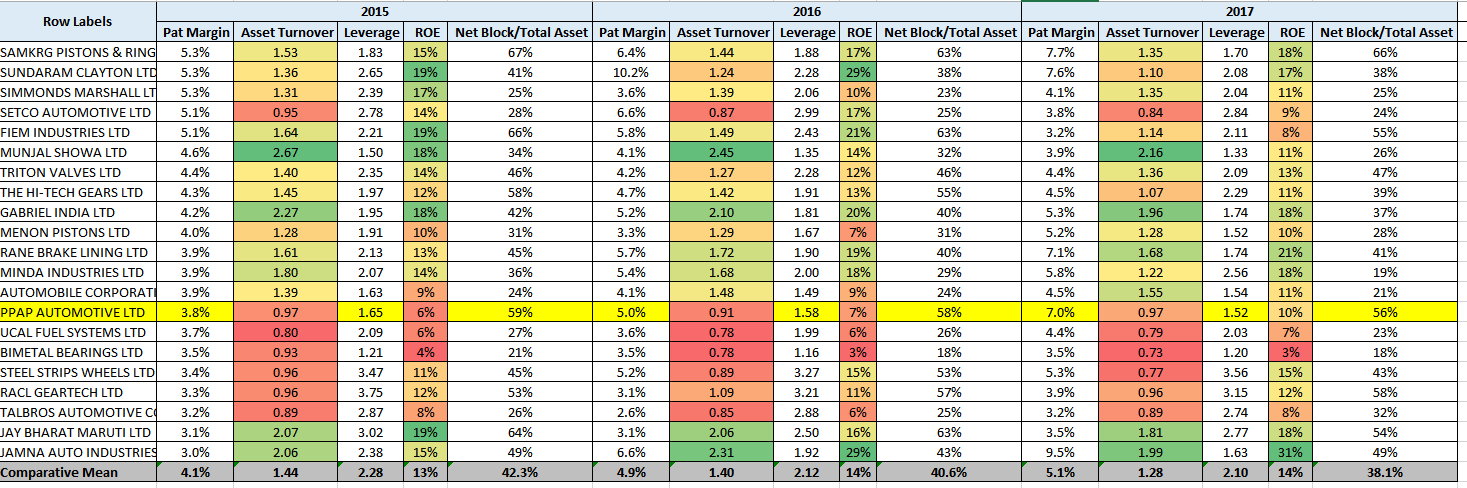

. However, what is your view on key reason behind low ROE? I might have missed something or may have interpreted something wrongly. So, glad to know your views

. However, what is your view on key reason behind low ROE? I might have missed something or may have interpreted something wrongly. So, glad to know your views