I had started looking at this company when it came out with an IPO as I found it to be interesting reading the IPO notes of various brokers, etc.,. But wasn’t able to apply due to liquidity issues.

Disclosure – Finally was able to buy from secondary market post listing. Hence disclosure at the beginning itself that I am invested in Power Mech Projects.

Purpose of the IPO was to provide Motilal Oswal PE and exit and at the same time raising cash to pay debt partially and to utilise rest of the funds for WC requirement.

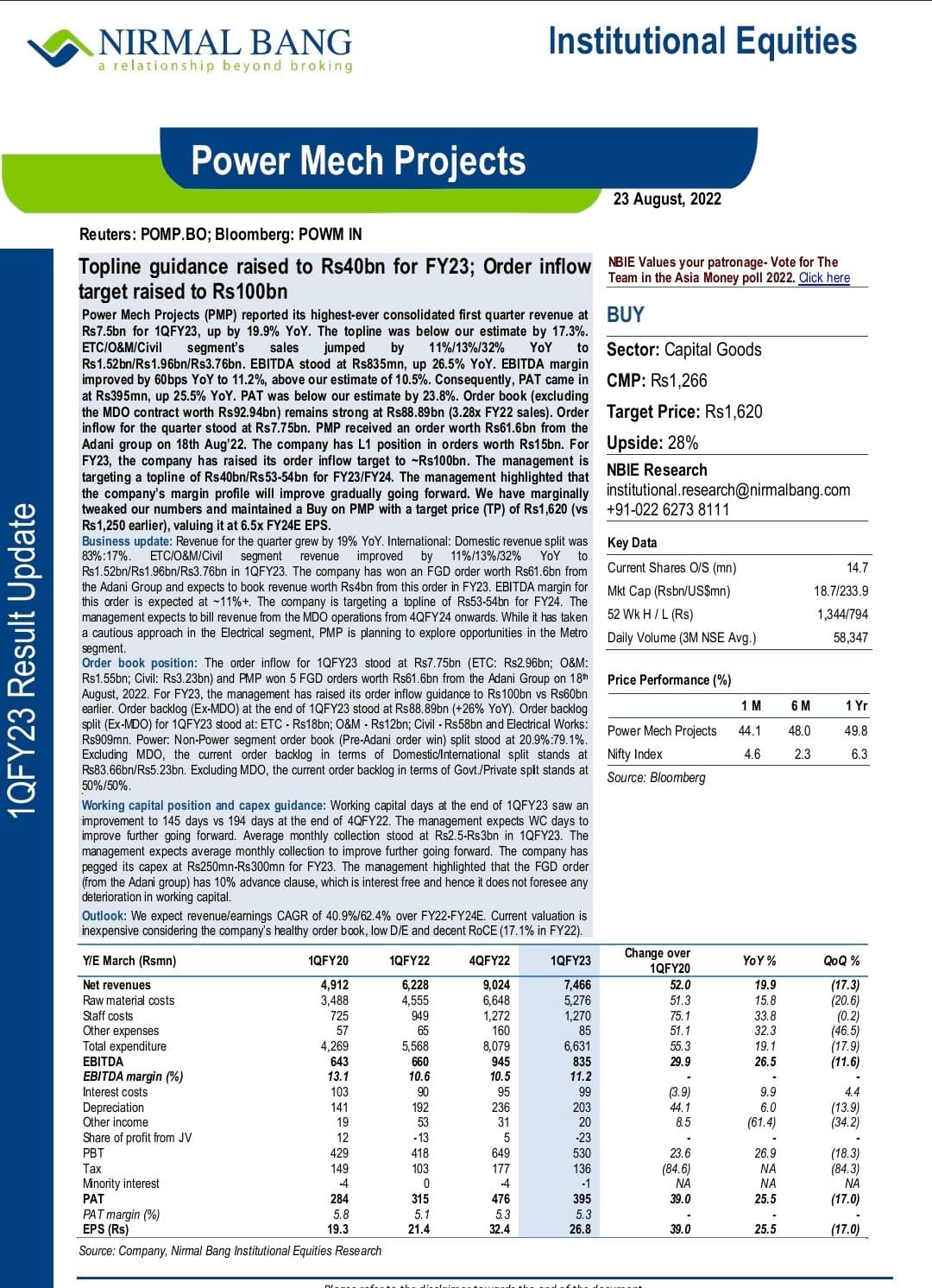

Luckily Nirmal bang also started covering this stock and has come up with a detailed report on the same (can be found here). I am utilising excerpts from Nirmal Bang report to provide a brief summary on the stock.

CMP – Rs. 607.

Current Mkt.Cap.- Rs.890 Crs.

FY16 Rev. Expected – Rs.1600 crs. (as per mgmt.)

Promoter Stake- 64.5%

Company Url.- http://www.powermechprojects.in/

Company-

The first step of setting up a plant is the most arduous for any power company. It requires intense engineering expertise which is often in short supply—and also proves expensive to acquire and retain. The simpler option is to outsource the heavy-lifting: Enter Power Mech Projects, a Hyderabad-based company, which spotted this opportunity back in 1999.

Power Mech Projects (PMP) is an integrated power infrastructure services company providing below services to power plants which are nothing but the business segments that Power Mech. operates in:

- Erection, testing and commissioning (ETC) of BTG and BoP equipment (67% of FY15 revenue) - ETC work is provided to thermal, gas and combined cycle power projects covering BTG packages including various types of boilers (HRSG, WHRB, CFBC), turbine generators, electrostatic precipitators (ESPs), hydro turbines, structures, pressure parts, air systems, fuel oil systems, coal systems and BoP packages including structural steel works, ash handling, coal handling, fuel oil systems, water treatment plants, fire protection systems and high-pressure piping works.

- Civil works (13% of FY15 revenue) - civil, structural and construction works which are ancillary to its ETC business.

- Operations & maintenance (O&M) (20% FY15 of revenue) - AMC, repairs, renovation and modernisation, residual life assessment, scheduled shutdowns, retro-fits, overhauling, maintenance and upgradation services for thermal power plants, hydro power plants and gas turbines.

In 2013, it built, tested and commissioned projects for a cumulative capacity of 40,000 MW across India. It also erected 65 boilers and 80 turbines during the period. And, in the process, it crossed Rs. 1,000 crore in revenues for the first time.

Few Clients-

BHEL, NTPC Limited, Doosan Power Systems India Private Limited, Adani Power Limited, L&T Ltd-Thermal Power Plant Construction BU, Thermal Powertech Corporation India Limited, GE Power Services (India) Private Limited, CLP India Private Limited, BGR Energy Systems Limited, Thermax Engineering Construction Co. Limited, SEW Infrastructure Limited, KSK – Arasmeta Captive Power Company Limited, KSK - VS Lignite Power Private Limited, KSK –Mahanadi Power Company Limited, Abir Infrastructure Private Limited, Siemens Limited and Reliance Infrastructure Limited.

Promoter-

- First generation entrepreneur, Mr. S Kishore Babu.

- Spent the first 14 years of his career in an engineering company, Indwell Construction.

- Rose up the company’s ranks to additional managing director and, later, to joint MD. At this point decided to branch out on his own.

- Driving force behind Indwell Construction’s success, built strong associations with NTPC and BHEL during his stay at Indwell; hence thought why not venture on his own, rather then doing it for somebody else.

- Tapped into his extensive network and founded Power MeCH.

- Has leveraged his personal touch and execution skills to gain contracts from several large power producers in India.

- Colleagues describe him as someone who is relationship-oriented.

Salient Features-

- Largest and most credible ETC company – 38% market share while in the highly profitable O&M business (19% margin) it holds a 60% market share in private IPPs.

2.Worked on 16 out of 21 super-critical plants in India as well as both operational UMPPs. - Gets 1 out of every 2.5/3 orders from NTPC and BHEL.

Some Financials and Ratios-

- OPMs – 12%

- ROCE - 24%

- ROE – 22%

- P/Bv. – 2 times

- Asset turnover – 4 times

- Receivables – 52 days (industry avg. 92 days)

Future Opportunities-

- Revival of stuck IPPs worth 57GW.

- Servicing of Chinese plants (60GW capacity in India) through a joint venture with a Chinese firm.

- Opening up of state utilities to private O&M contractors.

- Focus on increasing share of foreign business. (6% of FY15 revenue and 14% of order book)

- Focus on O&M business which has healthy margins of 19%.

- As per CRISIL, over the next four-year period the opportunity size of AMC services in thermal power sector in India is estimated at Rs75bn. The total opportunity size includes power plants of central utilities like NTPC as well as state power generation companies, which currently do not give out AMC contracts to private parties but prefer to do it themselves.

Threats – (Direct copy paste from the Nirmal Bang report)

- Significant time and cost over-runs in lump-sum price contracts and item rate contracts on account of delay by PMP or its sub-contractors can affect the profitability and working capital cycle.

- PMP’s operations are dependent on a large pool of contract labour and any inability to access adequate contract labour at reasonable costs at project sites across India may adversely affect its business prospects.

- Inability to effectively manage project execution and milestone schedules may lead to project delays, which may adversely affect PMP’s business.

- Any economic downturn or other factors adversely affecting investments in the power sector will adversely impact the demand for PMP’s services.

- Any significant and unforeseen increase in competition can affect the profitability and market share of PMP adversely.

Points I like -

- Have liked what I have been able to read and understand about the promoter. First generation entrepreneur, understands business very well, looks like having an aggressive mindset, has been able to achieve scale in a business where it isn’t easy to attain scalability.

- Company has shown that it can achieve scalability in a difficult business. Future plans also points towards this that scalability can further be achieved.

- Small company and is the market leader.

- Niche segment that requires lot of technical expertise. (creates entry barriers)

- Has maintained decent margins and good return ratios despite being in an industry related to power.

- Has done well at a time where power as a sector hasn’t done well, and I think things for power sector would eventually improve gradually (maybe slowly) as government’s increasing focus on clearing bottlenecks in the power sector, opportunities for service providers should grow. For e.g. visible steps being taken by govt. higher coal production by Coal India in the last few months, reforms in fuel linkages, setting up of railway lines for coal evacuation, and steps taken towards restructuring of distribution companies in some states.

- Good return ratios of the segment it operates in.

- Good WC mgmt. despite being in a stressed sector like power. (should improve further as mgmt… is focussing on O&M business and wants to increase its share to upto 30% in future.)

- Margins should improve with rising contribution of O&M business.

- Annual maintenance contracts should grow due to a rise in installed base of IPPs in recent years.

- PMP is in the process of setting up a large heavy engineering facility in Noida for making non-critical equipment and spare parts to service 60GW Chinese facilities and other equipment like hydro turbines. This reminds me of AIA Engg. Kind of business. I like this as I see this as an extension to O&M services business. Company is already providing O&M services, then why not use spare parts etc.,. manufactured internally. I think that Power Mech’s presence and dominant position in the O&M services business should be an advantage for this new plant.

- This looks like a segment where small players may not find it easy to enter as needs technical expertise & credibility and big players like BTG or BOT guys may not be interested as this segment maybe small from their point of view and also non-core for them.

- Nirmal Bang report states that Chinese and Koreans are competition only in product manufacturing and supply and wouldn’t be able to or wouldn’t be willing to compete in this business segment where Power Mech operates. The report states that Chinese presence may infact translate into business opportunity and not a threat. I see the above JV with a Chinese company as a proof of this that Mgmt. maybe sees this as an opportunity.

Power Mech looks like a play on it getting better valuations and then being driven by improved earnings. There are no like to like comparable players with closest one being Sunil Hitech and BGR Energy Systems. Power Mech seems to be trading at discount to both these Sunil and BGR as it is trading at 10-11 times earnings and at an EV/EBITDA of 4.8 (estimated FY16), whereas BGR trades at 15 times earnings on TTM basis and EV/EBITDA of 8.25 times and Sunil although trades at similar valuations as Power Mech but Power Mech has better return ratios, operating metrics, WC cycle as compared to both BGR and Sunil.

I think Power Mech should trade at 15 times earnings or EV/EBITDA similar to BGR i.e. 8 times.

Hence I have taken a position expecting a re-rating and after that better numbers driving the stock price post re-rating.

P.S. - This is not a buy/sell recommendation. I am an amateur investor and not capable enough to analyse a stock. Above are just my views on Power Mech., which may be biased as I am invested in the stock. Please do your own due diligence.

References-

- Nirmal Bang Report

- Forbes Article

- Other articles and info available on the net