Quick Snapshot

CMP: 85 as of 19th June

Market Cap: 22,439cr

P/E: 2.38

Div Yield: 11.15%

ROE: 22.82%

52 W H-L: 75.15/138.8

History

-1986: Started Business

-1993: MoU with Government of India with the aim of developing the country power sector

-1999: Started consultancy services to both State and Private owned companies

-2005: Entered into MOU with LIC and other 10 private banks for financing of Power Projects

-2015: Incorporated Jharkahnad Infra project and Bihar Mega power as a wholly-owned subsidiary

-2019: PFC acquired majority of the REC which is the second-largest PFC controller by GOI.

Segment

Company has only one segment which is lending loans to power sector companies which are engaged in:

- Construction of Power Plant &

- Generation supply and distribution of electricity.

Note that the company doesn’t have any other geographical segment other than India.

Promoter Holding

- GOI holds 55.99% ownership in this company. GOI has divested its stake in this company from 66.6% at one time in 2018 to 56% currently. It is one of few consistent profit-making PSU which was divested by Government

My personal views on the disinvestment are positive. I believe in disinvestment of PSU because from a company viewpoint :

(i) it helps in improving the efficiencies of such companies when it comes to management policies and productivity as it’s now more governed by professionals instead of bureaucrats ![]() although it can be argued that public sector companies can also appoint professionals so this argument is not valid. However, we all know the efficiencies b/w Public and Private sector in reality esp in the context of India hence my views are biased towards the positive side.

although it can be argued that public sector companies can also appoint professionals so this argument is not valid. However, we all know the efficiencies b/w Public and Private sector in reality esp in the context of India hence my views are biased towards the positive side.

(ii) It helps to attract private foreign investors for JV which is much better than foreign borrowing which PFC is currently doing to fund its loan book.

-

FII holds18.92% as of March-20 which is up from 14-15% in 2018. Its mainly owned by :

Windacre partnership master fund 4.87% and UBS principal capital 3.28% -

DII holds 20.4% mainly by LIC 5.59% and HDFC Trustee company 9.25%

Loan Book

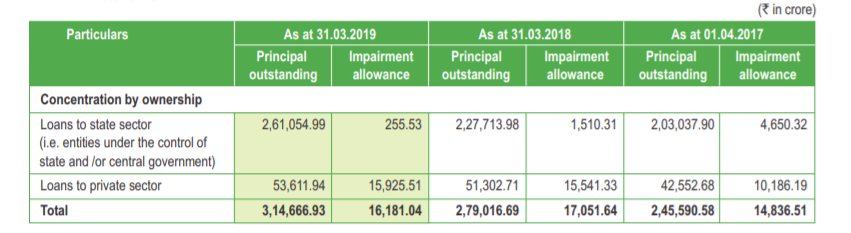

- Company has continued to increase its loan exposure to 3,14,667 cr as of March19 as compared to 2,79,329cr as of March-18 i.e. up by 13%

It has been able to consistently grow its loan book by 10% during the last 5yrs.

-

The cost of the fund has gone down to 7.95% from earlier 8.21% in FY19. This year company has further benefited from it going down due to a low rate.

-

Looking at the annual statement of the company, one can make out that it has a high % of the loan to financial weak state sector companies which do give the risk of NPA however company argument is opposite that its state-backed so won’t default. To me, this is a risk factor in the book given a high concentrated profile of the borrower.

-

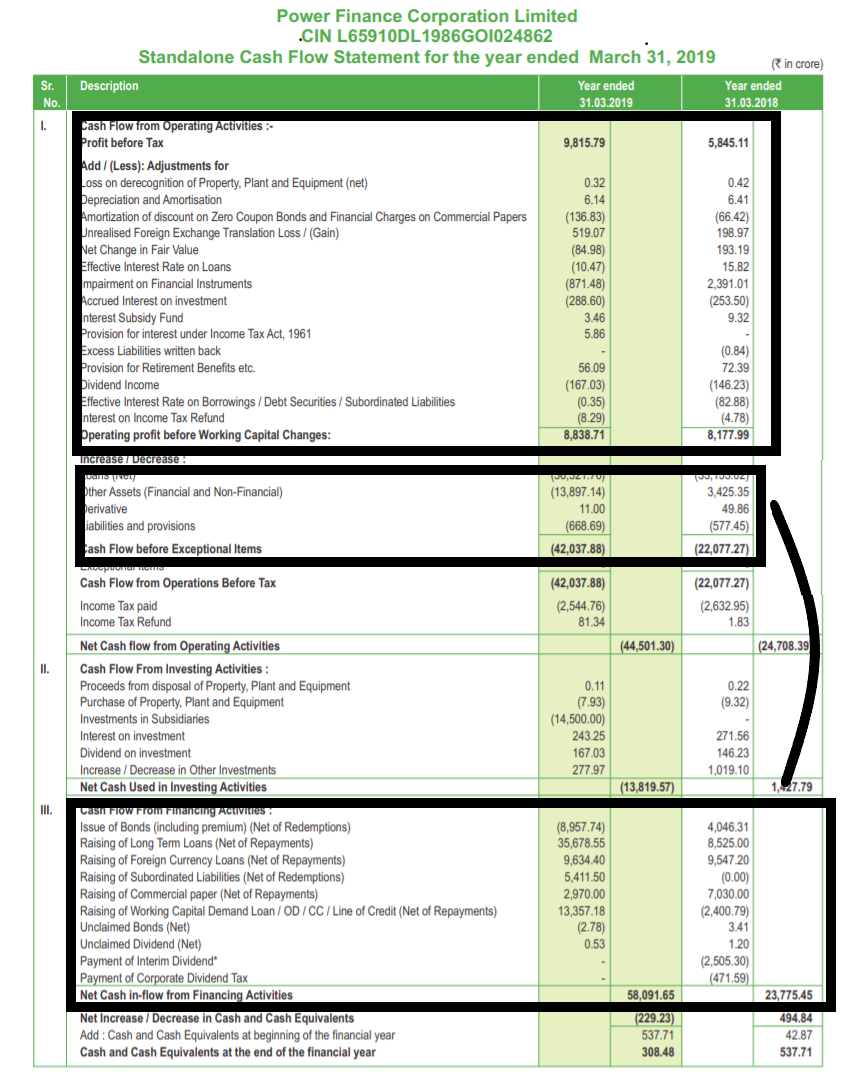

Company loan book growth has been from the borrowing against the internal accrual as we can see from the cash flow of the company.

As we can see below the majority of the investment of the company is funded by external borrowings under CFF as compared to a small percentage being funded by Internal profit actual. This exposes the risk further when GOI holdings say goes below 51%. The cost of borrowing might further increase in that case of the company while its highly concentrated state loan portfolio if gets distress can become a debt trap for the company.- Company loan book growth has been from the borrowing against the internal accrual as we can see from the cash flow of the company.

As we can see below the majority of the investment of the company is funded by external borrowings under CFF as compared to a small percentage being funded by Internal profit actual. This exposes the risk further when GOI holdings say goes below 51%. The cost of borrowing might further increase in that case of the company while its highly concentrated state loan portfolio if gets distress can become a debt trap for the company.

Financials

-

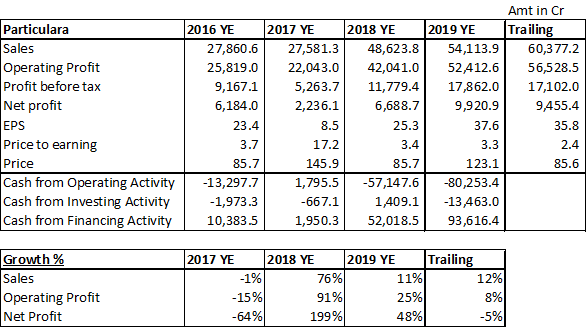

Financial performance has been quite good. It has increased its sales every yeat at a decent rate and its expected to overall report 12% higher sales as compared to 2019

-

Net profit is expected to be down however given the current market price and strong growth in strong growth in Sales and Profit in 2018 and 2019, this year’s profit and Sales don’t look bad. It’s one of the few Profit-making PSU.

Also, note that we can see that Price is at the 2018 Year-end levels currently at 85.7 while EPS, Sales, and Profit has already increased by 50% almost to those levels of FY 2018.

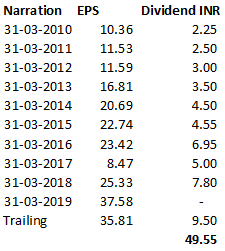

- The company has been a consistent dividend payer and has paid a dividend of Rs 49.55 in the last 10yrs. Given the Price of stock at 85.7, it’s trading at an attractive dividend yield of nearly 11% to its FY20 dividend.

Liquidity

-

As shown above, that company heavily relies on the interest income and refinancing to pay its debt. The current COVID time with 3 months of moratorium doesn’t give that much of comfort at this time.

-

One thing which does separate this entity from all other NBFC is its sovereign ownership which is the main reason to recommend this NBFC. Its a good consistent profit-making PSU and given its backing of GOI, it has the ability to raise funds at short notice when required as it has shown in the past when the situation demands.

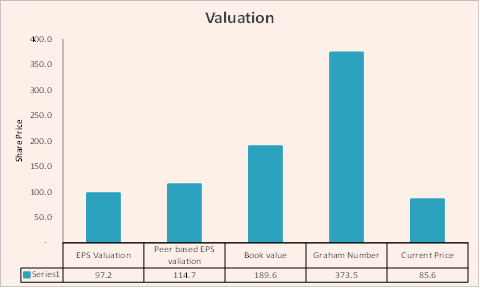

Valuation as per different methods:

Looking at the valuation right now, we do have a chance of 50% to 100% upside. These evaluations are made under certain assumptions which are given below.

- EPS based valuation:

PFC has been historically been trading at a P/E of 4-5 as an average over the last 2-3 yrs. Lowest P/E has been 2 which its currently trading at and highest has been around 18.

We have a fairly good upside of ~30-40% on this stock-based upon EPS remaining the same over the next few yrs ( which is quite a conservative assumption) and P/E reverting back to somewhat normal of 3 times instead of 4-5 times currently more inline with the past historical average.

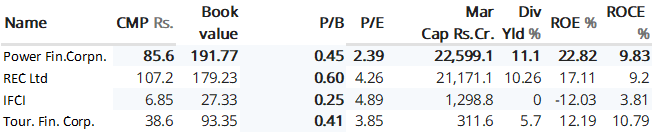

Also, its worth noting that its the largest power finance company in India even larger than REC while REC is trading at P/E of 4.3 vs PFC at 2.8

Note: 30-40% also takes into account the Dividend income of ~17rs on Rs87 stock price.

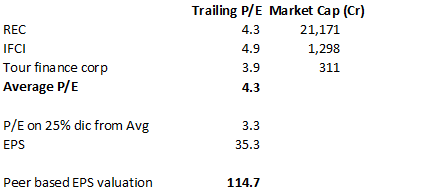

- Peer-Based Valuation

Again we have got a 60% upside against Peer-Based valuation (including dividend Yield) under a conservative 25% discounting to average P/E of the Peers. This I have done as I have highlighted risk earlier of Loan book being highly concentrated to state-owned power companies and risk of raising money to fund the loan book.

Also if you look at the above Peer, reason, why this company is so attractive, it has the lowest P/E in spite of being the largest Power financing NBFC in India and beating other NBFC’s in terms of ROE, ROCE yet lowest P/E.

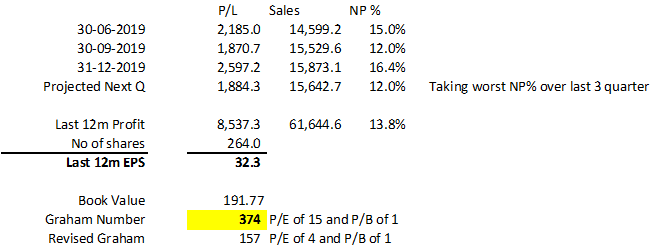

- Graham

Looking at the Graham, we will come up with a much higher valuation of INR 374. However, the Graham formula has certain flaws like P.E of 15 and P.B of 1.5 is assumed

this is obviously going to show the stock as massively undervalued. However, the core concept of Graham is still relevant, blind usage of the formula without understanding will not yield a correct result like below its yielding 374

In the below, I have modified the Graham formula to take a P/E of 4 which given the historical range of 2-18 and average of 4-5 P/E looks to be a much more reasonable and conservative P/E and P/B is assumed to be 1 given a growing company should always trade at least equal to its book value. Also looking at the closest Proxy of REC at ~4 clearly suggests this stock is mispriced.

Given the modified Graham formula, I get a price of 157 which shows an upside of >100% in relation to the current stock price.

- Book value approach

Looking at the book value, this stock is trading much lower than its book value as compared to its peers.

You might argue that why not IFC. We can clearly see that its not only has other poor parameters like ROE%, ROCE%, etc but also dividend yield is nil which doesn’t have GOI India backing yet trading at a P/E ~5.

This has the lowest P/E in the sector and trading at 0.45 P/B times just.

Risk:

-

The loan book is highly concentrated towards the State-owned power companies are highlighted earlier. Due to COVID, we do have a risk of delay in servicing of loans by these state government power companies however given power segment is a profitable segment and given company is a profit-generating entity so it should be able to sail through

-

There have been talks in the street that the GOI might reduce its stake < 51% on this company. While disinvestment I believe is good overall but <51% might turn to be bad in short term and the company will not be Govt controlled entity below 51% thus losing the ability to raise money at a cheap rate in the market. In the long term, I still think it will be good as a company can enter into JV with Foreign counterparties which are always better than raising money from abroad which the company is currently doing.

-

The ability of the company to grow its Loan book without incurring heavy Credit costs will be important esp during COVID times when the chances of getting caught in a bad debt trap could be huge.

4) Most important risk is the REC merger with PFC. Although the merger of the two largest power financing companies will create a monopolistic market however it is expected to limit the ability of the company to borrow from banks due to large combined debts. As per the latest update, due to this reason, the merger is still on hold. Due to this reason, PFC doesn’t have management control of REC although it has majority share in it. This issue needs to be examined closely however both are good profit-making PSU’s

Overall its a company with good historical growth, the strong Loan book growth, Lowest P/E in the Industry in spite of being the largest power financing NBFC, GOI backed and profit-making PSU, trading at all-time low P/E with best ROE and ROCE in the industry in its sector and good dividend payment history.

I have invested in this at the current market price of 85 for long term purposes given the above.

Disclosure:

-

I have an investment in this stock so my views might be biased. I request you to take your own judgment call before you make any investment in this name.

-

I am not a SEBI registered analyst so don’t have any recommendation service/Paid service. It’s an educational website that is just meant to share the analysis I do before I invest.