It’s 4 months and good time to update performance.

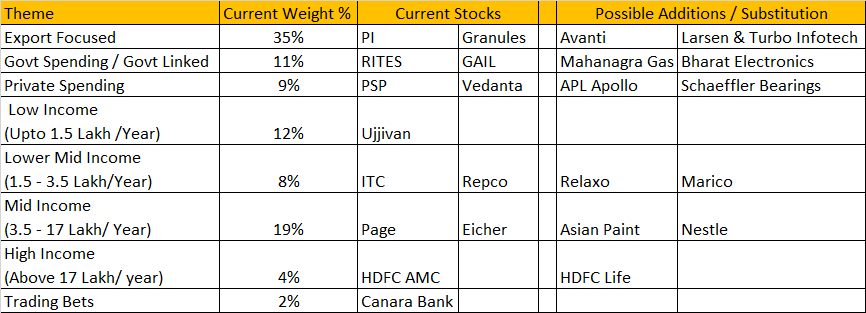

Export Focused - PI Industries, Granules, Laurus (3% of portfolio) struggled and down by 0%-15%-16% from July levels Vs market being up 8%. So close to 15% underperformance against the Index. But it still makes 30% of the portfolio. I thought results of PI was good, Granules was as bad or good as expected and Laurus was bit lower than expectations but too much discussed.

Govt Spending: Shifted out of RITES and moved it to SBI. SBI now makes close to 15% of portfolio and performed slightly better than Index. SBI Results were good and looks SBI will continue to perform a slightly better than Index for some more time.

Private Spending: Shifted out of PSP to India Bulls Real Estate. IBReal is really not a great proxy to private spending but there are more triggers in IBReal and hence made a call. Again performance is slightly better than Index. Given the triggers, narrative on real estate, increased the weight to 10% of portfolio. IBReal will be interesting to see how it unfolds. Biggest real estate player in India (Post merger) going in best decade for a country can not be at the valuations it’s currently at.

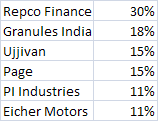

Low Income: Ujjivan disaster continues. It is now like 2% of portfolio. Anchoring bias taught a big lesson and paid well for this tuition. But not sure if I have learned still all lessons.

Low Mid Income: Repco at 3% weight continues in portfolio underperforming the index by big margin. Moved out of ITC as it was too much a discussed and analyzed stock by market with no price performance and result performance and hence moved the money to SBI for now.

Mid Income:

Page (12% of portfolio) has outperformed Index very well. Results and commentary is very positive but so are valuations. It will be interesting to see it’s performance over mid term.

High Income: Sold out HDFC AMC and SBI Life and moved the proceed to SBI and India Bull Real estate. HDFC AMC seems doing right things but results are still few qtr away. I am still looking for a stock in this area but not getting a luxury brand or a play.

IEX is the key performer of the portfolio and single handedly took care of all other mistakes and more. 70% up in 4 months with portfolio weight now at 15%. IEX has become a very highly discussed, momentum play stock but results are good so is the commentary around it and price performance. For me IEX is the bull market stock of this rally, as long as rally continues IEX will continue to perform. IEX reminds me of Page, it went from 4K when I started buying till 35K when the story peaked. (I continued from 4K to 16K to 9K to 35K back to 18K now at 40K)

CDSL stock performance is in line with Index but I liked results and it is another stock of this bull run similar to IEX.

Increased allocation to HCG to 8%. Results were good of HCG and I think management is taking right steps. So will be interesting play for next 18-24 months.

Missed Borosil Renewable was ready to pull trigger and reliance news came resulting into upper circuits. So another missed opportunity.

Future Plan: Planning to move out of Repco, Ujjivan and even Laurus (either Laurus will double in portfolio weight or will be replaced) . In watchlist is SAIL, Adani Port, Guj Gas, Power Grid, Syngene.

Over last four months, learning got reiterated that portfolio weight is most important thing.