Any updates in Pondys result?

Both Pondy oxide & Nile posted Superb no’s as expected!

Pondy’ new Zinc plant is coming up.

Power storage/Battery mkt is exploding.

1 Like

Q4 Results

EBITDA at 21.5 Cr vs 8.2 Cr

PAT at 10.7 Cr vs 2.93 Cr

FY17 PAT at 28 Cr vs 10 Cr

Great numbers

Pondy’s OPM has doubled in last quarter… Is it sustainable ??

Taking avg price for last 3 mths = USD 2087 per tonne

& based on TTM sales of INR 759cr, POCL sold ~56k tonnes.

POCL capacity is 57k tonnes, so it is operating close to full capacity.

Further increase in sales is limited.

Next triggers can be through margin expansion or debt reduction or PE expansion.

Business points discussed 6-7 yrs back in this thread are still so relevant today.

Disc - interested but not invested.

Whats the capacity of the zinc plant ? How much can it add to revenues under 100% utilization ?

Here are my notes on the company.

POCL increased its annual production of Lead Metal and Alloys from 32,140 MT in the previous year to 46,636 MT in the financial year 2016-17 showing an increase of 45%.The Company forecasts to increase its capacity utilization from 78% in the year 2016-17 to 95% in the year 2017-18.

Source: Annual Report 2016-17

Based on the production and utilization, company’s lead capacity works out to 60,000 TPA. Company has not been giving volume numbers except for most recent annual report. Based on the above company expects 20% increase in production this year. I cross checked this with power consumption (which is a major expense for this company besides RM and it is proportional to volume of production.) In 2016-17, power consumption was 50% higher than previous year. Similarly, in Q1 FY2018, other expenses (which are largely power costs) are up 25% from year ago so volumes may have gone up 20% this year Q1.

Zinc capacity has started trial production in Aug 2017 so over next few quarters this capacity should add to top and bottom line. Zinc capacity is 12,600 TPA.

Source: company filings on BSE.

Additionally, company has acquired 60% of Meloy Metals in Sept 2017. (a related party as Ashish Bansal is director of both and CFO of Pondy is director of Meloy Metals).

Zinc capacity and Meloy metals (as and when it closes) will add substantially to existing capacity and should provide good visibility for next 2-3 years.

Now the question is, will the company sell all it can make and at remunerative margins? So far it looks like company is able to sell all it can make as seen from a 45% jump in production in 2016-17. Similar gains are seen for other players (Nila and Gravita) so it is unclear if this is industry tailwinds or something else. I don’t think demand has gone up that much.

Risks

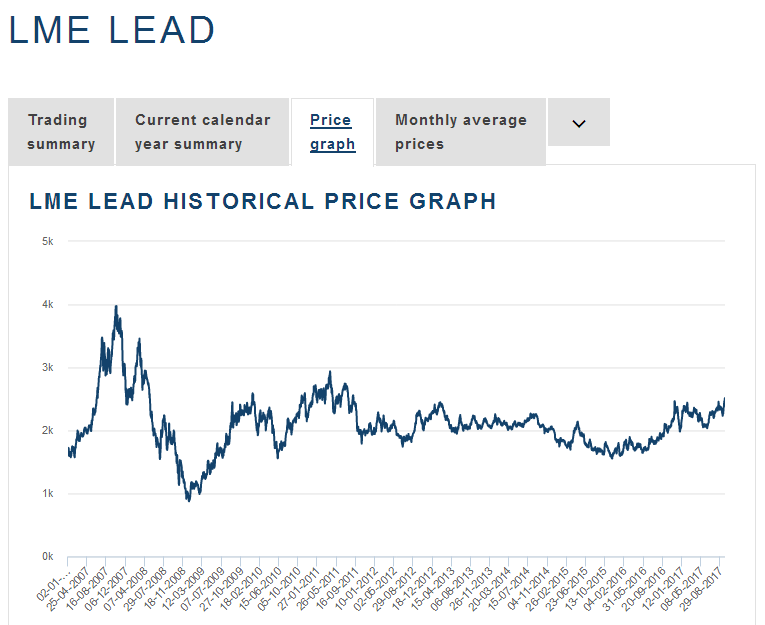

Price volatality of lead is a major risk and it has been discussed here before. Here is a long term 10 year chart of LME Lead prices

Source: LME

It shows that prices were indeed very volatile in 2008-09 and then some in 2011. since then, volatility has reduced. Also prices have gone sideways for almost a decade so a substantial price drop is unlikely from these levels.

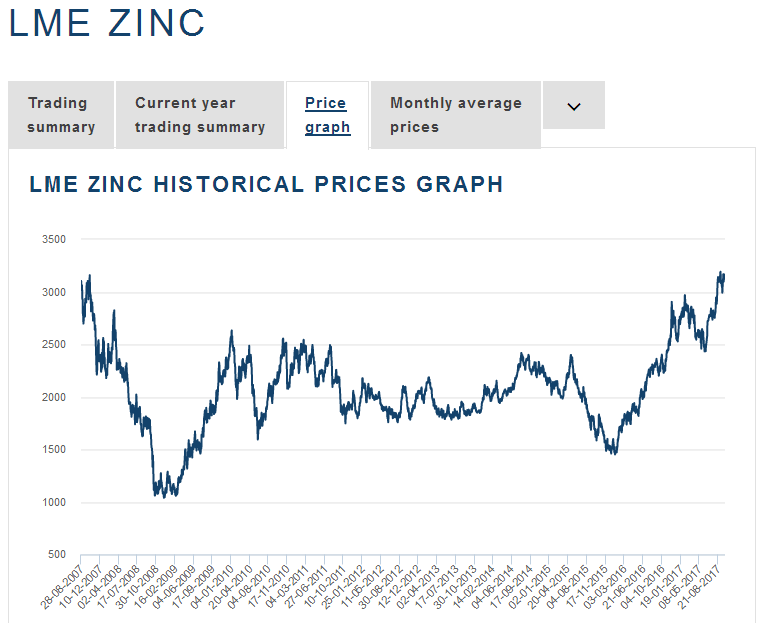

Zinc is often used as a substitute for Lead but Zinc prices have gone up much more than Lead so that does not look like an immediate threat. However, zinc prices are much more volatile than lead.

Source: LME

Loans from promoters

Mr. Ashish Bansal has advanced unsecured loan of Rs. 453.28 lakhs to the Company. He holds 6,33,086 equity shares in the Company. None of these are pledged.

Mr. Anil Kumar Bansal has advanced unsecured loan of Rs. 582.24 lakhs to the Company. He holds 6,22,761 equity shares in the Company. None of these are pledged.

Mr. R.P.Bansal has advanced unsecured loan of Rs. 616.04 lakhs to the Company. He holds 4,97,302 equity shares in the Company.

Source: Annual Report 2016-17

Loans from promoters should be viewed with skepticism. A promoter should issue shares or warrants to himself/herself instead of lending money to the company especially when promoter shareholding is low. A loan promoter to company means that promoter thinks share price is too high or it is likely to decline and would rather be a creditor than a shareholder. If the company’s performance and share price is expected to improve, promoter would normally issue warrants / shares instead of loans. Often, promoters pledge shares and lend money to company but that is not the case. Also company would borrow directly from banks using promoters shares as collateral rather than borrowing from promoters.

Disc: No position but interested.

7 Likes

Company itself is saying that increased lead capacity is 46,636 mt. Most humbly, I could not understand how you have mentioned 60K TPA capacity?

46,636 TPA is production.

Capacity = production / utilization

or

46,636 / 78% = 60,000 TPA.

Source: AR 2016-17.

4 Likes

According to this disclosure on BSE the few promoters have been classifies as public resulting in promoter holding decreasing from 51% to 46%.

Do we have any knowledge about any pending succession planning among the promoter family?

Does anyone still trackung pondyoxide…hows Q3 numbers expected and any trigger in near term…lead prices making new highs and soon there zinc facility may start commercially…

Q3 Revenue has been flattish compared to Q2 & YoY basis. Improvement (about 20%) in profitability. EPS for first 9 months is about Rs. 39.

Annual report suggest that Zinc facility was scheduled to start from Aug’17. However there is no meaningful improvement in Q3 revenue. Does anyone has confirmation about commissioning of the zinc facility & how much additional revenue management expect from zinc & zinc oxide?

No disclosures by company on this front. We need to write to company to get the answers.

You have reviewed the company for long time @Yogesh_s.

Anybody still tracking this company? Results are out and EPS is around 20 for this quarter but looks like it is mainly because of Inventory gains. Any views on this would be helpful and highly appreciated!

1 Like

@ayushmit :- Dont u see the similar situation in Pondy when you first found it.

Current Capacity is 84000TPA, They are on track to make it 120000TPA in next few years, with Zinc Oxide Capacity of 12000TPA company can do a turnover of 2000Cr and a Possible Net Profit of 100Cr??? Trading at 1Times FY 22-23?

1 Like

Word Multibagger is Prohibited on this forum, so sharing just a link.

https://strategicalpha.wordpress.com/2020/01/17/pondy-oxides-cmp-205-a-potential-multibagger/

Hi, I haven’t been tracking this company since last few years. I had lost interest as I felt the business is too volatile for my comfort.

2 Likes

Ok. This business is under my circle of Competence. (Metals,AMC’S, Trading Business, Environmental Businesses) are the businesses which I can understand well. Pondy has a potential to generate profits of 50% of the current Marketcap in next few years, recent results are on the same lines.

Stock is quite undervalued, and seems like market is discovering it. Stock is up 25% past week.

2 Likes

Hi, Trying to understand Pondy Oxides. The Share Price @ 169/-, Cash and bank balance @ 7/-, CFO @ 42/-, Reducing debt/ Conservatively financed, OPM margin decent for a commodity business, Increasing sale, Debtors of 30 days. This share looks to be a steal. What am I missing? Please advise.

1 Like