Sanjiv is 63, also no one else from family has joined the business yet. Most of top management is working with him for 20+ years now. They are also reaching retirement age. It looks to be a part of retirement plan.

4 Likes

180120230921050028E.pdf (27.8 KB)

1 Like

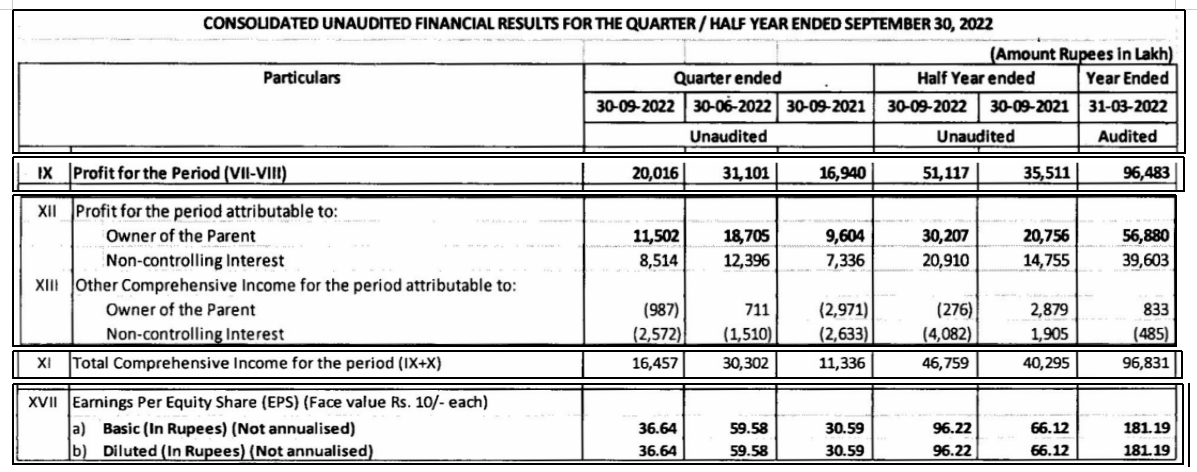

The company calculate its EPS by:

EPS= Profit for the period attributabe to owner of the Parent/ Total Shares = 11,502 lacs ÷ 313.9 lacs = 36.64 EPS.

(*Non-controlling Interest represents the equity in a subsidiary not attributable, directly or indirectly to a Parent. Non-controlling interest in the net assets of the subsidiaries being Consolidated is identified and presented in the consolidated Balance Sheet separately from the equity attributable to the Parent’s shareholders and liabilities. Profit or loss and each component of other comprehensive income are attributed to Parent and to the non-controlling interest.)

Is my understanding correct that we cannot think Profit for the Period is the real profit of the company?

Also Upon calculating PE Ratio by using Market Cap and Net Profit/PAT, I cannot arrived true PE Ratio.

1 Like

Abakkus Emerging Opportunities Fund-1 and Dolly Khanna have exited their holding. Does this indicate to sell the stock?

Also the company has guided lower EBITDA for Q3FY23. The company has no con call. I see some overcapacity.

In 2013 and 2014 the capacity of thin PET is 1.42 and 1.48 times the demand of thin PET respectively. It is likely to occur during 2022 and 2023 from the studying the graph.

The CMP is around 52 week low. While NCAVPS (Net Current Asset Value per Share) is INR 1,009.

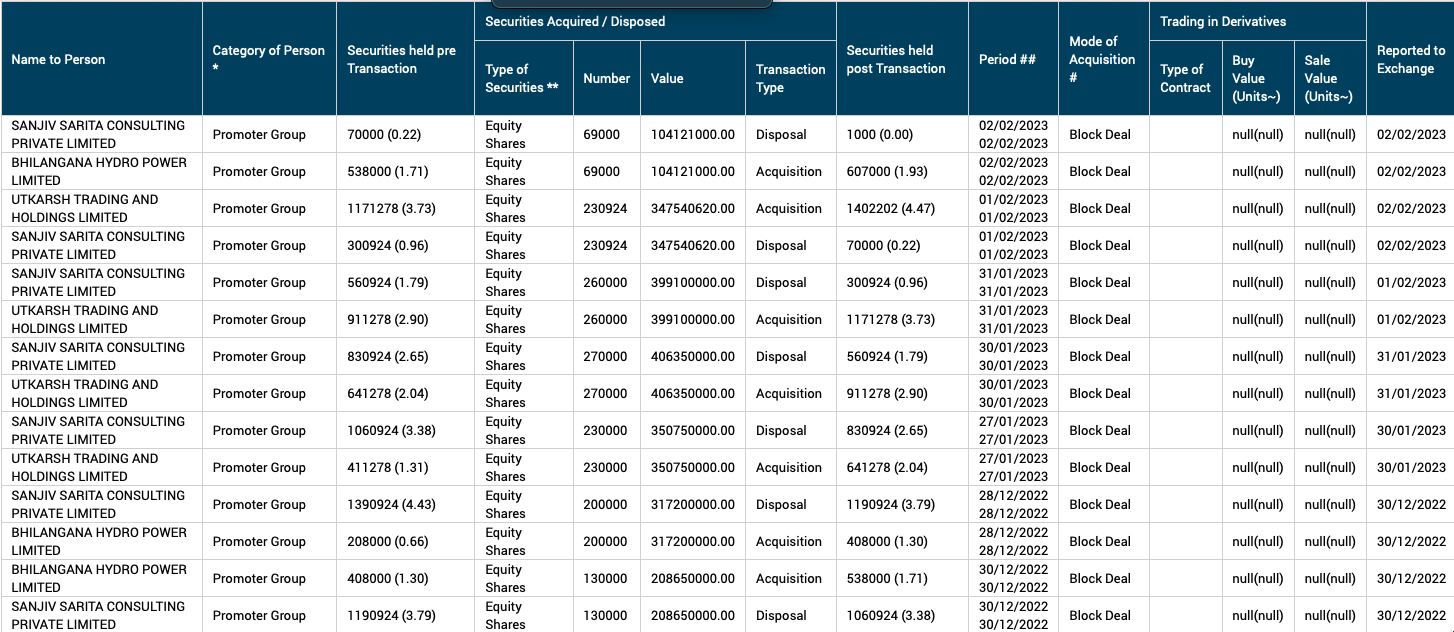

Clearly the promoter Sanjiv Saraf is not interest to run the company. The company is giving high dividend which indicates that the company don’t how to use the surplus capital.

Global scenarios of higher inflation and generally high material cost looks no good.

I am still holding the stock from Nov 2020. I got 276 dividend per share till now.

I think about exiting the stock but the discounting the market gives pull me in to hold the stock. Is it value trap? Is the company short term future look bleak?

Anyone holding the stock give me some insights?

1 Like

@praveen2510 I don’t really know the motive behind this transactions. One can ask write directly to the company as there is no con calls of this company. If you write to the company and got replies, please share in this forum.

But I speculate that company founder Sanjiv Saraf is no longer interested in running the company. He exit his individual stock holding.

Directors of Sanjiv Sarita Consulting Private Limited are Rajesh Kumar Jindal, Ashok Kumar Gurnani, Manav Kothari, Pranay Kothari, Ritu Kothari.

Maybe WTD Pranay Kothari want to strike off this Sanjiv Sarita Consulting Private Limited.

@indirachitra

Polyplex and Cosmo are good company to me.

Uflex and Jindal Poly have lowest dividend payout while the industry are giving good dividend. This indicating lack of transperancy and capital misallocation. The stock looks like a value trap to me. Also I found bad governace in these two companies.

Products: Polyplex is mainly in BOPET. While Cosmo is mainly in BOPP.

PAT margin: Polyplex have 2 digit margin 5 times out of 10 years. While Cosmo improving its margin recently at 12% and maintaining strongly in recent sep quarter also.

Asset Turnover: Cosmo have high asset turnover ratio of 1.28. vs Polyplex have 0.99

Working capital days: Cosmo have lower 45 days while Polyplex have 60 days.

EPL limited have high payable days of 100 days while working capital days of 15.4 days. Indicating sth about EPL highest valuation in the industry.

Shareholder friendly: Polyplex and EPL have the highest dividend payout ratio nearly 50% in last 2 years. Also cosmo is giving decent dividend and doing buyback.

Tax rate: Polyplex is the only who benefit from low tax rate 16.88% average of 3 yrs. While Cosmo film have the highest tax rate 27.17% average of 3 yrs.

Cash Cycle: Cosmo have the lowest cash cycle 63.33 days. vs 146 days in Polyplex.

ROE and Profit growth 5yr : RoE and profit growth highest in cosmo 22% and 37% repectively. while Polyplex have 12.8% and 23% respectively.

Industry of Poly Film packaging is a commodity business. Overcapacity have lead to losses. Company trying to temper the cyclicality in the business by producing value added products. The market is giving discount of these stocks except EPL Limited.

6 Likes

Do post on the forum in case the Company clarifies your questions.

I had written at the Investor mail id of Polyplex with a follow up to Co. Sec. on Con Call, did not hear from them.

Await Q4 numbers and clarity on the underlying point on the Stake Sale on the table

1 Like

This quarter results are good in standalone basis and drop in consolidated basis how to analyze results in this scenario kindly throw some light any body on results?

จำกัด (มหาชน) PTL")

Concall

4 Likes

Polyplex Thailand Con Calls are on the following day after the results.

Polyplex India had no Con Call on Results post Q2 FY23, no intimation of a date when and if, they would hold for Q3 FY23 Results.

Polyplex declares a final dividend of Rs 3/ Share.

Consolidated Revenue stands at Rs 7652 crores with a PAT of Rs 615 crores.

The last time it declared final dividend in single digit was in 2016 when Consolidated Revenue stood at Rs 3200 crores with the corresponding PAT at Rs 16 crores!

Company has entered into a binding term sheet dated May 23, 2023 with certain members of Promoter Group and AGP Holdco Limited (Investor)

Promoter Group Members have agreed to sell to the Investor 24.2778% stake in the equity share capital of the Company for an aggregate consideration of INR 1379.47 Crores

That’s around Rs.1809.99574 per share.

How does one read this? On one side the results look bad, on the other side stake is being bought at a premium!!

Noting to worry on resilts . Its fully.pricwd it. We have seen similar results from all oetrochem plastic products as RM COST WERE HIGH and inventory is high which .ust have been sold at loss m q3 smale issue. China repoem has hit all the yarm chemical plastic etc industry …fall is becaue stake sale done below 25% so no open offer. But buyer is huge player and they will inveesse ans eventually open offer wkll emage

1 Like

BOPET business to remain under pressure for some more quarters to come

From Polyplex Investor Presentation on Q2 FY24 Results:-

Short to Medium term outlook

• Slow recovery in demand is expected in both Industrial and Packaging segments •Reduction in cost –primarily utility in Europe and normalization of freight

• Anticipated weaker global GDP growth along with the supply overhang is expected to continue for some time

•Continued efforts on portfolio expansion, increase in DPAC sales will help support improvement in margins

1 Like

Did anyone attend the AGM today? Highlights ?

The Co. does not post Audio Transcripts of its AGMs and hence they are not available on Co website.

Is there any information available on the proposed 28.4% sale by promoters to an investment firm? The promoters have pledged 100% of their shares, but I could not find any information on the reasons in their annual report.

Disc: has entered the stock recently