SEBI’s regulation. Please go through the attachment i have posted above. That contains the answer to you query

3 Likes

Polycab Q4FY22 results Press release

Strong results.

- Q4FY22 Revenue at Rs. 3970 Cr; up 35% YoY

Q4FY22 EBITDA at Rs. 476 Cr; up 18% YoY

Q4FY22 EBITDA at Rs. 476 Cr; up 18% YoY

Q4FY22 PAT at Rs. 325 Cr; up 20% YoY

FY22 Revenue at Rs. 12,203 Crs ; up 39% YoY

FY22 EBITDA at Rs. 1262 Crs; up 14% YoY

Wires and cables business grew 39% on YoY basis to Rs. 3511 Crs in Q4FY22 from Rs. 2530 Crs in Q4FY21.

Domestic distribution driven business continued to see strong traction. Housing

wires posted strong growth led by continued momentum in real estate and

renovation activities as well as demand generation initiatives. A new sub brand

“Etira” was launched in the economy price segment.

Trade sentiment in Cables was temporarily restrained by significant volatility in Aluminium prices. Exports business was 2x of last year led by strong demand from sectors like Oil & Gas, Renewables and Infrastructure globally.

Segmental margins continued to improve sequentially led by judicious price hikes and improved operating leverage.

FMEG business grew 9% YoY to Rs. 379 Crs in Q4FY22 from Rs. 346.8Crs in

Q4FY21.

Overall demand momentum in Q4 was subdued largely attributable to broader inflation.

The business also underwent realignment exercise to improve sales force efficacy and achieve distribution synergies.

Fans, lights and switchgears business posted healthy growth while Conduit Pipes continued the strong

momentum. Switches saw a decline due to supply challenges. Transition to inhouse manufacturing of switches is in progress. Solar business was muted however for the full year it achieved over 50% YoY growth.

• EBITDA margin continued to improve sequentially by 125bps to 12.0% led by price hikes

and better operating leverage, partly offset by persistent input cost pressures. PAT margin

improved to 8.2% against previous quarter. PAT grew 20% YoY.

• As of 31 March 2022, Net Cash position stood at Rs. 1100 Crs as against Rs 960Crs last year.

Debt to Equity decreased to 0.01x.

Declared a Dividend of Rs 14/- per share.

Press Release text

fa8d349e-3b10-4508-88d8-f320dbdff1fa.pdf (bseindia.com)

Q4FY22 Results.

8d8629d4-54b1-4079-ab06-410ae54e1bdd.pdf (bseindia.com)

7 Likes

2 Likes

I would like to add few more points that I have collected from last many quarters of results and earnings call

1- The EBITDA margin was slowing down by past few quarters, and in this quarter, it reversed and was 12%. The long-term guidance of the management for EBITDA is between 11-13%, and happy to note that we are back in the range.

2- Over the past one-month Copper and Aluminium prices have significantly corrected. What it means for Polycab? The RM cost would go down.

3- Polycab’s project LEAP is on right track and Gandharv spoke about quite a few changes they have implemented in the first year - having presence in economy segment, better job on channel financing thereby reducing inventory days and working capital, backward integration on switches etc.

4- The company did north of 12000 crores of sales and EBITDA margin for the full year was 10%.

5- The split between B2B and B2C sales was 60% to 40%.

Future prospects and my comments

1- Project LEAP target is to have 20000 crores of sales by FY26. I expect that most likely Polycab would hit that target sooner than that.

2- The FMEG business is ripe for a bounce back and expect that in coming quarter the company would go back to 30% plus y-0-y growth on topline. Particularly the Fan and lights segment should do well in next two quarters, and switches would start doing better from Q3.

3- Wires segment would continue to see good traction because of tailwind in reality, and cables because of a lot of government infrastructure projects.

4- Company is sitting on a cash of 1100 crores. Taking away about 400 crores for Capex there is still good money on the books. Add another 800-1000 crores of free cash that would be generated in Fy2023, and the number looks very big. This a great time for the company to look for M&A (Gandharv indicated on it too) or increase the dividend payout/buyback (completely my expectation)

5- I expect with RM going down, the EBITDA would inch towards 13% in the coming quarters.

6- For the full year FY23 I expect, top-line to grow 15%, so the sales would be 14000 crores. With 13% margin, EBITDA would be 1820 crores. Add other income of 100 crores, reduce 40 crores of interest and further reduce 220 crores of depreciation. This would leave with 1660 crores of PBT. Tax at 24% would be 400 crores. The PAT for the full would be 1260 crores. For comparision the PAT was 900 crores in FY22, and so I am expecting PAT to grow about 40% translating into EPS for FY23 to be 85 rupees. I do understand that it sounds optimistic but I have a strong feeling based on logic that they would be able to do it if another bif event like Covid would not hit them.

Cheers,

Krishna

PS: I am not an analyst. This is not a buy or sell reco. I have done transactions in the last month.

22 Likes

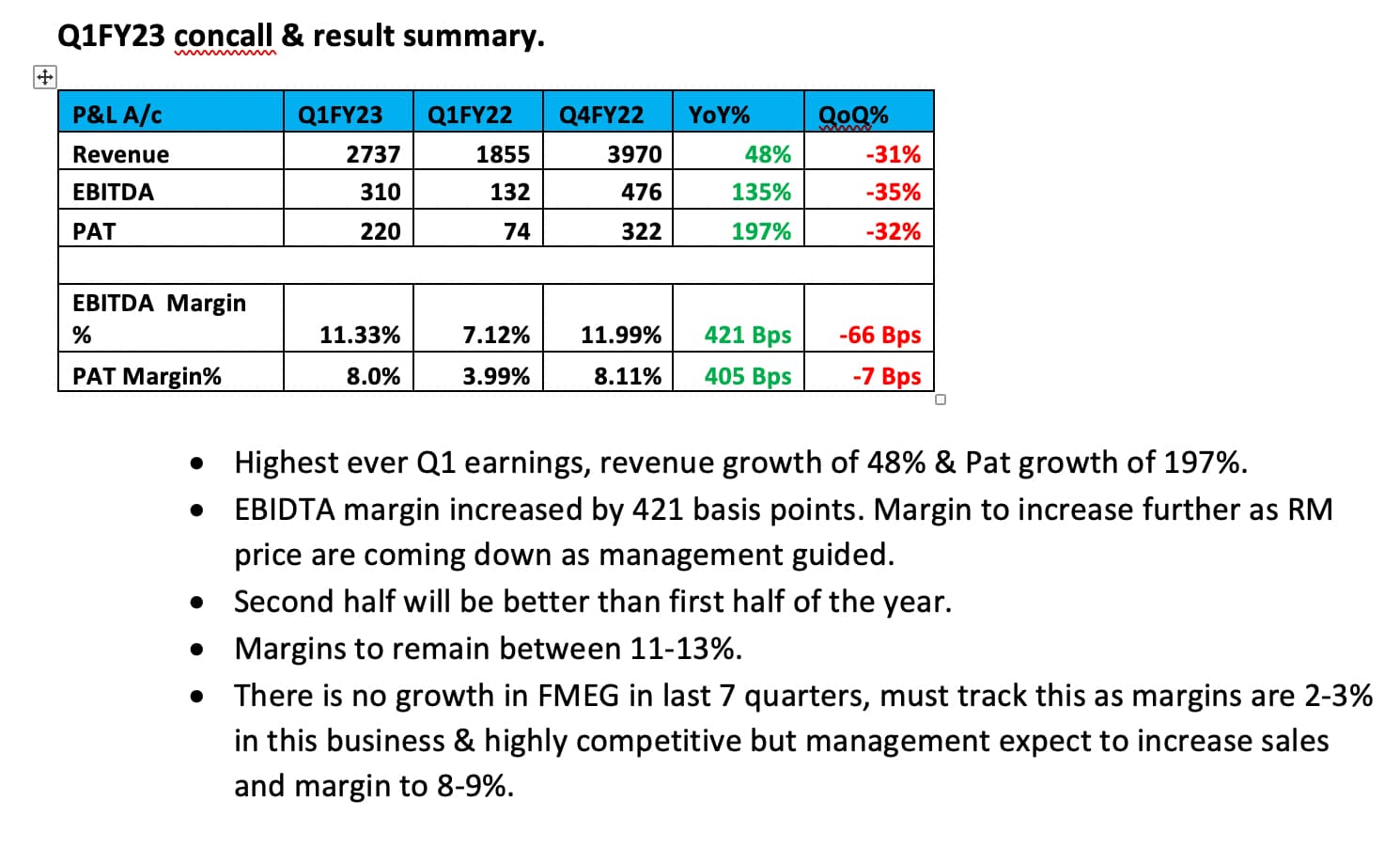

Any specific reasons for 30% drop in revenues from previous quarter Q4?

1 Like

Due to commodities’ prices coming down, consumers are delaying their purchases, expecting prices to come down further. Hence, sales reduced compared to Q422.

1 Like

and historically 2nd half is better than 1st half.

1 Like

June qtr has always been weak. I don’t understand the reason either. Anyone knows why is there such cyclicity?

1 Like

The customers are usually companies doing capex , So to show better capex utilization they procure much more during the end of the financial year. So the march quarter is the strongest usually and june quarter weakest

2 Likes

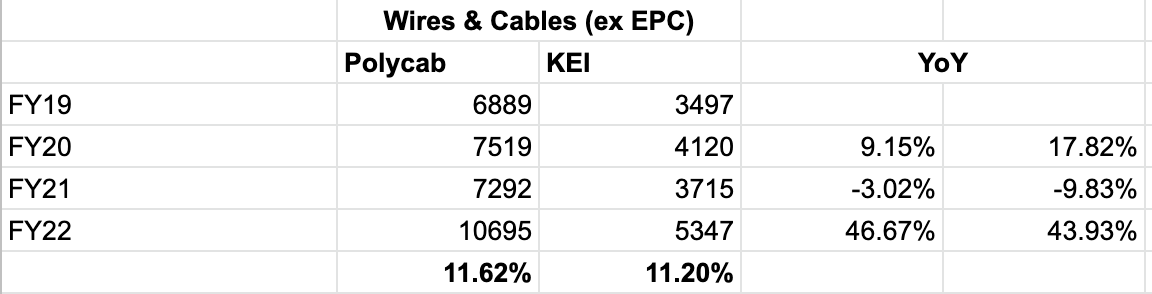

Polycab has degrown more QoQ than KEI because of retail channel destocking has been severe and Polycab is more B2C than KEI. Nothing else. History also tells us such things happen and Polycab has slighly outperformed as well but more or less same -

6 Likes

3 Likes

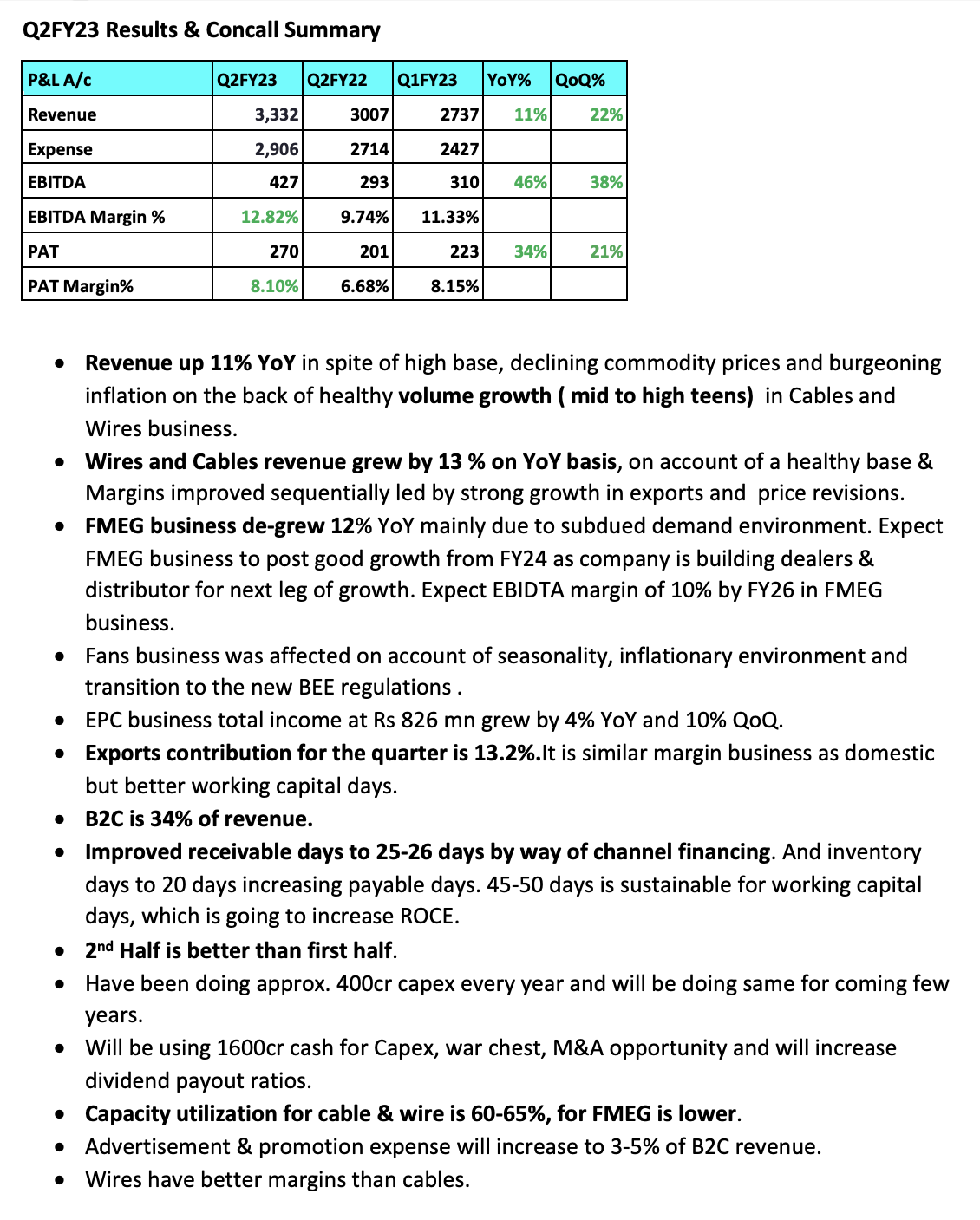

Q2 FY 23 Results. Good results.

Press release on Q2 results

Sustained Growth Momentum

![]() H1FY23 Revenue at ₹ 6068.9 Cr; up 25% YoY

H1FY23 Revenue at ₹ 6068.9 Cr; up 25% YoY

![]() H1FY23 EBITDA at ₹ 736.7 Cr; up 73% YoY

H1FY23 EBITDA at ₹ 736.7 Cr; up 73% YoY

![]() H1FY23 PAT at ₹ 493 Cr; up 82% YoY

H1FY23 PAT at ₹ 493 Cr; up 82% YoY

![]() Q2FY23 Revenue at ₹ 3332.4 Cr; up 11% YoY

Q2FY23 Revenue at ₹ 3332.4 Cr; up 11% YoY

![]() Q2FY23 EBITDA at ₹ 426.8 Cr; up 46% YoY

Q2FY23 EBITDA at ₹ 426.8 Cr; up 46% YoY

![]() Q2FY23 PAT at ₹ 270.5 Cr; up 37% YoY

Q2FY23 PAT at ₹ 270.5 Cr; up 37% YoY

Key Highlights (Q2 FY23)

• Revenue grew 11% YoY to ₹ 33,324 mn in spite of high base, declining commodity prices and burgeoning inflation on the back of healthy volume growth in Cables and Wires business

![]() Wires and cables business revenue grew 13% on YoY basis to ₹ 29,259 mn. Domestic distribution driven business continued to see strong momentum. Institutional business too saw healthy growth.

Wires and cables business revenue grew 13% on YoY basis to ₹ 29,259 mn. Domestic distribution driven business continued to see strong momentum. Institutional business too saw healthy growth.

![]() Exports business exhibited strong growth of 75% YoY on a healthy base, contributing 13% to consolidated revenue in Q2 FY23

Exports business exhibited strong growth of 75% YoY on a healthy base, contributing 13% to consolidated revenue in Q2 FY23

![]() FMEG business de-grew 12% YoY to ₹ 3,032 mn mainly due to subdued demand environment, exacerbated by realignment in distribution strategy undertaken under Project LEAP to improve long-term business growth. Fans business was affected on account of seasonality, inflationary environment and transition to the new BEE regulations. Switch business recovered from the lows

FMEG business de-grew 12% YoY to ₹ 3,032 mn mainly due to subdued demand environment, exacerbated by realignment in distribution strategy undertaken under Project LEAP to improve long-term business growth. Fans business was affected on account of seasonality, inflationary environment and transition to the new BEE regulations. Switch business recovered from the lows

of Q1FY23, posting 123% QoQ growth.

• PAT grew by 37% YoY to ₹ 2,705 mn from ₹ 1,978 mn in Q2FY22. PAT margin stood at

8.1% for the quarter

• As of 30th September 2022, net cash position improved to ₹ 16.7 bn against ₹ 8.7 bn

net cash during the same period last year

• The Company merged Fans vertical with Lights & Luminaries vertical and Retail Wires

vertical with Switches & Switchgears vertical to unlock latent value through crossselling opportunities and operational efficiencies.

6 Likes

Is there any more information like size and quantum of works and revenue expectation?

Is there any bad news about polycab?

Stock price is crashing like never before?

1 Like

Not seeing the growth in FMEG I want.