1 Like

5 Likes

Four brothers of 1st generation have done well during struggling period. But now 4 cousin brothers are running the show in growth phase. I hope there is clear succession planning.

I may be sounding somewhat foolish because I am relatively new investor. Is this a concern as I am interested in Polycab for investment.

Hello,

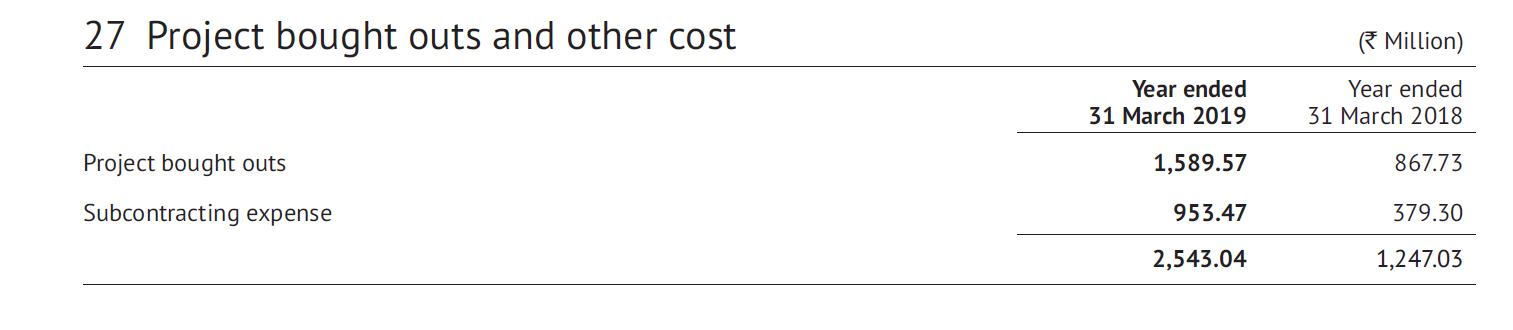

I am new into Equity market and was trying to understand a cash flow statement. Can anyone explain what is the below expense and what is its significance ? ( Snapshot from Polycab Annual report )

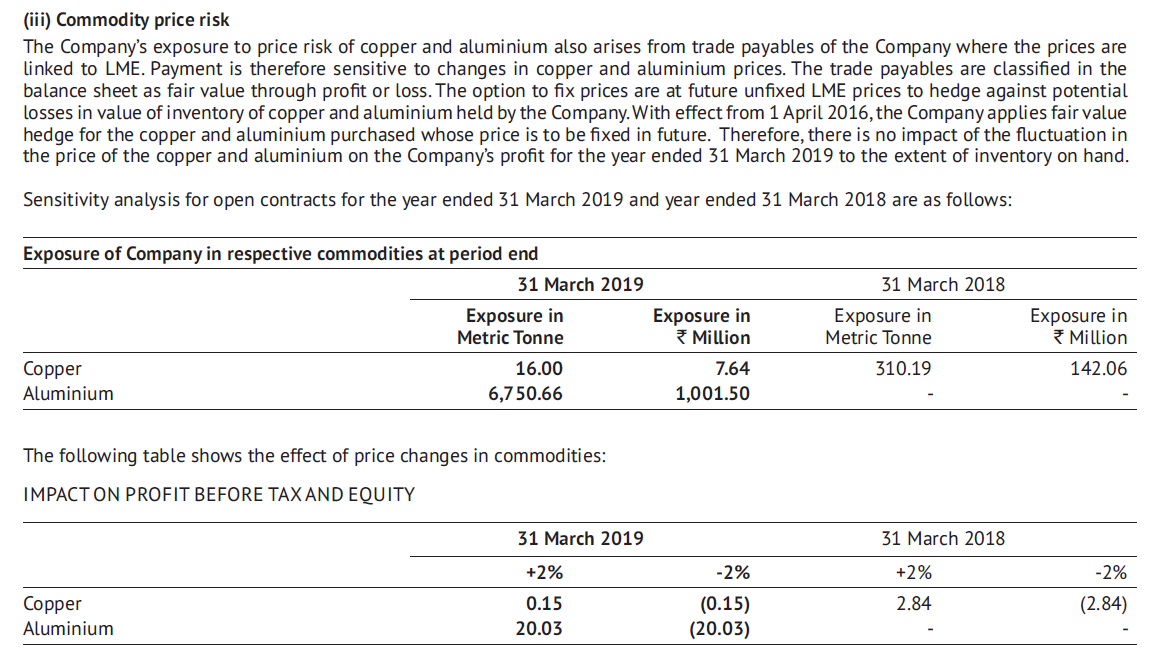

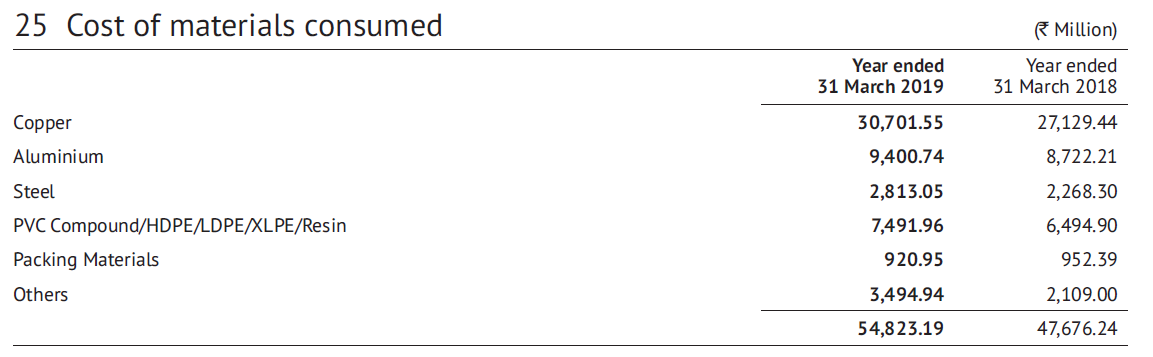

Why is the exposure in copper very less in 2019 compared to 2018 even though there is increase in sales and copper constitutes a major portion of raw material cost ? as shown in snap below

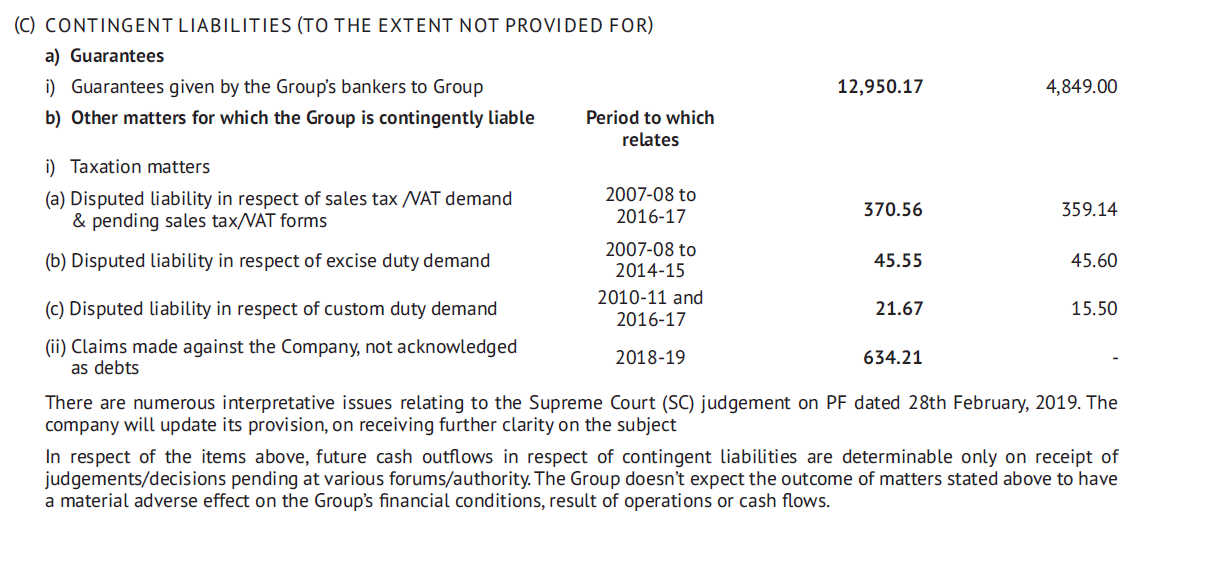

Also could some one help clarify the increase in bank guarantee (Almost 3 times increase compared to previous year) and its possible impacts. Whether good or bad ?

From what i understand :

-

Polycab opened a copper rod manufacturing plant with Trafigura which a global commodity player ( 50:50 JV) in Halol Gujarat. Now polycab sources almost all of its copper requirements from the plant ( JV) itself, and so its doesnt need to hedge its copper requirements. Thus the exposure to copper derivatives is low.

-

Bank guarantees generally increase with the liabilities of the company. From FY18 to FY 19, the increase in the liabilities for the company is roughly around 800 Cr, which is the increase you see in the bank guarantees as well . According to me, this seems to be positive for the company as banks extending guarantees should indicate good repayment capacity.

4 Likes

Thank you Siddarth.

Could you kindly let me know your views on the below point too.

Ryker, the JV which is now fully acquired by PIL is manufacturer of conductors and rods. Even for Ryker, copper is a raw material whose price shall be affected by global events and supply.

I have just started learning fundamental analysis and not sure whether this is a trivial matter or worth more detailed check. Just caught my attention while going through the annual reports.

Thanks Nigil , I guess i missed a point there .

The JV hedging should be consolidated in the parents financials .

In 2018, seems like they had majorly hedged their copper requirements . 310 metric tonnes hedged nearly represents the raw material cost of copper for 2018.

Considerable reduction on Copper hedging exposures for 2019 can be attributed to fall in Copper prices in H1’18 and thus lower volumes hedged, maybe.

Even i am new to investing, so we are in the same boat in terms of wondering about trivial matters.

1 Like

Imo this is one of those no brainers. Available around fair value currently and is already the market leader in Cables and wires and they are using their cash created to move into FMEG which gives it a stable business + a huge runway for growth in the consumer space. That being said I have a question. For companies to start profiting in the Fmcg space it takes them years. However, they print money when everything is set. I’ve not really followed FMEG companies before… does the same principle apply here? This looks like it’s mimicking havells model so maybe an in depth study there would help?

Disc: invested. Though I can’t afford too many shares at one time. So buying in sip format

1 Like

On FMEG venture, Polycab’s existing pan India network and brand name familiarity is an advantage. But grabbing a meaning-full market share going to be difficult.

Last week I found Polycab LED tube lights in a near by electrical shop, when enquired about the quality, shop owners response was positive. I feel that, their lighting business could easily pick up in the coming years as they can sell them through their existing network and the current brand goodwill should be enough for this segment.

However they may struggle to sell relatively high valued items like “Fan” as Polycab doesn’t seem to be having neither cost advantage nor brand advantage here. I checked Amazon & Flipkart and don’t see major attraction to brand Polycab. No wonder as their listing price is close to “Usha” and “Crompton”. So why should someone but a polycab fan? We needs to see how management tackle it.

https://www.amazon.in/s?k=Polycab+fan&rh=n%3A4369221031&ref=nb_sb_noss

Disc: Invested.

2 Likes

Hi everyone,

Disc: Researching polycab since I have an investment in its competitor KEI industries (as my effort to better understand the industry). No investment in Polycab.

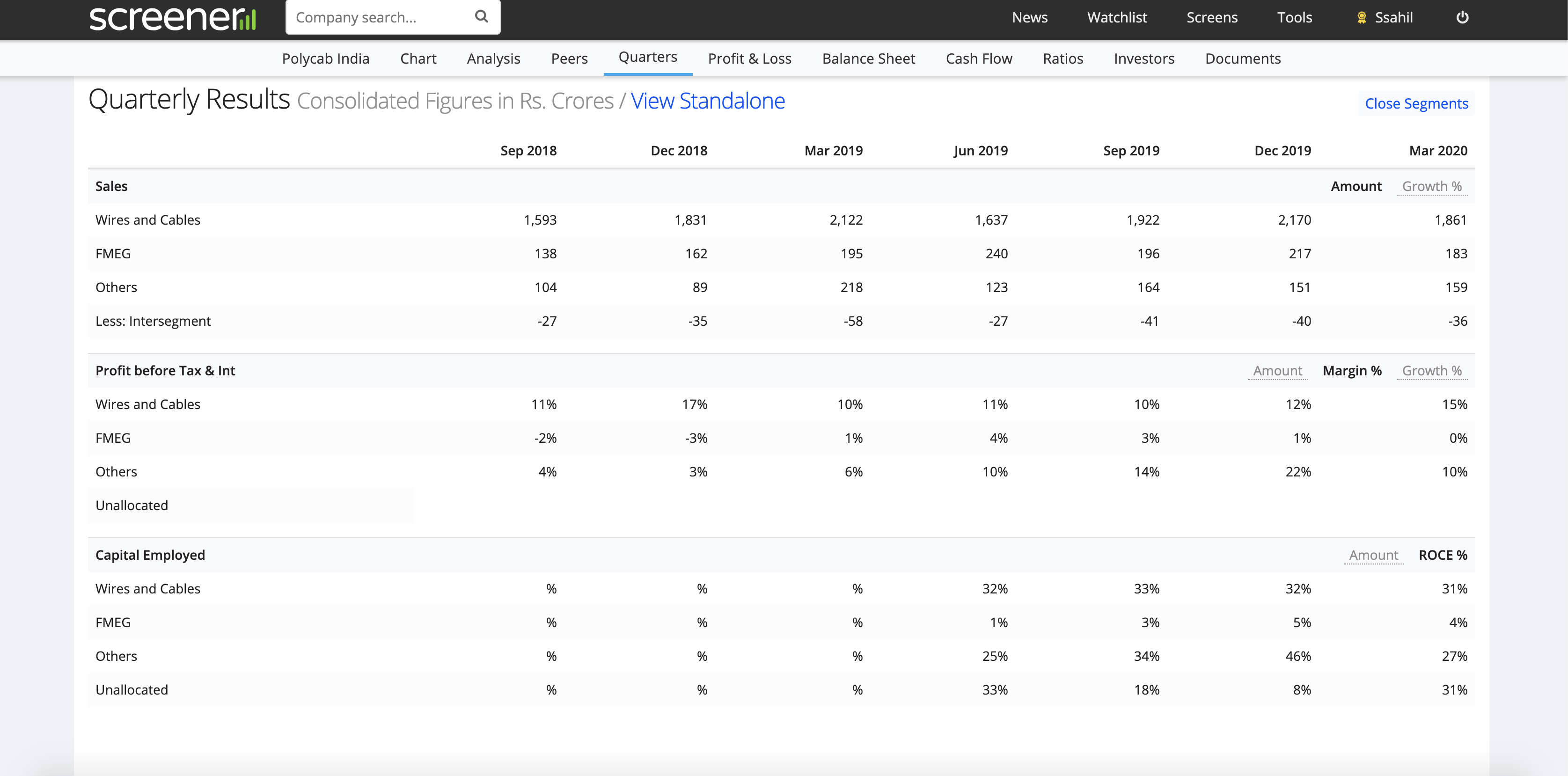

I can see on screener that the NPM and ROCE for the FMEG segment is kind of low for Polycab.

Does anyone know why Polycab margins and ROCEs are low for FMEG? Is this because its difficult to establish an FMEG brand and compete with existing companies like Havell’s etc? Does the management have a take on what they foresee for this segment?

As Polycab has got listed recently, I’m not sure how accurate the capital employed split is. Also the segment wise screener data for Havels and Finolex has a line item “unallocated” makes me to guess that screener is fuzzily calculating the numbers.

We should look at sales to capital employed as Polycab’s FMEG business is relatively new and margins are close to zero. Still Havells is doing exceptionally well but without capacity utilisation metrics its really hard to do an apple to apple comparison.

2 Likes

Polycab ventured into FMEG only recently and it is currently focussed on increasing market share(currently mere 1%) and also segment contribution to the topline. From 4% a couple of years back, the segment contribution went up to 12% which itself is laudable. The segment EBITDA margin is also expanding and is close to 3.7%. Mature companies like Havells and Crompton have a margin of 10-13%. It’s a long term play on FMEG business and I feel it is futile to compare the numbers at this point in time. However, the guidance for FMEG looks positive from the recent management commentary and is well poised to grow at 30-40% over the next few years.

6 Likes

Can’t compare polycab n havells in my opinion. Havells is big in B2C where as poly profit from B2C is negligible n they are just scaling it up by toplibe . The kind of working capital cycle, return ratios, pricing power of a b2b electric good company is very different from B2C n hence different valuation. However, among b2b, polycab stands out and they are scaling up well in B2C though not much profitability, reason being front end investments in people, distribution and branding . If they can build a profitable B2C with reasonable share of profit, it can get rerated

2 Likes

Not so great results for this Co. for Q1FY21 , is this an aberration or a sustained FY21 phenomenon only time will tell but the loss of :

Sales ( down 50% y-o-y) EBITDA ( down 75% y-o-y) & Margin down to 5.8% from 11.5% …is quite a steep drop .

Any learned friends in the forum who have some insights , opinion on the Q1 performance of this Co. and how does it compare to Bajaj Electricals & Havells will be interesting to watch out .

If you go in result of previous year break down the growth by geography n business segments, India growth was 0 n it was FMEG in domestic which grew. So, from where growth came? 5x growth came from international, FMEG grew well on topline but still no meaningful contribution from bottom line. Now, 5x international growth was not something repeteative and high one time base effect visible. FMEG with flat or lower topline dud to covid ll hurt bottom line more, so, I think there are reasons beyond corona for this underperformance. Last point, copper prices ve been down helping margins n recently there has been spike in copper prices, so, that can further hit gross margins

13 Likes

First glance at polycab Q1 Reports …

Sales have been hit drastically due to lock down

Export : posted robust growth of 116% Q On Q (** see note )

profit decrease 13 % QoQ but most of it is largely due to exceptional item of tax refund (approx 110 cr)

debt increase by 250.5 cr this can be attributed to 271.5 cr asset acquisition (##See note)

cash + liquid assets = 638 Cr

I felt the balance sheet is still strong … not sure about the revenue, yet to compare it with peers

Waiting for concall transcript to check on below details

Notes ::

** As per Earnings-Presentation Dangote Project linked sales were nil in Q1 but the CFO has complete different story to tell on moneycontrol

https://www.moneycontrol.com/news/business/companies/expect-exports-to-be-10-of-our-topline-over-the-next-3-5-years-polycab-cfo-5582931.html

acquisition → could not get any details regrading the same

Note : I am invested in polycab

1 Like

Q1FY21 concall summary:

Financials:

Revenue - Down 50%

EBITDA - Down 75% margins down 5.7%

PBT - Down 87%

-

Current situation: All factories, warehouses, and offices are operational but the larger dealers, distributors, and retailers in metros and Tier 1 towns continue to be impacted by the outbreak. Infra and construction projects executions are delayed due to labor shortage. Sales in Metro, Tier 1, Tier 2 towns are 40%, 50-60%, 80% of pre-COVID levels respectively. June had 15% lower sales while the co. is witnessing growth in July may be due to pent up demand. Growth in expected sequentially from next quarter. Incrementally, focus is to drive reach in lower tier towns, semi urban and rural where presence is limited at the moment. On the exports front, Anti-China sentiments are improving the prospects for the company visibly.

-

Wires and cables business is adversely affected due to no optic fibre cable revenues because of execution delays and Zero sales to Dangote. Positives include rising exports and increasing commodity prices

-

FMEG sales down 43% however growth revived in June. Sales for fans in April and May were lost but seeing pick up in lights and agri pumps

-

Currently received orders from large customers in Australia and the USA and exports prospects look good for the future. Dangote order is expected to be completed in 2-3 quarters

-

Growth is likely to come from Tier-2 and lower tier towns where the company is in expansion mode

-

Company is focsing more at profitability aspect also for FMEG products after the growth phase (till 100 cr.).

10 Likes

below is the response from polycab regarding the link to moneycontrol post

Dear Ramakrishnamraju,

The statement in our earnings presentation is correct. There were no sales linked to Dangote in Q1FY21. The moneycontrol article seems to have an error and we have informed them accordingly. Thank you for pointing it out. Take care and stay safe.

Best regards,

Polycab India Limited

also on acquisition → could not get any details regrading the same

got below details by reading concall Q1

acquisition :: Purchase of Ryker for 30 Cr

the status of the Ryker changed from equity accounting (Associate) to wholly owned subsidiary → which required Polycab for Line by line consolidation

this explains both debt and Fixed Assets increase by 250 cr from March 2020

7 Likes

I have a noob question regarding Polycab or any manufacturing intensive company.

How do you identify China threat? By this I mean how do you find out that there is no Chinese competition in wires and cable market?

I didn’t see any mention in Polycab AR’s risk section. Does that mean there is no Chinese manufacturer who produces wires and cables cheaper than them? Or the Govt has a tariff wall?

If the Govt is protecting the companies then isn’t there always a risk of Govt opening the gates for Chinese manufacturers that should be accounted?

I am new to investing and I have been struggling with this question for multiple companies. Some companies do mention it in their AR but some don’t. For those who do not I wish to find out how riskfree is it for them.

1 Like