Poly Medicure Limited is experiencing strong revenue growth, in line with the guidance given at the beginning of the year. Revenue grew by 23% in the first half of the year, driven by new plants that started functioning well and increased sales in India and abroad.

Margins have also improved, with operating IBITA margins reaching almost 28% in Q2 FY25, compared to 25.82% in the same quarter last year. This is attributed to the new expansions, new product launches, and efforts in the domestic business.

Exports constitute around 70% of the sales mix, with the domestic business accounting for the remaining 30%. The company aims to maintain a similar range throughout the year. Domestic business has shown significant growth of 22% in Q2, driven by increased focus and efforts in this segment.

Europe is a key market for Poly Medicure, with a growth rate of 35% in export business. The company has good visibility in Europe, with long-term contracts spanning 3 to 5 years.

The US business is expected to generate $2 to $3 million in revenue this year, the first full year with FDA approvals. Poly Medicure maintains its guidance of $15 to $20 million over the next 3 to 4 years.

The renal business is performing well, with a growth of 40-45% in the first six months. The company expects 50% growth in the next six months as well, driven by the new PMJY scheme and increased government focus on dialysis treatment.

Poly Medicure raised 1,000 crores in a QIP in the previous quarter, which will be used for new capital expenditures, corporate purposes, working capital requirements, and acquisitions. The company plans to set up three new facilities in Haryana, Rajasthan, and Uttarakhand by mid to end of 2026, focusing on renal dialysis, cardiology, and critical care.

The company has already spent 150 crores on capital expenditures in the first six months of the year, primarily for automation in existing plants. For the full year, they plan to spend an additional 100 to 125 crores on expanding capacity in existing plants.

Poly Medicure sees potential opportunities in the CDMO sector, particularly contract design manufacturing for large companies. This is due to changing US tariffs against Chinese products and increasing interest from European companies in India as a manufacturing option.

The company aims to maintain its revenue growth guidance of 22% to 24% for the full year. They are also focusing on expanding their sales force, with plans to add 100+ sales associates in the current financial year, particularly in the critical care and cardiology verticals.

Cardiology is expected to be a significant growth driver for Poly Medicure, with the company aiming for 300 to 400 crores in revenue by 2030. They are targeting the consumable side of interventional cardiology, which is largely import-driven in India.

Overall, the company is demonstrating strong financial performance with robust growth in both domestic and international markets. They are strategically investing in capacity expansion, new product development, and strengthening their presence in key therapeutic areas. The management appears confident in their ability to achieve their growth targets and navigate the evolving global landscape.

Those who are tracking this, Who are competitors in India across Renal, Oncology and Critical Care spaces across MNC and domestic manufacturers. Meril was mentioned. Who else. Where is PolyMed in this space and where on the matrix will it sit???

Q4 Commentary:

Page 3 of 16 : The balance sheet is of course very healthy. We have a liquidity position of Rs. 220 crores as of March ‘25. Of course, we are looking at some new opportunities in M&A side and as soon as we finalize something, we will definitely get back to you with proper details. So we are now constant lookout for good technology, good Company in India or outside India and our endeavor is that Polymed should be focusing more on technology in future, so that we can build solid platforms across our new verticals like Cardiology, Critical Care and Renal portfolio.

Page 6 of 16 : Anyways, Company is doing fine, we are doing. So I think the business is in good shape, is in good auto mode, but the only thing is that let us be cautious, conserve our capital, conserve our energies for a bigger opportunity is going to come to us.

Page 15 of 16: Question, On the M&A, have you been able to decide which particular vertical you would be interested in, whether it be Critical Care or Renal?

Answer: I can’t call out this. This is sensitive information. I am sorry, I can’t answer this question. We will work within what we are. We have a specialty in those areas. So that is what we will be within the same specialty area. And if we have to some new M&A opportunity, we will definitely do complete DD (due diligence) before getting into a new vertical.

Clubbing all statement: The company is aggresively looking for some acquistion.

Q1 : Page 14 of 18

Q : Which means if you look at in the first quarter, we have de-grown?

A: Yes, we have de-grown by -6%, 7%.

Q : we are saying we will grow 5% to 10%, which means the remaining nine months should be a period of decent double digit growth rate for…

A : Absolutely. Absolutely That is the point I am calling out, that we should come back to that double digit growth, high double digit growth. And that is what we are also calling out again.

Q: Also domestic grew in the first quarter by 20%, but yet in entirety, we are saying we should grow 30%. That means the nine months we should grow well over 35% to make that happen

A: That is that is already on the card. This is already under the process. Because we have started two new divisions last year and these two divisions have become active. So, the cardiology and critical care. So, they are ramping up as we have talked about a stent deployment from 1,300, 1,400 stents to go to 20,000 stents by the end of the year. And then critical oncology segment is

growing. And then our renal segment is growing, is growing at a healthy rate. So, all in all, domestic and we are hiring 100 people in domestic market, 22 already been hired in the first quarter. So, as all in all, I think and but in the private sector, we already grown 25% in Quarter 1 in private sector, which is 90% of our business. So, overall, the ramp up is already happening.

Solo-Dex And Polymedicure Partner To Bring Opioid-Free Acute Pain Management To India And Major Asian Markets

Solo-Dex, Inc. and Poly Medicure Ltd. have partnered to manufacture and supply Solo-Dex’s opioid-free regional anesthesia solutions in India and key global markets. The partnership aims to bring Solo-Dex’s patented, continuous peripheral nerve block system to hospitals, supporting Enhanced Recovery After Surgery programs and outpatient surgical care.

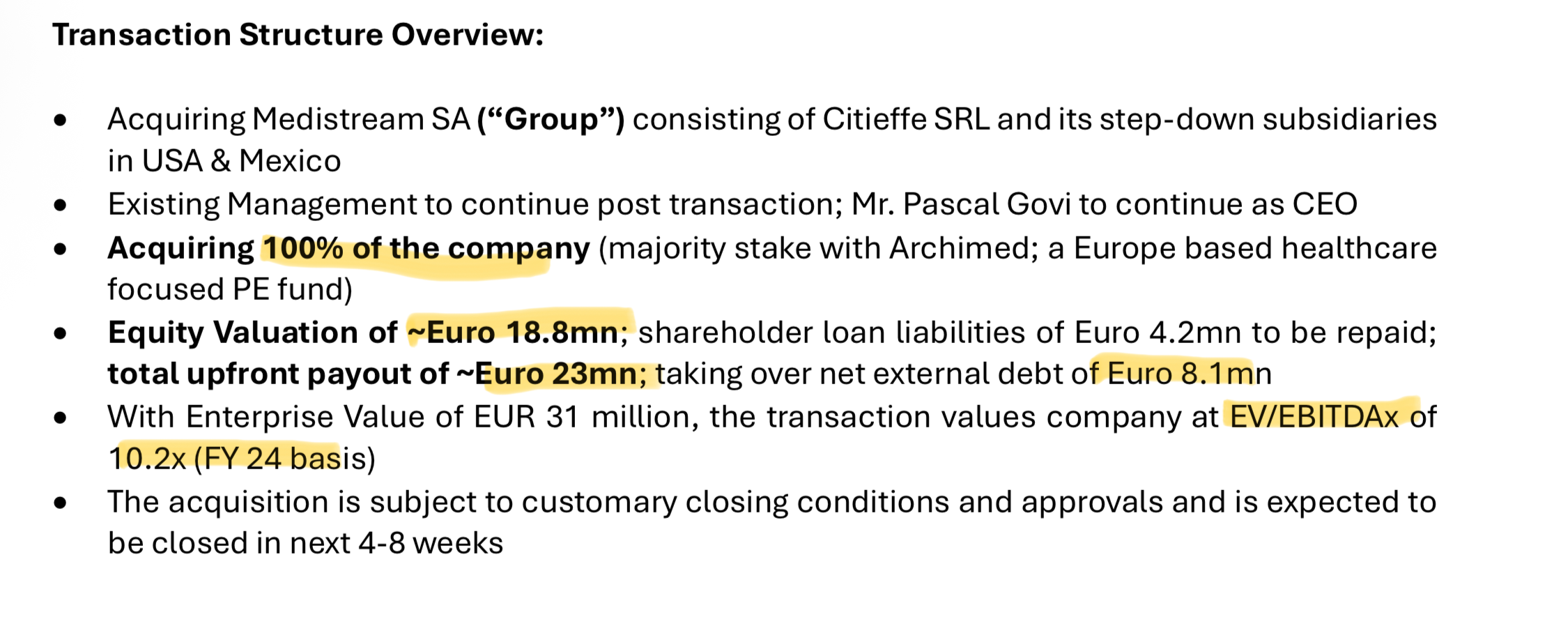

Page 5 of 12 : This transaction starts the journey for Polymed in the orthopedic space is the new adjacency within the medical devices space, which Polymed has entered into on top of cardiology, critical care and renal care that we’ve entered in the last 5 to 7 years. We believe that orthopedic is a very attractive space with significant growth potential over the course of next many, many years. And we believe that Citieffe is the right kind of platform for us to use and expand in that space.

Page 6 of 17 Q3 : We have ended the quarter with liquidity of Rs. 1,109 crores. This strong cash position allows us to continue backing off our ambition growth strategy both organic and inorganic. Of course, after completing the Citieffe acquisition which we have done by 6th November, 2025 the net cash position as

on date is close to around Rs. 800 crores. As mentioned earlier, we have completed 2 acquisitions in this quarter and further thesis focuses on technology acquisitions that complement our verticals, Critical Care, Cardiology and adjacencies, we will keep the market inform as we move forward with new

opportunities.

Now, let me share the guidance for current quarters in H2:

If you look at the current domestic market, we are still very bullish that we will end almost with a growth of 28%-30% for FY '26. So, we currently reiterate our guidance. For international business, we are now guiding for revenue growth in the range of close to 10% including revenue from 2 acquisitions. This revised outlook reflects the current global market conditions underlying uncertainties. We will keep you all updated as we gain greater clarity on the evolving environment. We maintain operating EBITDA guidance in the range of 25%-27% for the year. As you have seen, we are close to around 26.5% on the upward segment of the bank. We continue to invest in future growth. CAPEX of Rs. 150 crores was done

in H1 and we further informed that CAPEX planned for the current financial year will be over Rs. 250 crores. This fund will be deployed to set up the facilities at Mitral and Haridwar as well as to expand capacity at existing plants. We expect these plants to be fully operational within the next 12-18 months. It is worth emphasizing that the guidance is built with a measure of conservatism, particularly around exports, given the current geopolitical macroeconomic headwinds. However, we remain confident with our strong product line, upcoming launches, and domestic momentum, all of which we believe will comfortably offset this segment.

In summary, Q2 FY '26 has reaffirmed the fundamental strengths of our business.

been studying this company for last few days.here are my thoughts:

1)the question of why the company did not grew faster like it is doing after covid after mar2015

my thought process is medtech is asset heavy industry and company was capital starved after paying a consistent dividend payout: (2014-now)

same confirmed by the management in q3 fy25:

fyi q3 fy25 is a goldmine of information into the company.

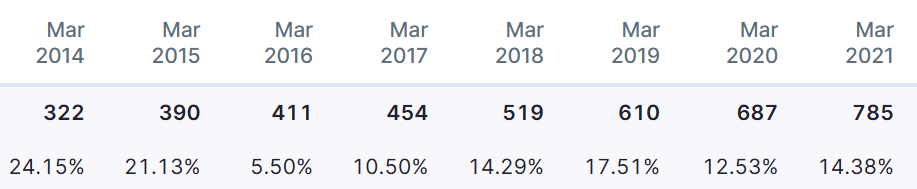

so in summary when they did two fund raises which helped the company to enter into the 20 per revenue growth orbit.so to confirm this this is the fixed assets: (from 2014 to sep 2025)the fixed assets grew much faster compared to 2015 -2020.also one more point is they have reduced the dividend payout which is a good thing because raising qip and giving dividend does not make sense.

2)so now on the growth part right US was their decent aim in medium term 20 million dollar sales but trump govt discredited all medtech certifications from india which did their validation in india labs.so this will take much time to start revenues.

3)so now they have acquired two companies in europe which they can absorb and cross sell.

4)management mostly after covid has hit their guidance or sometimes over hit the target too reflecting in sharp rise in share price growth.

5)although looks good as a company valuations are elevated.

views are welcome for any further optionalities.disc:not a financial advise only for educational purpose.

Thanks for a good write up. I myself come from Class-3 medical devices company and know this space/challenges quote well.

New products/markets need an approval process from various authorities. Compliance is a big factor as well. Every new production line/equipment/tools/machines need to be qualified and validated. Once everything is submitted and approved then companies need to go for bidding phase and if they are successful then they could start selling.

I very much welcome the acquisitions in Europe due to their expertise, capability, compliance mindset, local language force/support (Important for Europe) etc. It would take some time for gestation period but once the synergies are aligned then it would help bring back the growth.

Hope this is helpful. Also, studying. Will check Q3FY25 concall.

Disclaimer : Not invested. No recommendation.

Yeah unlike any other industry medtech has high gross margins which lets them to acquire European businesses and continue the operations.for example their italian subsidiary which I guess they acquired in 2019 now does73.93 crore revenue(ending 31 dec).so their new acquisitions in Europe atleast won’t face losses in my opinion.so downside is very limited for polymedicure if they fail.

Also below points which I don’t like about the company .

The company spent only 1.47 percent of its revenue on r&d .I mean too less amount in my opinion because it stresses a lot on r&d in its annual report.so which comes to about 24.57 crores and in this 10.16 crore is the salary of r&d people rest is consumption of materials in r&d.

Second is very high salary of the himanshu and rishi combinedly they take home close to 41 crores.each close to 20 crores.this is. Extremely high in my opinion .