Reading this business recently, and observed that the salary hikes of Mr Himanshu Baid and Mr Rishi Baid are close to 50% in FY21, which seems to be very high. Also, the salary of the each of above is close to 10cr compared to 180cr profit. Is it normal?

4 Likes

It does seem like a red flag to me. I am an amateur investor so could anyone please explain why the 1)high management salary and 2) Promoter role in VITROMED, are not red flags?

Disclosure: Not Invested, Just learning

1 Like

Is there any negative news or changes in fundamentals for Poly Medicure? 50 DMA < 200 DMA since quite some time.

Below is my understanding of this stock.

- March quarter has recorded highest sales ever though the OPM is 22% which seems good too. After reading concall and thread forum, the management aims to achieve 30% margins in next 2-3 years.

- Valuations were peak at ~1200 in May’21 have now fallen to ~740 levels and PE is below 1 year median PE (source - Screener)

- What I know is medical equipments can be good proxy play to both diagnostics and hospital industry as I don’t have to think about unorganized sector these 2 industries have.

Is there anything missing in my analysis? Fairly new to fundamental analysis. Would love to learn more.

2 Likes

as per company law not more than 11% of PAT can be the total remuneration of the directors, which in this case stands at 16 crore. so yes this is a red flag

1 Like

Polymedicure --Q3FY23–Earning call Highlights–CNBC interview–24th Feb23 :

–Revenue growth was 24% YnY & Margin expanded in Q3FY23.

–Good growth in exports from Europe which is growing around 25% YnY.

–Domestic mkt growth is muted at 15% as last year the growth was due to lot of covid products , If we remove covid products the growth there is also 25% in that segment

–Overall a growth of 21% in 9M and we will see a similar growth & next year we will see aa growth of 20% from FY23.

–Margin improvement guidance --FY23 will continue to improve in margin in Q4 as well as RM prices have come down a lot because most RM was imported and had an petrochemical base so prices have dropped from a Peak of May/june22 to now the prices have dropped by 30/40% & similarly the freight cost has come down compared to last Year

& currency will have a better role as we have 70% export revenue so overall we will 100/200bps margin improvement going forward

– We are only in consumable Biz , so our consumables are used in oxygen therapy so that was a big last yr in India & outside due to covid but this Yr the demand has dropped off. Now the growth is from Infusion therapy and Renal segment right now.

–US Biz , we are waiting for US FDA approval and final filing will happen in week to 10 days & after that revenues to start from Q2FY24. We are still doing US biz at 1Mn$ but once we get FDA approval for some new categories of products we will see a huge ramp. & China+1 is helping as lot of co.s looking for Indian Mfers.

–The US FDA approval we are expecting in Infusion segment & US is a high margin geo & we will see higher margin from this product in US. Our Europe and US margins are similar & Africa and Asia margins are lower so that will help us improve margins when volumes grow and most of these products are patented devices so we will have better profitablity in these kind of products

–US contribution to current revenues --its currently over 1Mn$ & once we get the US FDA approval on these products we will do in 3 to 4 yr window we will see revenues going to 10/15 Mn$ as a rough estimate.

–China dumping of products in renal Biz --Most of these chinese cos are misusing the FTA & they are setting Psudo mfring facilities in Thailand or Malaysia 7 from there they are dumping products into India and getting duty waiver as those countries we dont have any customs duty on imported products. 2) Most of the co.s are selling products below the import prices in India so there is clear strategy is to eliminate Indian Mfring & that is where we are struggling.

–Also , there is very little GST on these products as when we make in India we pay 18% GST on mfring RM but finished product GST is only 5% so when Chinese bring the product to India , they have just 5% IGST and we pay almost 18% on our input and 5% on our Output so we have lot of inverted duty structure on the products.

–We have not Lost mkt share but the growth which we anticipated of 50/60% , we are probably getting only 40 to 50% range in FY23. So that has hampered the growth a bit & the product is also part of the PLI scheme so we are going back to govt and telling them about FTAs & inverted duty structure otherwise the Chinese will keep on dumping the products in Indian mkt

–Dialysis biz which we hoped to grow at 50/55% in FY24 will only grow at 30/35% due to This issue with Chinese Dumping.

14 Likes

This news could be a game changer to control China dumping:

4 Likes

The Union Cabinet has approved the Medical Devices Policy, which aims to increase India’s share in the global medical devices market. Himanshu Baid, MD, Poly Medicure discusses this policy in detail on CNBC TV18.

6 Likes

I am skipping this company because

- Promoters has unlisted subsidary Vitromed healthcare which manufactures same products.

OPM growing, sales growing but ROCE falling YOY , may indicates siphoning off money.

Risk of repeating story of manpasand beavourages. - All medical devices to come under controlled price so OPM to reduce further.

5 Likes

I am gaining my knowledge about the medicat device industry.

You mind please sharing any evidence to support your pt. 2, ? Any other country also doing controlled pricing, any clue?

It shouldn’t affect export pricing I feel…what do you think?

1 Like

-

Export to Europe has increased by 40% compared to the previous year

-

A lot of expansion is happening by the end of FY2024.

-

Spend 500 Cr on a new expansion that includes four new manufacturing plants

-

Maintain a steady growth rate of over 20% in quarters

8 Likes

Poly Medicure is advantage of certain MOAT.

- EU Plus strategy.: CE Certificate for Plaster device under NEW MDR.

CE Certification ensures that products meet all necessary safety, quality and standards required by EU.

Plaster device a single product but once company is habitual of such kind of certification, they will be trying to more products come under this certification (Interesting to see in future)

2.Import Substitution strategy (page 3 of 13 of Q2): further strengthening our India business as I said with two new divisions adding more people almost 100 people we will be adding during the year and out of this 100 people around 25 will be

from the clinical side will be nurses and clinical application team so we are continuing to solidify our clinical application team so that when we are launching new products, we are able to go strongly to hospitals and talk about clinical advantages of these products and most of these products will be import substitution products and they will have more higher margin compared to our existing products. So we are building that whole network and infrastructure to launch these products.

3.Banning of Unregulated products by new Laws.

- Management reply on Surplus Cash :

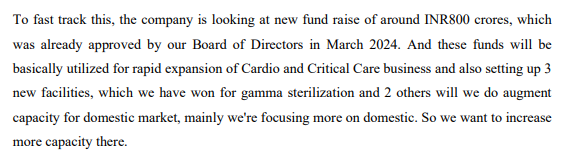

Himanshu Baid: So I think this is a very capex heavy industry and needs constant investment so we have to up our anti on R&D as we get into cardiology and critical care we have to increase our spending’s on R&D and bring in some new capital equipment for R&D so we have to work in that direction and this medical device industry if you look at the global industry it grows through acquisitions and

MNAs and we have done one acquisition in 2019 and I have talked about a few minutes ago that how important it is for us in terms of oncology products, and it is growing very steadily so if we find any new opportunity, we will definitely deploy our surplus crash into this new opportunities.

5 Likes

Information Purpose adding here ![]()

Why Get CE Certification in India?

There are many reasons to get CE certification for your product. CE certification ensures that your product meets all the necessary safety and quality standards required by the European Union. This can give you a competitive advantage in the marketplace and make it easier to sell your product in Europe. It can also help you to avoid costly recalls and legal problems.

CE marking certification is mandatory for many products sold in the European Union. This includes products such as electrical equipment, toys, medical devices, and construction products. If your product falls into one of these categories, you must get CE certification before you can sell it in Europe. The CE certification procedure can be a complex and time-consuming process. However, it is worth the effort to ensure that your product meets all the necessary safety and quality standards.

4 Likes

Poly Medicure Limited Q3 and 9 months FY-24 Earnings Call February 02, 2024

-

We see that we should be able to grow 20% over also in the next fiscal year

-

In the current 9 months, we have seen that domestic business has grown by around 18%, and export business has grown to close to 24%

-

We should grow by over 50% for the next year because we now see the traction. We are already investing in new capacity build-up, which will help us reach this new revenue number of INR140 crores to INR145 crores for the next fiscal year.

-

Earlier, the machines are around 35% made in India content. And now the new machines, the next generation of machines are around 50% made of made-in-India content. This is a big milestone because this will allow us to now participate as a top-tier supplier and a lot of government contracts. After all, there’s a preference for companies with 50% local content.

-

The Italian subsidiary has done well. And Italian subsidiary has grown the business by around 50%. And also the company has generated approximately a PAT of around INR7 crores over 9 months. In the same period last year, it had a loss of around INR65 lakhs. So I think there’s a big turnaround with an increase in revenue and also the profitability. And I think we will continue with the same momentum. And next year also, I think we have plans to grow the company by around 35% to 40%

-

We have launched our critical care division in India. There is a soft launch already done. Also, we’ll be doing a soft launch of our cardiology business this month

-

We have done close to around INR185 crores of capex for the first 9 months. And key plants are already ready, and they have started functioning, and we’ll be in a ramp-up phase now. The fourth tranche will be ready by early next year, early next year means the financial year, maybe in April, or May.

-

We have grown again 40% in quarter 3 in export in Europe business, which is, by far, still the biggest market almost 40% to 42% of revenue comes from Europe for exports. So if you are splitting the revenue again, we still maintain the same split of 1/3 India, 1/3 Europe, and 1/3 rest of the world.

-

In the last 9 months, we have been granted 19 additional patents. The patent portfolio is now over 375 patents

-

In 2024, we plan to launch around 8 to 9 new products. Already the work has been going on for these products

11 Likes

- We should grow by over 50% for the next year because we now see the traction. We are already investing in new capacity build-up, which will help us reach this new revenue number of INR140 crores to INR145 crores for the next fiscal year*

This is in reference to Renal Business: Which one FY24(E) Rs 90 Cr and FY25(P) 140-145 Cr.

3 Likes

- Medical Device and China Market outlook: Chinese companies would be exporting close to $75 billion to $100 billion of medical products. These are different from a needle to an MRI machine and the number could be even bigger. A lot of U.S. companies are based in China, they have their own

subsidiaries, and they cater to their own parent companies. So the market potential is huge out of China, which could go out of India. And what I’ve heard

in different corridors and people talking about is that they want to move like 30% business out of China in next 2 to 3 years. And that is where I see a big opportunity for Indian companies. It’s India’s infrastructure, India’s supply chain can cater that whole manufacturing ecosystem, I think India is in a great place to take that market share. - How many number of angiographies done in India ? Answer : Almost 20 lakh angiographies are done in India today and most of the products used there are imported. So for us, the market that is the big size of the pie. And that is what we are targeting today that what are the catheters which are needed for angiography, balloon caterers or diagnostic catheters or

guidewire or anything related to interventional cardiology. That is where we are focusing on right now. So our major focus will be on these kind of products. And then we will probably get into more, let’s say, complex products going forward with radio sheets or something with a femoral sheet or something else. So that is what we are trying to build in as a business.!!!

We see a number of cardiology patients; cancer patients and renal dialysis patients continue to increase in the country and then also the critical care infrastructure of the country is also getting augmented after COVID. A lot of focus has been there on the critical care side, where we had shortage of critical ICU beds. So in critical care sales also, we see a significant growth. The company has been focusing on a few of the areas earlier, but now maybe more focus and will be adding more products in this category of products in the next few years. - The guidance for the current financial year is to grow at the same pace as last year. So again, we are guiding for revenue increase of around 22% to 24% in the current financial year (FY24 Guidance was 22-24% and actual delivered 23.6%) And also as we see more operative leveraging or leverage coming our way, we are guiding for a better EBITDA margin in the coming financial year, improving by around 100 to 150 bps. ( FY24 EBITDA 29.07%)!!

9 Likes

Poly Med has came up with Q1 Fy25 result. Revenue and Profit growth is there.OPM sustained at 27%.Company hardly generate any free cash flow as going through agrresive capex phase. Like any decent mid and small cap in Indian market valuation has been taken to different orbit. PE hovering at 72 though Poly med is growing at rapid rate. But one thing in result footnote is catching eye , in current quarter Poly Med has received a CGST demand notice in the tune of 42.38 Cr. Poly Med is going to challenge the demand.But nothing to conclude yet. Tax dispute is very normal for Indian companies and without any resolution for very long time.

[Invested at lower level , no plan to add/sell for now]

4 Likes

Business Updates

- The first phase of capacity expansion is over and new machinery has been added which has enhanced capacity from 1.2 billion units to 1.5 billion units which will be further enhanced to 1.8 billion units by the year end for medical devices

- Renal, cardiology and critical care remain the focus area for the company

- Once the gamma sterilization plant is complete the company will move on to this process on its own which is currently being outsourced

- The company is investing in AI based tools for its sales people which in training has been seen to help the business

- The first sale of infusion products in USA has started and hopeful that the new equipment will be ready by end of the year. There are 4 FDA approvals already and 8-10 new approvals should be in place in the next 12 months

- The outlay for the PLI scheme is too less to make a difference and has not helped the equipment industry as of now and the company continues to work with the government to change the modalities of the scheme

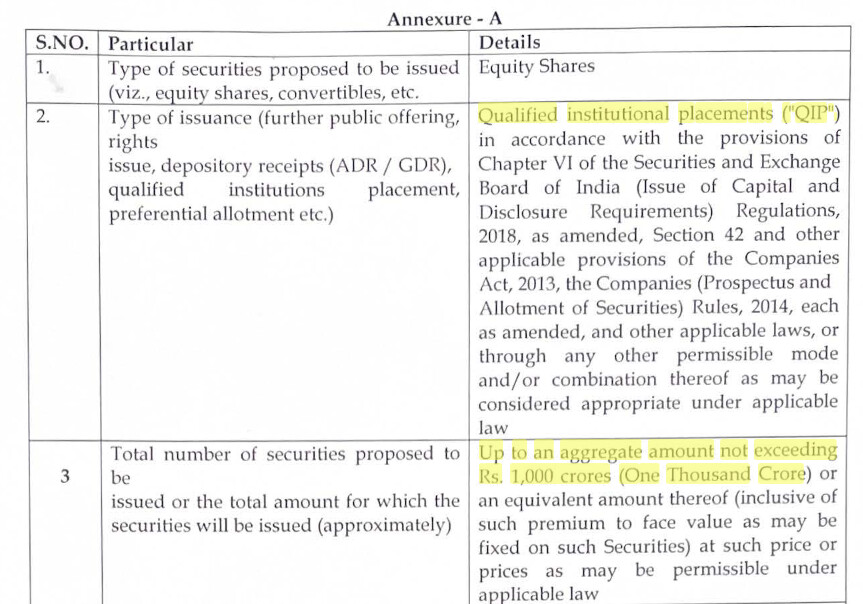

- The board has given an approval to raise up to Rs 1000 crores through a QIP which will be utilized to build 3-4 new facilities and this money will help in scaling up faster. The fund will also be used for technological capabilities to enhance the cycle of introducing new products faster to the market. This will be via inorganic route

- There is keen interest from foreign investors in medical technology space and post covid the fund availability has improved drastically

Participants

Ambit Capital

Elara Capital

KGMG Finserve Group

Dalal & Broacha

ICICI Bank

Bonanza Portfolio

QnA

- The Vision 2030 is focusing more on how growth can be faster than what is being seen in the domestic market and growing at 20% plus versus industry growth of 12% through import substitution

- The coverage in India hospitals is still at 40% and there is scope for deepening the engagement with the existing hospitals

- The infusion products have a share of 60-65% to the total revenues of the company

- The guidance for FY25 for capex remains at Rs 250 crores

- The capex from next year will be Rs 400-500 crores yearly for the new growth that is envisaged

- Q1 has seen a 40% growth for the dialysis business and the target for the whole year is around Rs 130 crores

- Almost 60-65% of RM is still imported and there are almost 250 suppliers all across the world and hence an inventory of around 2.5 months is kept. On the finished good side no inventory is maintained for exports while for domestic market 1 months is maintained

- All the four new plants will be at new locations near the current plant but not at the same location

- There is a two year time line in terms of construction of a plant and getting all approvals in place for the plant to produce and sell and the approval for exports is even higher and thus the timeline from completion to getting approval is 4-5 years for a new plant

- The plant in China is being closed down because the lease period will expire in 24 months and the cost structure is higher than that of India plant

- The main areas in which products will be sent for FDA approval is vascular and critical care

- The locations of the new plants will be Jaipur, Faridabad and Haridwar and one new plant in a medical park can be setup

- In terms of volume the company has 10% market share in the world in the IV canula business

10 Likes

can a supplier royalsense and qmsmas be compared this manufacturer ?