Respiratory care products - Oxygen masks, Oxygen tubes, endotracheal tubes, Ventilator circuits seeing big spike in demand

Blood collection and VTM kits also seeing 3-5x spike in demand

Ramped up capacity to cater to demand but still not able to keep up

Capacities are fungible so ramping up capacities of products seeing higher demand and reduced others like surgery related

Considering Oxygen-concentrator as a new product (Trying to develop in 2-3 months)

Syringe capacity also increased to keep up with vaccination demand

Insulin syringe and pre-filled syringe capacity reduced to make space for normal vaccination syringes (Seeing demand sustaining over time)

Demand is unprecedented so plants are running 24/7 and RM supply is continuous and no supply-constraint or delay with vendors

QIP money put to use for Renal products. Got PLI approval as well from govt. for the same until 2024. 95% of Renal products and consumables are presently imported in the country

This is not a good sign from a humanitarian standpoint but the business is able to cater to the demand and make a potential positive impact which is good. They seem to be agile on their feet in terms of changing product mix and keeping things running

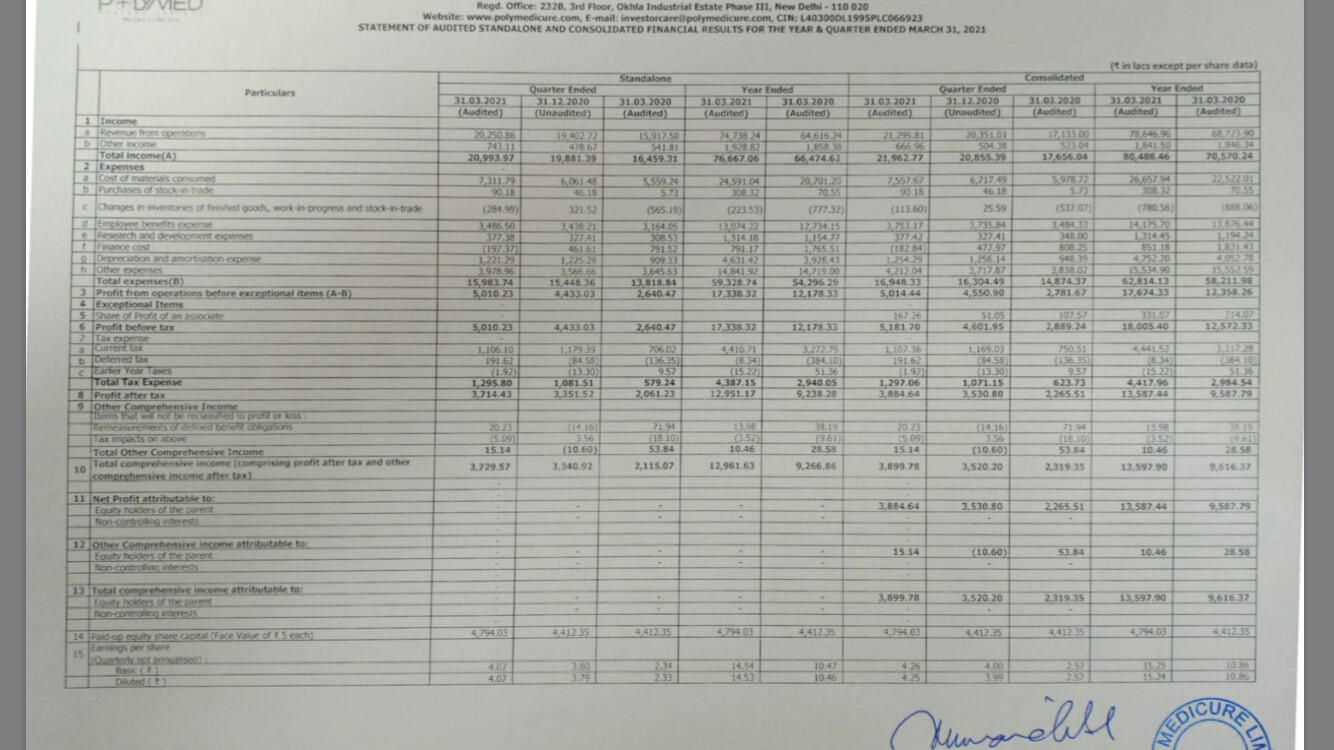

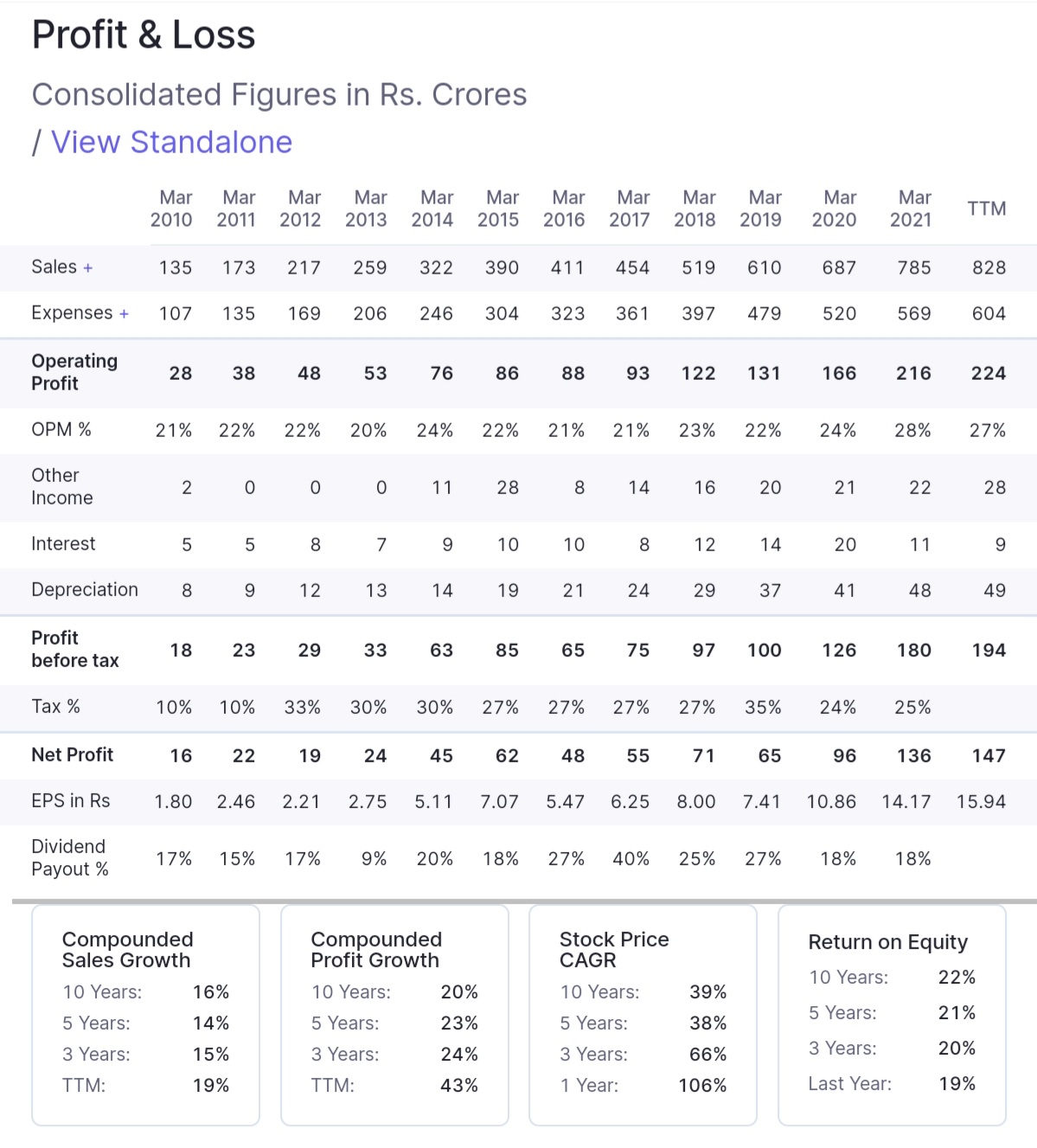

Topline grew by 11.44 percent and bottom line grew by a healthy 41.66 percent.

Why did the market react so adversely (-7.35 percent)? Was it because of the unutilized Rs 330 crores part of Rs 400 crore QIP?

with full year EPS of 15 at the current market price of 1050, it comes around 70 P/E multiples. Market was expecting better earnings and sales and considering this stock as expensive.

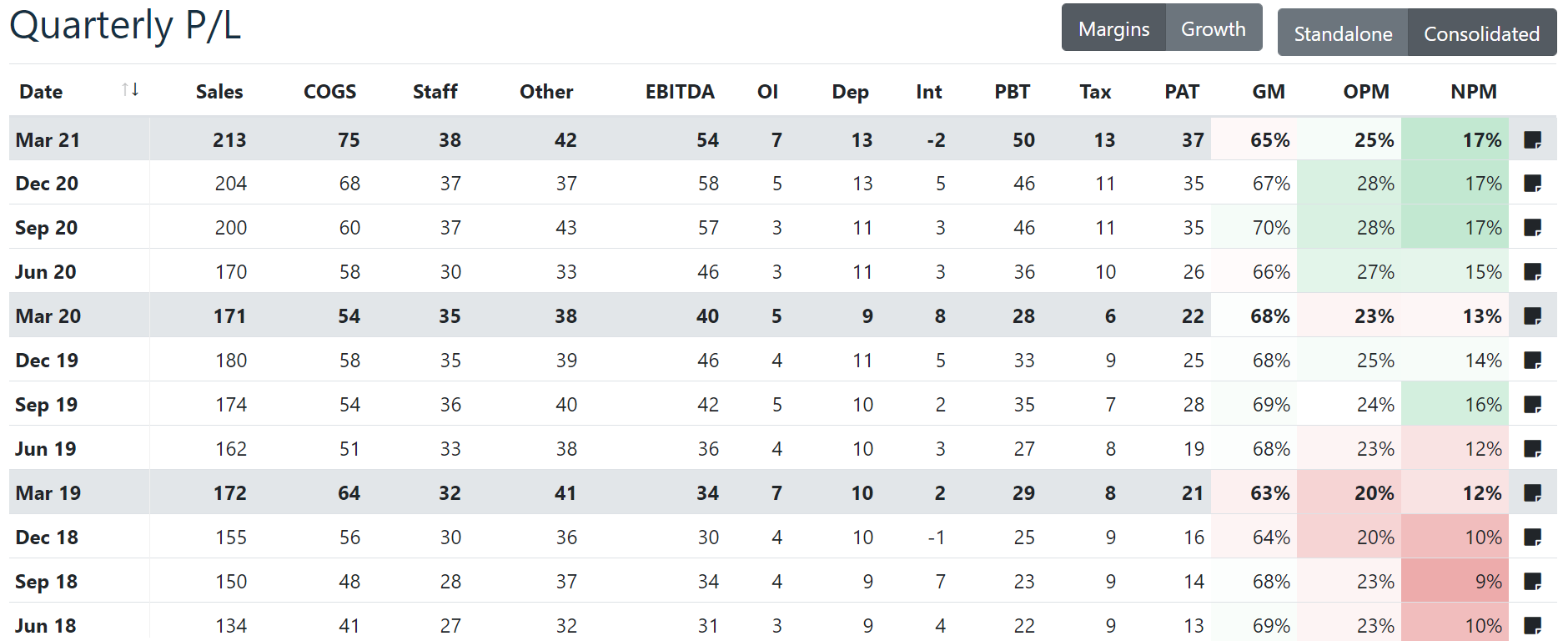

Steady numbers. Gross Margins are bit down QoQ leading to lower Operating Margins as well. 25% may be the normalized EBITDA margin. NPM is stable at around 17% (There’s an interest adjustment which has compensated for the reduction in margins).

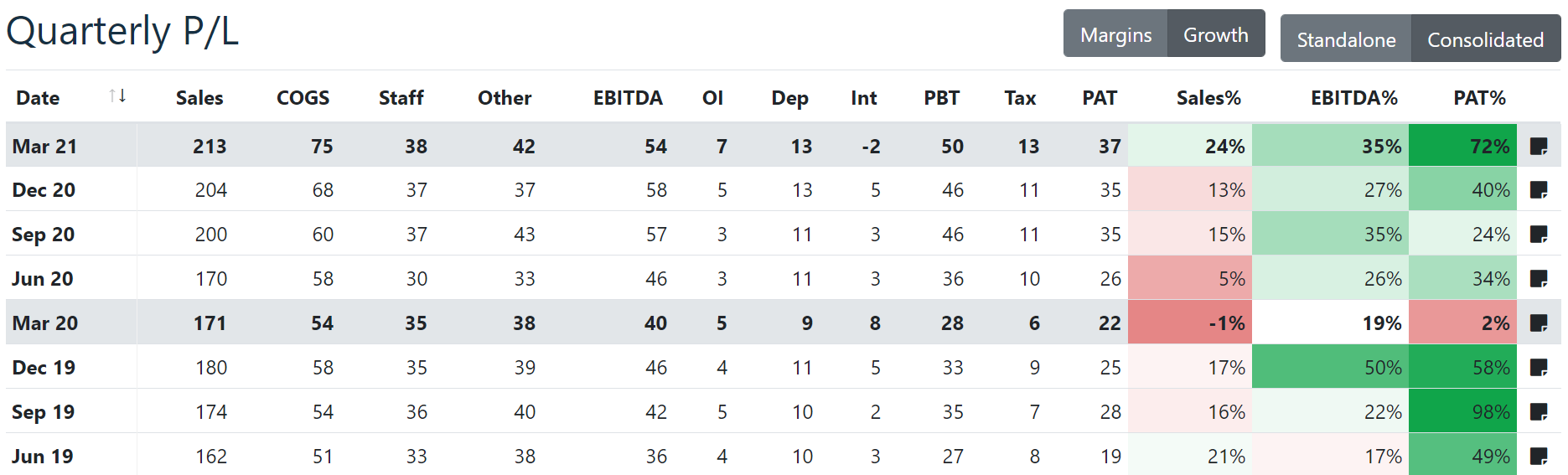

Sales Growth at 24%, EBITDA growth at 35% and PAT growth at 72% shows an acceleration in the growth even compared to last few quarters. The Covid demand growth from 2nd wave might show up in Q1 numbers and could aid as well. Also worth noting that EPS will be depressed due to the dilution despite the robust PAT growth as this QIP money is yet to contribute to numbers and won’t contribute until FY23 though the shares are already issued and EPS is calculated based on that.

The company seems to have paid back some debt as LT debt is now reduced from 114 Cr to 63 Cr (even ST is reduced from 53 Cr to 39 Cr). The proceeds from QIP aren’t yet showing up in CWIP (still under Investments) maybe because this is the snapshot of Balance Sheet as of Mar 31, 2021. The management had mentioned in a recent interview that Renal PLI capex is underway as of April.

Also worth noting that the book value of the company has increased from Rs.45/share to about Rs.100/share as of FY21 (aided by QIP proceeds as well).

The valuation of the business though is expensive now and there is no margin of safety for anyone trying to get in. Price is being set by short-term traders so someone with a longer-term view must wait. I think Rs.900/share might be fair value.

Disc: Invested from 230 levels. No recent transactions

Thanks for link for concall.

But one thing is sure - Poly Medicure is not a COVID story.

Yes. It got the healthcare sector tailwinds by luck due to COVID.

Its long term growth story fueled by increased healthcare spend by government & increased medical insurance penetration.

They are more into IV canula and now dialysis business.

With GST and strict healthcare guidelines ( for medical products) , this is poised to gain more market share from the unregulated and unorganized medical products sector.

Disclosure - I was lucky to start investing in it at 250 and have averaged around 500. Still holding with patience.

This should take some breather for now and further movement will depend upon its next 2/3 quarter results,

Regards,

Dr. Vikas

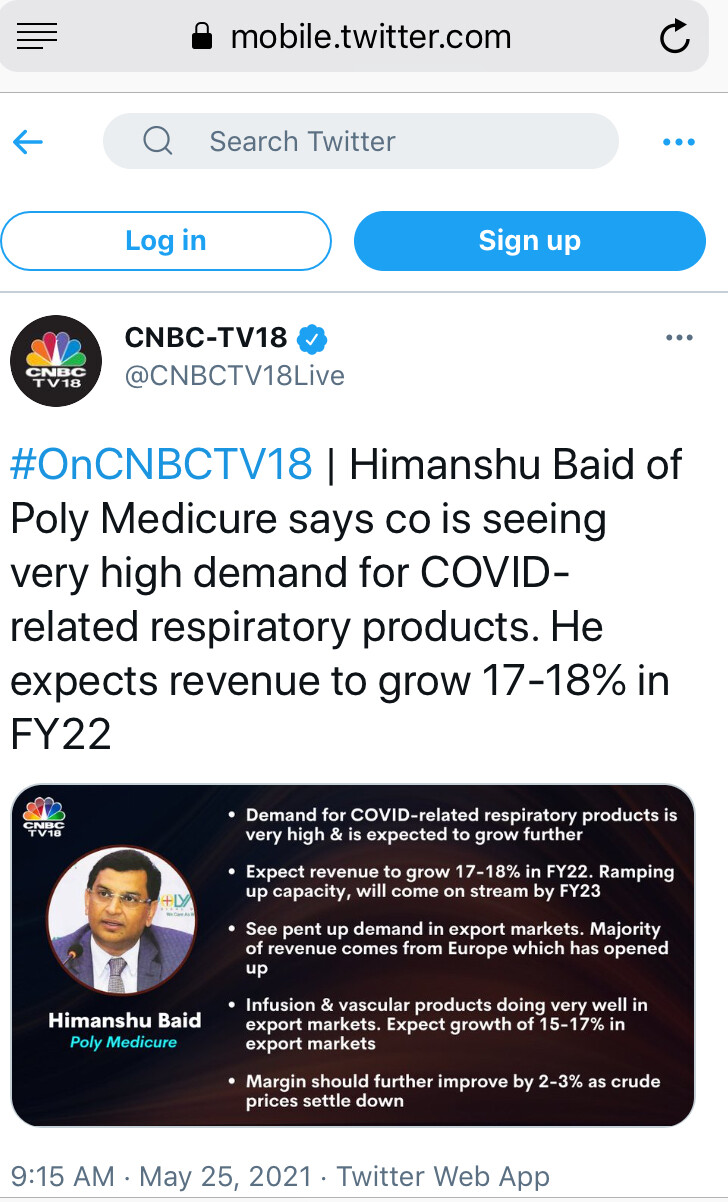

My thought process is, the company could have performed better if the impact of Covid is not so severe in Europe. 2nd wave in India will be a tough quarter with 60-70 percent attendance. They are entering into a low value business like manufacturing of generic syringes, their GPM percent will deteriorate further. What is promising is, in 5 to 6 months from now, they may get US FDA, they will get access to bigger market.

Next quarter projection, better than Rs 170 crores (Q1, 2021), did not tell how much better will it be, promised yearly growth of 15%

From 2023, company will have substantial growth

Disc: 6.5% of portfolio, invested at lower levels. My opinion here is biased

Very true. I am also surprised by their decision to enter into generic syringes, where other established companies like HMD, Braun have bigger market share.

Now with this stock in limelight, it all depends on how the Management delivers?

Regards,

Dr. Vikas

Absolutely true. But Market is always FORWARD looking.

I think , this stock may undergo a time correction or even price price correction ( if the Management doesn’t deliver)

Fresh entry should be avoided - Personal Opinion.

Regards,

Dr. Vikas

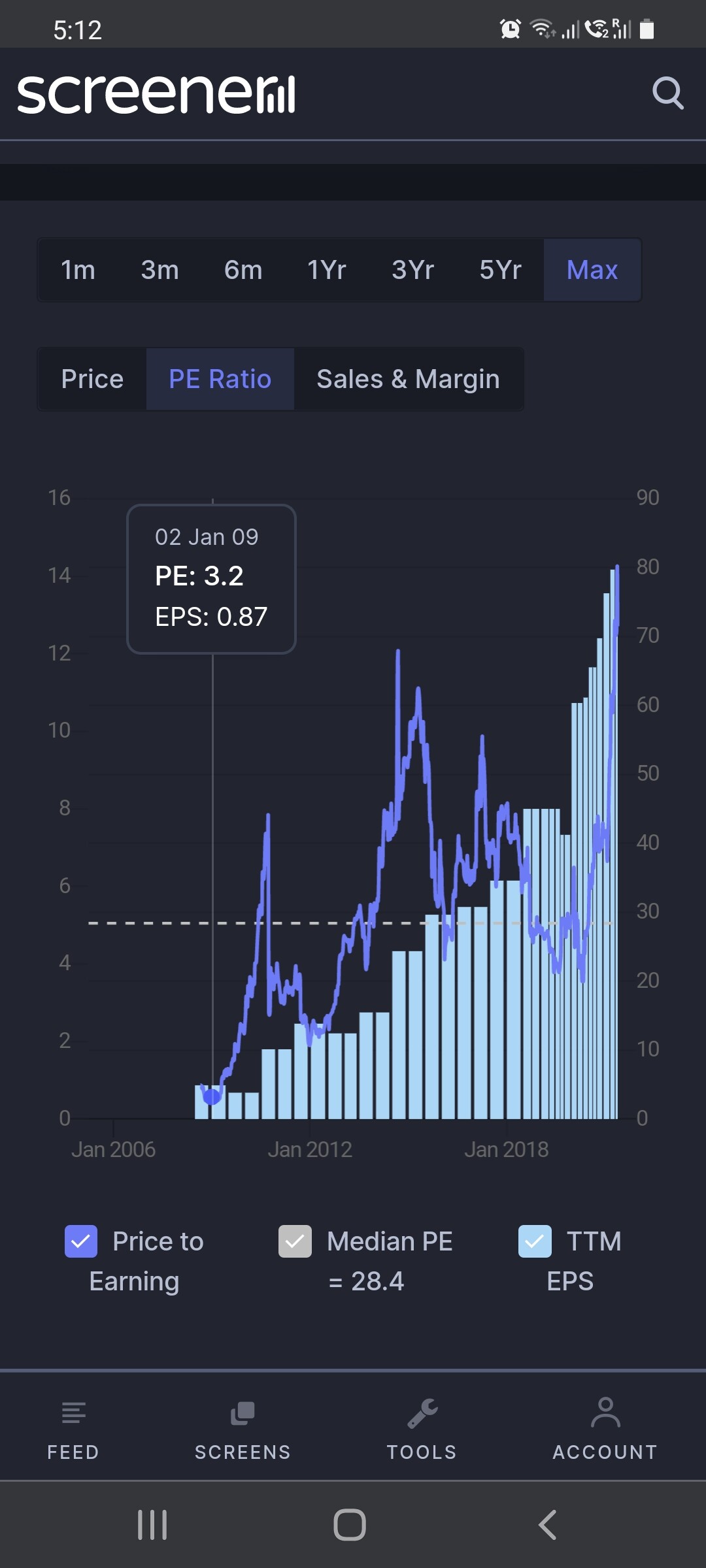

The earnings have compounded beautifully in the last 12/13 years. But so has the pe ratio. However I can see 2 derating events right after major rerating events. Could this time really be different? Every investor must make their own judgement call by studying fundamentals,.tailwinds, capex plans, future growth triggers like pending US entry and also the reasons for the historic deratings and analysing.

Disclosure: I used to be invested because company is absolutely amazing business and industry definitely has good tailwinds but recently sold out due to valuations and the opportunity cost it implies in case of derating. Also, I really could not have deployed incremental capital that I get from my salary at these valuations so had decided to sell. However this is not a buy or sell recommendation, everyone must do their own analysis.

Absolutely agree - this combination of a very high PE multiple coupled with record earnings does look stretched.

On the concall Mr Baid guided for 15-17% growth himself. Even if they meet guidance - will the PE multiples remain at similar levels? Even if they do - is there scope for future share price appreciation?

I anticipate next quarter results to be great but also looking at the levels of the small cap and midcap indexes - feel worried about even good companies there in the short term when the current exuberance passes by.

That said - good company and good business - no doubt it can do very well in the long term - just the downside for me currently seems too much - and hence I exited as well.

Discl - Was invested, exited completely yesterday, will continue tracking

If the company makes a very valuable acquisition in the next couple of quarters, I would tend to believe company will be valued higher, depends on management’s execution. If Indian government regulates renal products, that makes the stock even more exciting.

Disc: Holding from lower levels. Very biased and wishful thinking views

Past performance on sales and profit - been a consistent performance , grown in FY 21 as well, this is irrespective of Covid driven Healthcare push for coming decade. Margins were on improving trajectory over years.

Company has delivered 1.1-1.2X Over gross block over last many years. FY 21 gross block being 782 cr.

FY21 - 800 cr sales, 28% margins ( slightly higher than past averages), 136 cr profit( this is without MEIS benefits, with RodTEP coming back , will help margins thus bottomline), TTM profits at about 150 cr - There is higher depreciation as well in recent quarters due to ongoing Capex

FY 22 a growth guidance of mgmt at 18% puts numbers at - sales 1000 cr, Opm 26%( lowered a bit), Profit around 160 cr( sizable ongoing Capex with 400 cr QIP - 300 cr is likely Capex - 200 cr type in current expansion and 100 cr type for inorganic - per mgmt recent interviews - approximation )

FY23 - with Gross block at around 1100 cr + ( about 782 cr in FY 21 + QIP driven), they can deliver sales of 1300-1400 cr, with OPM of 26-27% , 225 to 250 cr profits.

Current mkt cap is 9500 cr. Considering CWIP it is not that expensive being in sector with tailwinds, of course not cheap either. Further rerating triggers may not be there but has ability to give 15-20% CAGR performance over Medium term.