I have been tracking the shipment data of Pokarna & other shippers from India. This scuttlebutt provides a trend of the quantity of material shipped from time to time.

These are the trends I found from https://www.trademo.com/ (you can verify them via their demo version)

As far as I know, DHL Vizag also ships exclusively for Pokarna and I have taken their numbers into consideration as well. These are the trends which have emerged:

Dec 2020: 9.67 lakh kgs

Jan 2021: 12.46 lakh kgs

Feb 2021: 11.45 lakh kgs

March 2021: 13.15 lakh kgs

Apr 2021: 19.22 lakh kgs

May 2021: 12.80 lakh kgs

Jun 2021: 21.59 lakh kgs

Jul 2021: 18.39 lakh kgs

Aug 2021: 19.5 lakh kgs

Also a relatively new shipper Globeline shipping, Hyderabad has emerged which eerily coincides with the commencement of Pokarna’s new facility in Hyderabad. Globeline has shipped 14 lakh+ kgs in Aug 2021 alone(I doubt if any other player except Pokarna can ship this much) and a few lakh kgs in June & July.

Please note that these figures can only be used as a way to figure out the shipping trends and cannot be construed as final indicators of revenues. Also, in these figures, I may have missed out on other shippers which might have earlier shipped on behalf of Pokarna and aren’t doing that right now.

Disclosure: Invested and bullish on the stock. Please do your own research for taking decisions.

Globeline shipping is a Qatar based company and they are operating in india since 2009. check out the link below. so they do not seem to be a related party for pokarna. Globe Line Shipping Services

Yes, you are right. But they are a shipper of products and not manufacturers, something similar to DHL. And they have started shipping quartz surfaces from Hyderabad, India recently(what I meant by ‘a relatively new shipper’) with decent volumes as per Trademo. And what they ship is definitely produced by a manufacturer who can produce decent quartz volumes mostly near Hyderabad. If someone can ascertain somehow as to for which company they are shipping, that’d be great. Also, if you can find that they’ve shipped quartz earlier, that’ll mean that they already had a customer. This is just me connecting the dots and we’ll get to know the actual trends in quarterly revenues of coming few quarters.

I was looking at the value and volume growth data for quartz export from India. I think after some good time we are looking at more value increase than Volume. As per my understanding, Pokarna has the most expensive product from India and their capacity was ramping up in April, May, June. So high chances, that the increment might be due to their products reaching the shore. Please find the numbers

Q2 results out.

Quartz Rev - 134 cr and EBITDA of 42 cr.

My best case is 190-200 cr quartz in Q3 or Q4 with 35% EBITDA margin due to operating leverage. Management had spent closer to 500 cr on plant 2 and had guided for 1.1-1.2X sales which was revised downwards.

Plant 1 used to do between 330-350 cr and company is spending 70 odd crores for plant upgradation

Plant 2 can do 450-470 cr

Hence, at 800 cr rev, 35% EBITDA margin implies 280 cr.

Stock still trades at 7X multiple and I think given the scale this company has achieved and the product quality, the multiple should expand to 15X. Hence, 1000-1200 should be achievable unless something bad happens in US market. Company has been unlucky a few times. With 200+ cr expected cash flow, deleveraging should happen very fast.

Eagerly waiting for concall to provide more updates on capacity utilisation, future capex plans and revenue projections for H2

Disc - Invested, Largest PF position.

Pokarna Receives Great Place to Work® Certification

Joins the ranks of the world’s most distinguished companies

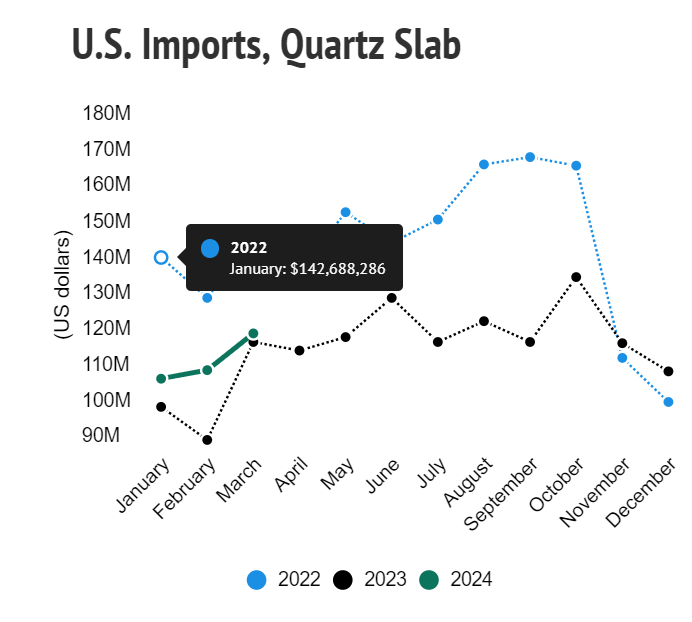

Quartz slabs continue to lead all hard surfaces in November 2021, with $155.3 million in import values outpacing the same month in 2020. The 18 million ft² moving through U.S. ports of entry in November marks a year-to-year increase in volume of 24.5%.

Quartz-Surface Tariff Evasion China/Malaysia : WASHINGTON – U.S. Customs and Border Protection (CBP) affirmed the evasion of unfair-trade tariffs on Chinese quartz surfaces in two separate cases late this year.

U.S. Tariff Rulings on Appeal : M S International (MSI) filed on Dec. 20 for reconsideration of a CIT ruling in October against inclusion of fabricators as producers as Commerce investigated unfair-trade claims made against India and Turkey by U.S. manufacturer Cambria Company LLC. https://www.stoneupdate.com/us-tariff-rulings-on-appeal/

Globalquartz just has polishing setup from Breton, whereas Pokarna has entire setup from Breton.

Also, I am not sure if StonePlus is a big player with Breton Technology since I didn’t find export data by their name.

Also, both these players deal with many other type of materials. Given that we know the capex requirements for state of the art Quartz plant, it looks unlikely that anyone of them are a formidable competitor to Pokarna.

Anyway, we can clarify in the conference all about the competitors of the company India with same technology.

I certainly believe that given Pokarna’s huge capacities and old relations with US counterparts, it is unlikely that they will switch their suppliers unless some strong value proposition is added by other players.

Additionally, I am expecting a massive growth in Q3 numbers due to resolution of shipping issues and ramping up of new facilities. My estimates say that the company should be doing 190-200 cr revenues in Quartz.

Disc. Invested from lower levels and forms ~30% of my PF due to massive move.

Preliminary Results of Anti-dumping Duty Administrative Review 2019-2021, are positive for the company. Attached is the disclosure made by Pokarna Ltd. Pokarna Ltd.pdf (276.3 KB)

In today’s Mgmt interview, Paras said that expect they are expecting 30% revenue growth in quartz business in H2FY25. And decent growth in FY26. US demand is expected to improve in FY26. Looking for buyer for Apparel business.

This is the main risk for Pokarna if trump impose tariff on India - as their main revenue is from US export.

Wait and watch till Feb 2025 - for having clear picture!!