Results are not as expected. Still, the quartz sales have not picked up like 2019 and the margins in Q4 have contracted due to a significant increase in other expenses (maybe because of the new plant). The new plant depreciation is still not appearing in P/L. By seeing sales, it seems the old plant capacity is itself not fully used. Is the demand not picked up or pokarna not getting the traction or quartz prices are very low with good volumes, need to be found out

2 Likes

186ed0ec-cca4-44ad-b216-813fc93683c4.pdf (1.0 MB)

Investor ppt

3 Likes

The company has spent Rs.6 crore towards CSR expenses, included under the head “other expenses”.

Doesn’t this look too high? Generally, the CSR spending is 2% of the last 3 years average PAT.

Am I missing something here?

Not much new in the presentation. I was expecting lower net profit due to lower top-line but results make it look like it’s because of other reasons. Anyhow, key unknown here is the shipping bottleneck. Why has it lasted so long and when can it be expected to be fixed.

3 Likes

Gross Margins have reduced by c.a. 300 bps. They have also appointed an external IR company (CDR). Guess there is more to the story?

1 Like

1 Like

The new plant capacity wil reach optimum levels in 12 to 18 months

Maximum sales from New plant is 1.1 asset turns.

Ebidta Realisation can be between 30 to 35%

Shipping challenges exist now and till today 30 to 35% issue only solved

Competition is not an issue. 130 exporters for quartz from India now

US market have expanded so all the players have market.

Pokarna concentrates in margins, rather than volumes

New plant debt is in USD due to natural hedge and cost is 6%.

4 Likes

The new plant will break even at EBIDTA level at 60% capacity utilization which will be conservatively reached by the Company in next 9-12 months, so we can see margins declining in FY 21-22.

The promoters did not sound very optimistic or enthusiastic during the concal even after successfully commissioning such a big CAPEX.

Disclosure : Tracking and not invested… will wait till Q3 numbers to see how the capacity ramp up is progressing.

2 Likes

Here is a snippet form their recent investor presentation. They clain to be the only user of BretonStone technology in India. But ASI Industries put up a quartz facility last year using the same tech. and ARO Granite did it this year.

Am I missing something?

1 Like

I think you are right.

Breton itself mentions ASI & Pokarna as the manufacturers.

1 Like

Thats quite helpful, Sir. There seems to be a mistake from the company.

Thank You!

They are selling that division…so may not be a serious competitor.

3 Likes

Inauguration of Quantra Quartz factory at Telangana:

Again, very average results from Pokarna. Quartz just doesn’t seem to be taking off.

3 Likes

The PE of the stock is now around 35 levels (from an average of 15). It is entering new PE levels without any profit increase to back it up. I have exited my position (with a decent profit), not so much because of the profits but more because I am uncomfortable with such high valuations.

1 Like

it has not fallen much in the recent midcap/small cap correction…Recent capacity expansion should increase revenue in the next quarters and that is why market is giving higher valuation

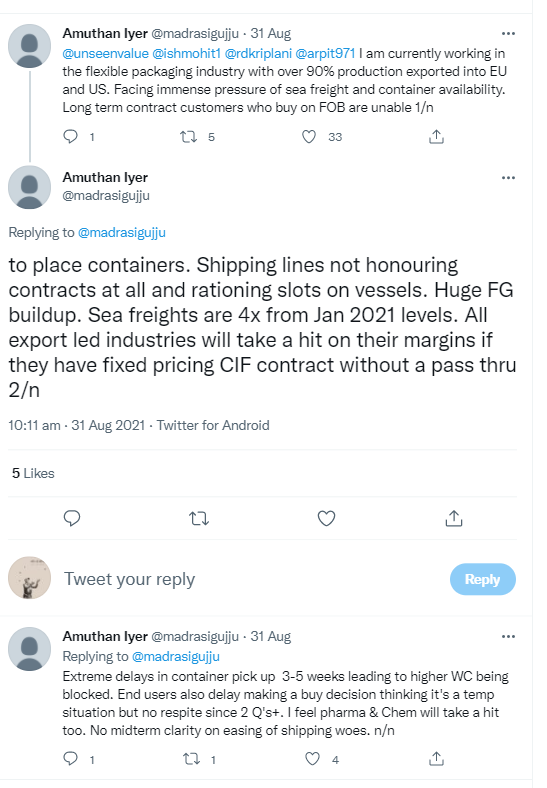

the immediate risk is the cost of shipping, the next quarter is going to be dampener for many companies that ship outside India.

The recent example is STRIDES where they had to spend $5 Mn for shipping the supplies to honor the contractual obligations.

increased by 3 folds

6 Likes

logistical challenges are there for every one, which one has to live with.it will impact whole sector and not just pokarna alone… sometimes, customer do understand these challenges and will probably relax the delivery dates.