https://www.stoneupdate.com/blogsmore/episodes/1925-radio-stone-update-sept-9-2021

Has anyone joined the AGM, any update on new Plant!!

1 Like

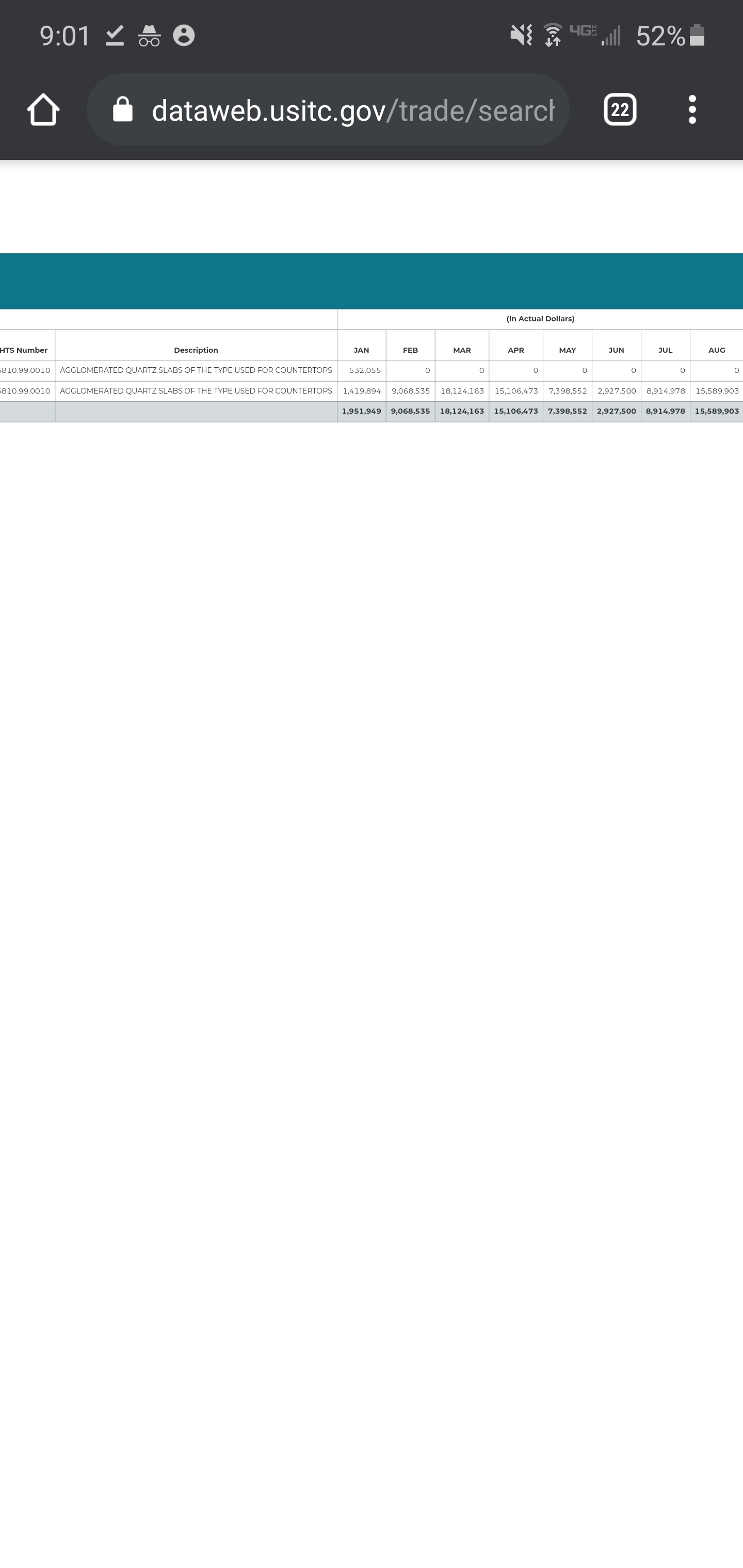

August Data is good, hoping for even better data in September given uptick in US housing. It would be important to have an update on the new capacity in the current quarter’s results.

@pratik - Do you have any idea why the Import data came so late for August ?

Regards

Kanv

Disc. - Invested in mine and Client accounts

2 Likes

Hello everyone,

I have compiled data for the last 60 months of export of Quartz Countertop (QC) from India to the USA and total imports of QC by the USA. I have clustered that into quarterly and annual figures as well. There are some interesting insights and questions that came to my mind-Pokarna- Trade Map Data.xlsx (10.6 KB)

-

In FY17, Pokarna had more than 80% market share of total QC exported from India, that fell to 67% in FY18, and since then it has been continuously falling and has come down to less than 20% at the end of FY20.

-

This implies that competition has mushroomed and there are a lot of QC manufacturers in India that are exporting to the USA. Interestingly, even though Pokarna’s share has come down from more than 80% to less than 20%, the margins have been intact, which assures about the high-end quality of their product and clients. Question- Who are these competitors? I could find a company called Haique that has set up a Bretonstone technology plant but they want to cater mainly to India. Do we know of other big QC manufacturers in India?

-

Even though QC imports by the USA has risen from $200M in CY 2012 to more than $1.2 Billion in CY 2019, India’s export to the USA has grown at a much rapid pace. India exported around $39M worth of QC at the end of FY17 and that figure stood at $240M at the end of FY20. That is a jump of 6x in 3 years. India’s share was 5% of total US imports in FY17 which is more than 18% at the end of FY20. A huge reason behind this is the ADD on Chinese imports. Question- What happens if ever the ADD on Chinese imports is rolled back/reduced?

-

At peak, India was exporting ~650cr worth of QC per quarter and USA was importing ~$400M per quarter. At this peak, Pokarna was clocking >100cr worth of exports.

-

Pokarna exported more than 100cr QC for 3 continuous quarters, each quarter. Then the ADD & CVD came in place. Question- Extrapolating this, if at max capacity, Pokarna can do a 400cr+ turnover from existing capacity, then with 130% additional capacity, could 900cr+ be the peak revenue when both the capacities run at full steam with ~40% EBITDA margins? Remember, USA QC imports have grown 6x from $200m in 2012 to $1.2B in 2019 which is a CAGR of 30%. Which means, there definitely is demand for QC that is rising at an extraordinary pace.

-

Pokarna is clearly losing market share but it is doing so in a rapidly increasing market with sustained margins. USA imported around $117M worth of QC in Aug’20 which is just 2% less than what they imported in Aug’19. The home improvement market has seen a very strong trend with people spending more time at home. It will be interesting to see if Pokarna is able to operationalise its new facility soon and come back to 100cr+ sales starting Q3FY21 from its existing facility.

Would love to hear their insights from everyone.

Thanks,

Ayush.

Disc: Invested and increasing at dips.

20 Likes

Nice work! My conjecture would be that the jump in exports from India seen since Q2-FY19 is just Chinese product passing through Indian shores to avoid ADD. Hence the unaffected margins. The disappearing moat is a cause for some worry, but the product and demand for it do seem to sooth some concerns. And more liquidity should see increasing luxury spending just like the last round of quant-easing did.

Disc: top holding

2 Likes

before the ADD thing came into picture pokarna was operating at almost peak utilizations. Which means they are least affected by competition. Losing market share is because market has grown at a scorching pace , while Pokarna has not grown their capacity. This only implies that Pokarna will easily be able to sell their new capacity.

2 Likes

Thank you, Sir! It does make sense that building and scaling up such a huge capacity would be difficult in such a short time. A huge chunk of this could be just Chinese players routing their exports from India. Is there a way we can confirm this? Plus, why India? Why not Hong Kong or Taiwan or the many fronts China has?

Yes, there are at least two other companies apart from Pokarna using Bretonstone technology in India. But on the other hand, the demand is also very strong.

1 Like

Yeah, agree with you one hundred percent. Pokarna was indeed running at full capacity before the ADD. As @vikas_sinha mentioned, they may not be losing market share, it could just be Chinese players routing their exports from India.

Also, I agree that Pokarna should be able to sell its additional capacity because Quartz Countertop is growing at an increasingly rapid pace.

1 Like

It is easier to hide supplies by making them part of a bigger flow, and HK would be treated same as mainland China for duties I guess. The background of such a (front) country should be a good enough social-distance from China and have (history of) enough local quarrying/processing of granite etc. to support the mis-labeling/hiding of diverted supplies, in order to avoid raising suspicion from US trade/customs.

4 Likes

Good Work Ayush

I was getting a small variance when I used numbers from https://dataweb.usitc.gov/ but overall variance was consistent and doesnt bring material difference to the discussion.

As far as the listed space is concerned I am aware of Pokarna and Asian Granito as the players in Quartz . So I think its fair to make an assumption that probably China was routing supplies through India and may still be doing it from other countries

Given the current scenario , the open question is are they still doing it from India or it is stopped. My hunch says that they might have started exploring some other options and it will slowly taper down as the current environment is not conducive for routing through India

If I look at Q2 data , in July and August alone we have achieved 200+ Cr of exports from India alone and at this rate we should clock 300 Cr easily for Q2 and depending on Pokarna’s Market share we can assume what could be the possible Sales in Q2.

At 10% MS Pokarna should do 30Cr , 20% arnd 60 cr and at 32% arnd 100 cr and I am tending towards 32% which was there average market share in 2019 and 2020

Market is still on the sidelines and waiting for the actual numbers. The Valuations look pretty attractive and if the new Capacity kicks in, it will be a icing on the cake along with low ADD

Also I dont see with China +1 sourcing strategy gaining momentum we should be worried too much about ADD on Chinese getting reduced sometime soon. In my view Pokarna will gain MS back as the supplies routed through India with re-labelling will diminish very soon

In fact, I see overall Exports from India going down and Pokarna’s Market share going up very soon.

Again there are assumptions but increasingly data pts are pointing in the right direction

PS : I have taken a token investment in Pokarna and looking to add more. So pls make your own view and above reflects my personal opinion and should not be treated as investment advice

4 Likes

Below is the analysis by stoneupdate magazine

Malaysia,Thailand and Vietnam have seen phenomenal growth again whereas India has degrown on Y-o-Y basis, this is a little concerning given now there are no lockdowns.

Would love to see if anyone has any on the ground pulse of the situation.

Regards

Kanv

3 Likes

The reports depend on how the products are classified. Pokarna doesn’t sell quartz slabs. It sells engineered/artificial stone that is created with quartz pieces and some binder. It also sells granite blocks.

68029900 - this is another HSN code for engineered stone. The numbers for July in screener are astounding.

I am not an expert in this domain hence all these classifications are confusing to me.

2 Likes

Pokarna hiring a team of 100 sales person pan INDIA as new plant is about to commission

Link

Job Description for Architectural / Sales Specification Representative in Pokarna Engineered Stone Limited in Bengaluru/Bangalore,Delhi/NCR,Chennai,Hyderabad / Secunderabad,Kolkata,Mumbai,Pune for 1 to 5 years of experience. Apply Now! https://www.naukri.com/job-listings-Architectural-Sales-Specification-Representative-Pokarna-Engineered-Stone-Limited-Bengaluru-Bangalore-Delhi-NCR-Chennai-Hyderabad-Secunderabad-Kolkata-Mumbai-Pune-1-to-5-211020007806?src=sharedjd&utmCampaign=pwajd&utmSource=share

6 Likes

Thats disappointing. It looks like a change in plan. and When I had conversation with CEO last year, he had sounded as if like they have demand lined up in US market for the new capacity. I can say housing materials , building products are in peak demand in US as we speak. Multiple favorable conditions for housing now. I have been tracking this company for few years now. With management’s experience in the US market, I thought they had better times ahead…

3 Likes

But why not? They supply to IKEA India and must have witnessed the dynamics. A brand is very valuable to have. After all the anti-globalisation rhetoric and duties etc, any prudent businessman will want to reduce exposure of his business to such risks.

1 Like

Fair enough. I dont know if Ikea is expanding as rapidly, thats just a presumption.

They have been in US market for almost 10 years, but havnt been able to increase market share, I wonder why they cant compete with Brazil in natural stone… with their own quarries and and with cost advantage.

PESL is another disappointing story, and apparel …dont know where are they upto…

Do listen to this interview to get more perspective on the journey of Gautam Chand Jain (Chairman of Pokarna).

5 Likes

I agree with your concern. It is absolutely fine to pivot your plans based on changing dynamics, however the problem here appears to be lack of communication from the management. They have even stopped their quarterly earnings call. So no real way to understand the reason for increasing their domestic team.

2 Likes

Results for Q2FY21. I am not sure what to make out of numbers. Ideally I would have expected the firm to match Q2FY20 numbers since the plant was operational for the full 3 months. There can be 3 reasons for the fall

a) Company lost market share in US and hence reduced volumes.

b) There was reduction in realisation due to intense competition

c) Company faced issues in stabilizing plant operations.

If someone can figure this out, do let me know.

Additional important info and missing puzzle is the date of commissioning of new plant.

Regards

Kanv

Disc. Invested and biased

2 Likes