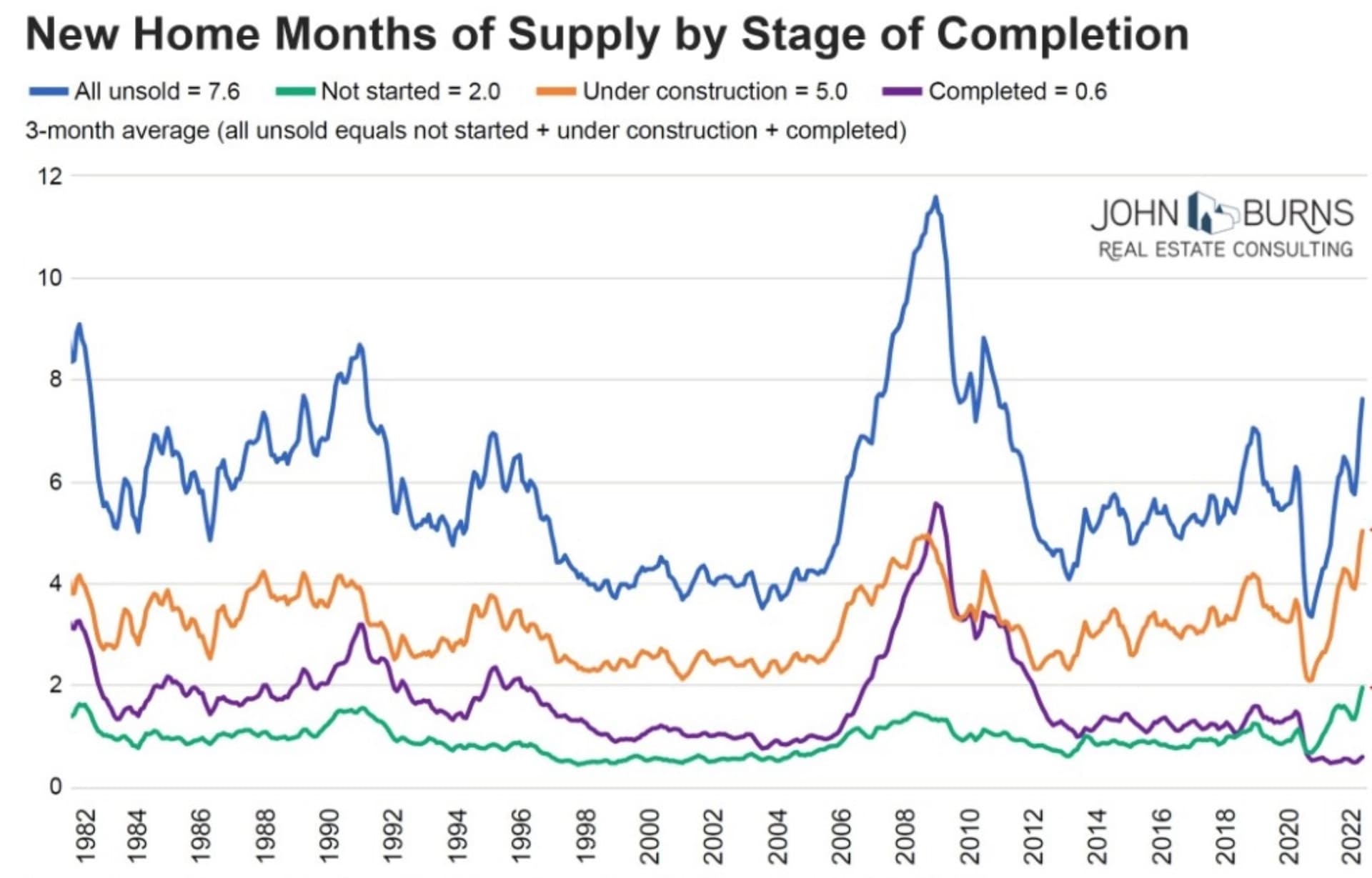

Looks like the US new residential market continues to be weak with rising mortgage rates and supply of unsold inventory to be highest among recent years as the demand finally slows down. (All unsold)

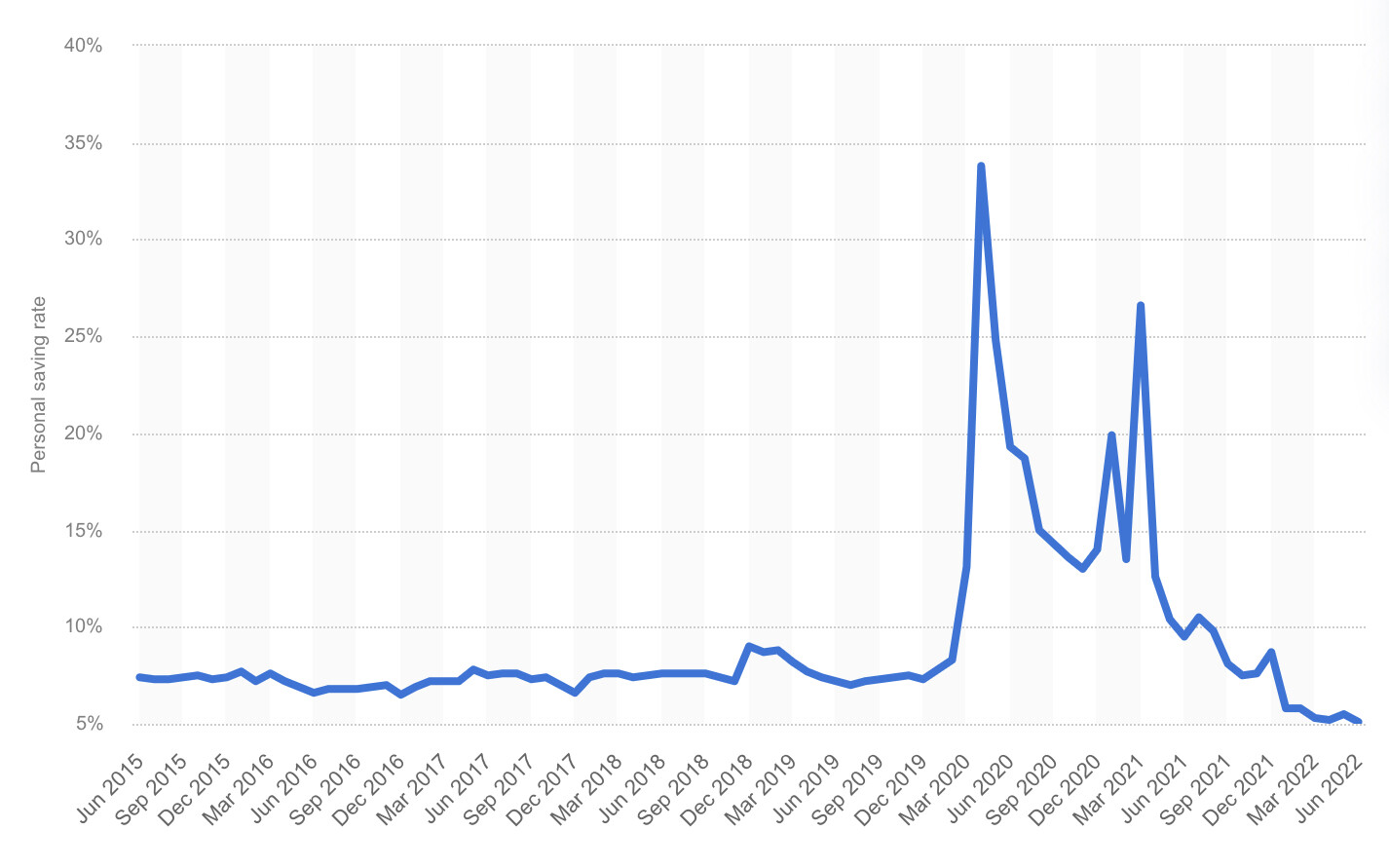

New construction happens to be around 30-40% of the demand while the rest is renovation and remodelling. With the US economy looking to be in a period of mild recession, and with high inflation eating up further into US households disposable incomes, causing household savings rate to dip into multi year lows -

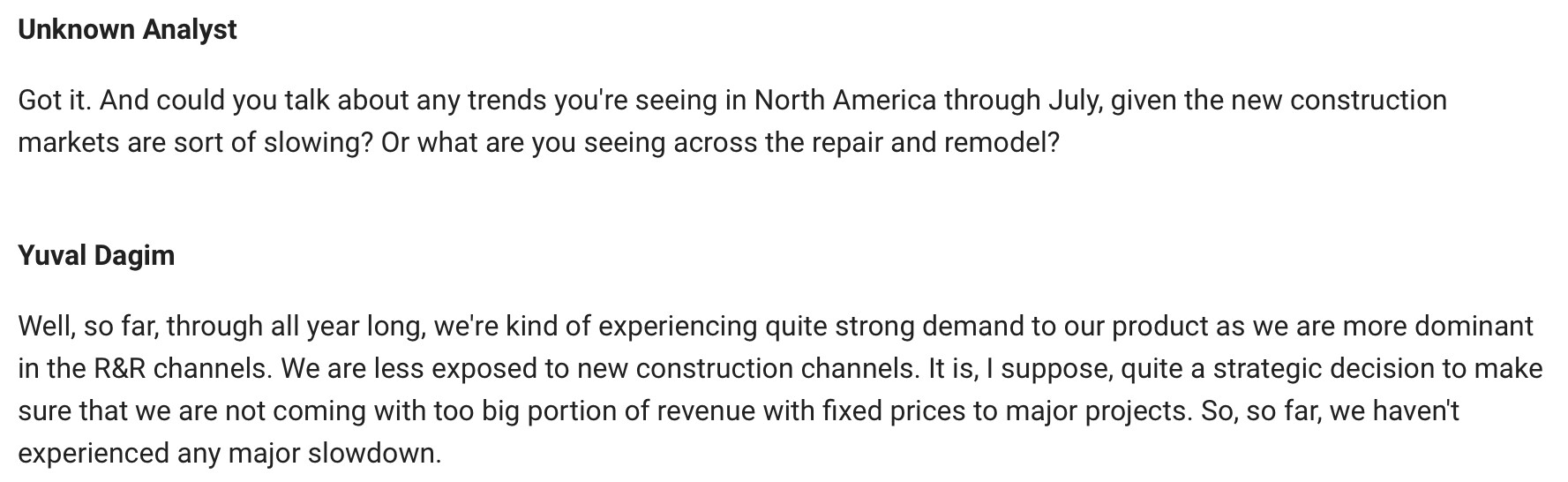

looks like a bit of contradictory inputs coming from the Caesarstone management on how they view the demand environment shaping up - new construction and renovation and remodelling.

While it merits consideration that Quantra typically serves a wealthier clientele that could be relatively insulated in a downturn and they are a minor part of the market share currently, there could be some form of operating deleverage play out until the demand environment gets better.

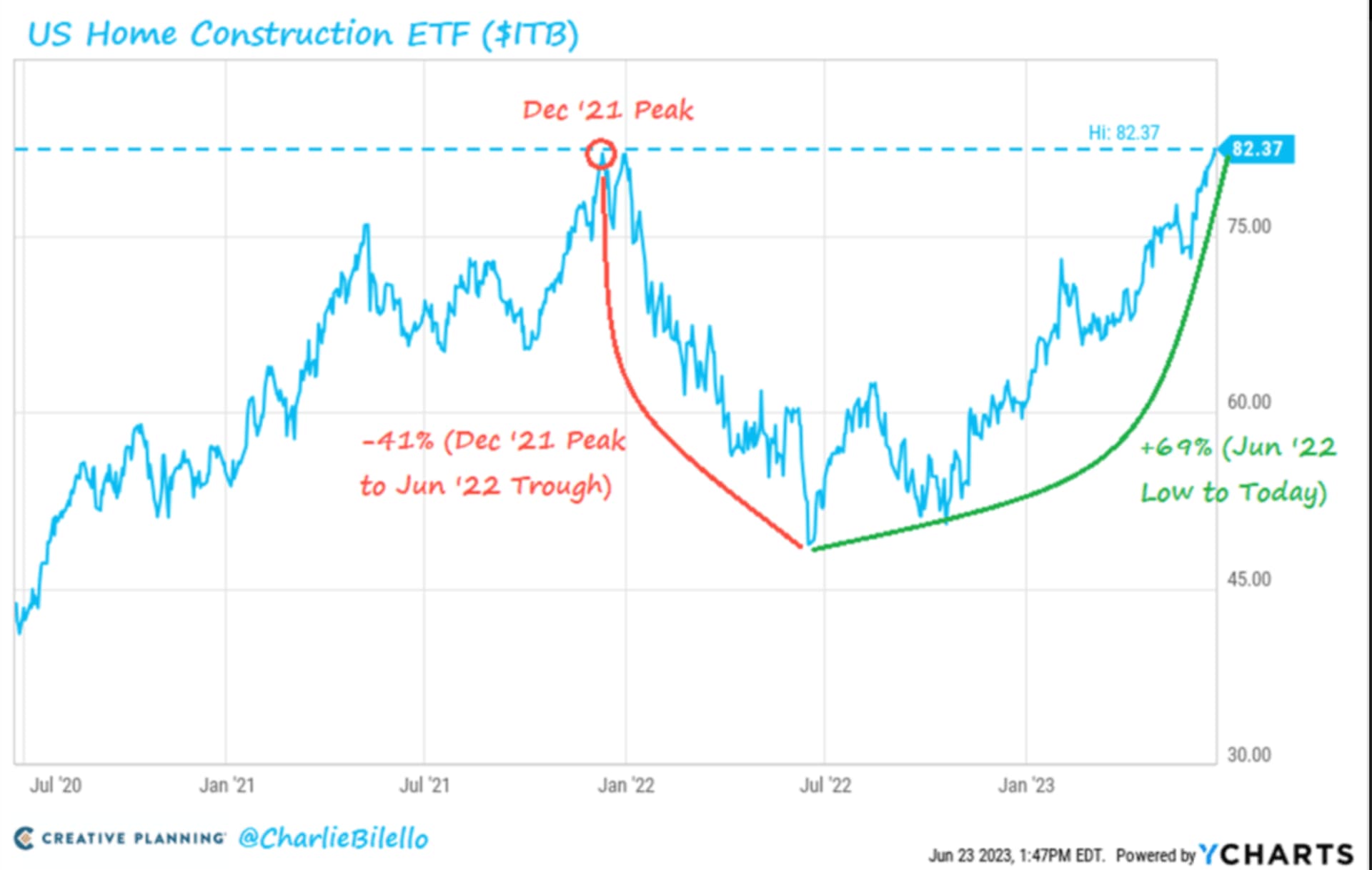

So Fed increased Funds Rate from almost 0% post-covid to 5% by May of 2023. Post-covid 30 Y mortgage rates went up from low of ~2.6% to 7%+ along with 30%-50% housing prices increase which impacted housing affordability for many first time home buyers.

Logical first level thinking was screaming loud and clear to all the investors (including me) that with increase in interest rates and difficult affordability - housing sector would be under pressure and would face severe headwinds in immediate future. This lead to sharp cut in stock prices of many housing builder’s stocks in the US and also likes of Pokarna and Acrysil whose businesses are strongly correlated to US housing market.

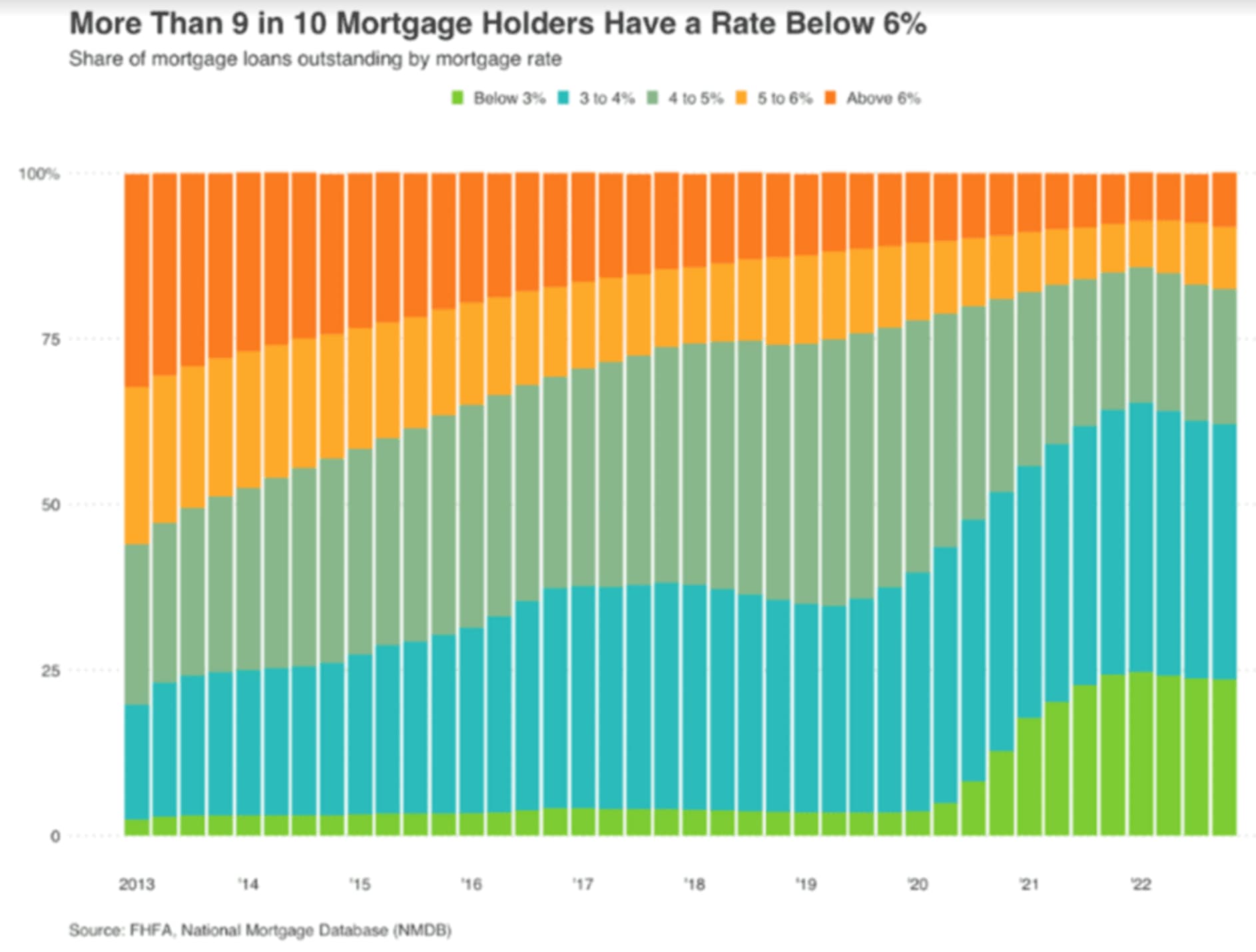

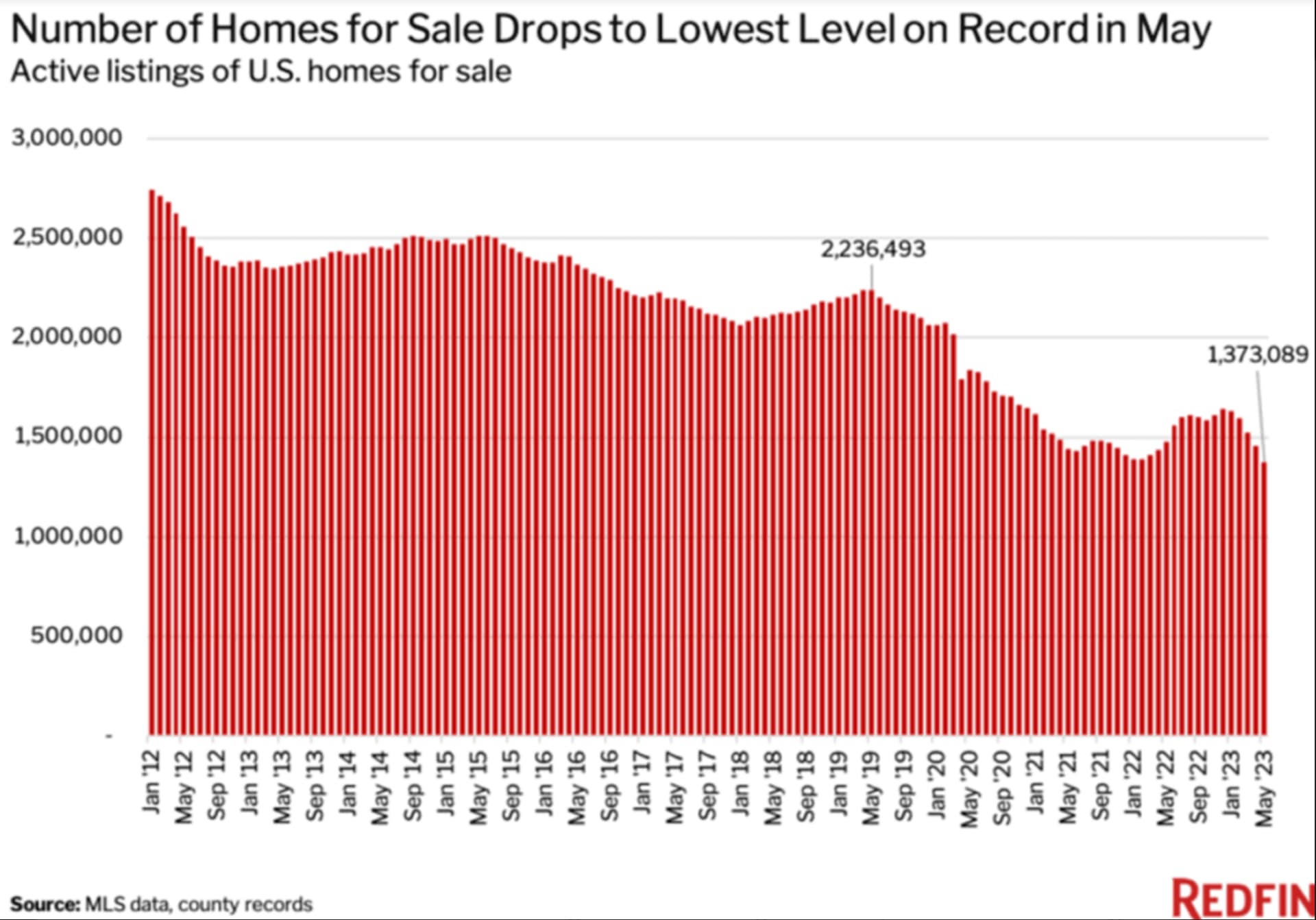

But something very unexpected played out as mortgage rates were climbing north of 6%. There was already a substantial shortage of homes (2mn to 7mn) for sale in the US with housing starts failing to keep up with population growth, for at least the past 10+ years. And 90% of the outstanding 30 year mortgage had fixed rate of under 5% (many had rates as low as 3%) which led to historically tight resale inventory as existing homeowners were unwilling to move into a new house by trading their 3% fixed rate mortgages.

After absorbing sticker shock of increased housing prices plus 30 Y mortgage rates somewhat stabilizing around 6%-6.5% made buyers realize that 6.5% is the “new normal” rate with no immediate sight of lower rates. With very little supply coming in from existing homes for resale - the only option that was left was new homes. This is where the new homes builders made a killing! The situation panned out in such a way that higher rates which caused headwinds in normal market environment, turned out to be a blessing in disguise.

Straight from horse’s mouth - Key Latest Insights from Recent Earnings con-calls of Housing Builders:

Q1CY2023 Earnings Concall Meritage

The true shortage of readily available new inventory coupled with extremely limited resale inventory persisted throughout the U.S. in the first order and doesn’t show any material signs of loosening in the near term. We expect this continuing housing undersupply as well as favorable demographics for the millennial and move-down buyer will provide a strong inventory runway – for strong long-term runway, I’m sorry, for future home buying demand.

Q2CY2023 Earnings Concall Toll Brothers

As I mentioned on our last call, we saw demand start to improve in January. I’m pleased to report that these more favorable conditions have continued through our second quarter and into the start of our third quarter. Physical traffic, web activity and deposits in the first 3 weeks of May have all been very encouraging. Overall, buyers appear to be adjusting to mortgage rates that have stabilized in the 6% to 7% range. The shock of last year’s abrupt spike in rates appears to be wearing off and buyers are moving on with their lives.

As I pointed out in the past, there is a substantial shortage of homes for sale in the U.S. with housing starts failing to keep up with population growth, for at least the past 15 years. Now with 90% of outstanding mortgages under 5%, the market is seeing the further impact of a low interest rate lock-in effect, existing home buyers – excuse me, existing homeowners are reluctant to give up their low rate mortgages, which has led to historically tight resale inventories.

In fact, according to recent reports, approximately 35% of homes currently for sale are new construction compared to the historical norm of between 10% and 15%. This phenomenon has become a boon for homebuilders and especially the larger, well-capitalized public builders who are more efficient and better positioned to take advantage of opportunities compared to smaller private builders. With such low levels of resale inventory on the market, buyers are gravitating to new homes. As they do, they benefit not just from the opportunity to buy new, but they can also take advantage of incentives like rate buy downs that are generally not available on resale homes.

In addition to the underproduction of new homes in this country and the low level of resale inventory, there are many other factors that continue to support the housing market. These include favorable demographics with millions of millennials and baby boomers on the move. Millennials, in particular, are buying their first home later in life when they have higher incomes and accumulated wealth. Migration trends are driving the population south and west, which not only increases demand in these markets, but alleviate some of the affordability pressures as buyers move from high cost to low-cost markets. More flexibility in the workplace also supports this migration and the housing market in general as buyers place a greater emphasis on their homes. These trends have staying power that we believe will continue to support housing demand for years to come.

Specs also allow buyers to lock their mortgage rates at or near the time of contract. We believe that in this market, our spec strategy continues to make sense. With such limited resale inventory, specs fill a significant gap in supply. We expect that specs will continue to comprise between 30% and 40% of our sales for the foreseeable future. The more stable environment has allowed us to increase price in more than half of our communities. Factoring in base price increases and incentive reductions, we have increased price by an average of approximately $25,000 per home in the second quarter.

Q2CY2023 Earnings Concall Lennar

As it relates to Homebuilding, the economic environment has stabilized as customers have adjusted to and accepted higher-for-longer interest rates. The supply chain chaos has normalized, inventories have remained low, and the supply of housing across the country is in very limited supply.

This environment seems to represent a new normal that is formed in the wake of the Federal Reserve’s aggressive interest rate hikes starting last year. While persistent inflation remains in the system, aggressive rate hikes have given way to moderated and measured rate movements, allowing the market to adjust in orderly fashion. The strong demand for housing that had been curtailed by sticker shock and affordability challenges, has returned, while the housing market adjusted prices, incentives, including rate buydowns and production costs in order to enable customers to afford needed shelter.

And even while interest rates and affordability were primary headwinds to demand, the well-documented chronic housing supply shortage has kept inventory levels very low, which has continued to propel customers to stretch their finances for needed housing, as incentives and price reductions combined to spark sales activity.

Looking ahead, we continue to believe that the market and the economy will remain constructive for homebuilders as pent-up demand continues to come to market and consume affordable offerings. Additionally, we believe that the supply constraint will continue to limit available inventory and maintain supply-demand balance. The core elements of the supply shortage will not resolve in the near term as the almost 15-year production deficit will take years to resolve.

And note that even when existing homes with low interest mortgages that are not currently trading do come to the market and add to supply, the sellers will also need a place to move. And that creates a net 0 to overall dwellings, in addition to supply and in addition to demand and, therefore, still a housing shortage.

Bottom line, supply is short, demand is returning to affordable offerings and builders will need to produce more homes to fill the void. Against this backdrop, the Lennar team has remained consistent in our commitment to strategies that we articulated as rates began to climb over a year ago. Let me do a quick review as these strategies explain both what we have accomplished as well as what we expect to accomplish throughout the remainder of the year.

Q1CY2023 Earnings Concall Pulte

Among the actions we’ve taken has been to increase our production of spec homes, a strategy we began implementing in the back half of 2022. As discussed on previous earnings calls, we made the decision to increase spec starts as we saw the opportunity to realize a number of strategic benefits within our homebuilding operations. With more units in production, we can better meet buyer demand as more consumers are seeking quick move-in homes as a hedge against rising mortgage rates.

Given improvements in demand conditions and the broader interest rate environment as well as a generally limited inventory of existing homes, we are starting to see the pressure on selling prices ease in many of our markets. In fact, in well over half of our markets, we have found opportunities to pull back on incentives and/or move prices higher in many of our communities. While the price changes are modest, it demonstrates the point that people desire home ownership and are willing to buy when they see a value.

Earlier this month, there was an article in the Wall Street Journal that looked at the housing shortage in this country. The article raised the point that, depending upon which expert you ask, the housing shortage ranges from 2 million to 7 million houses. While there are certainly debates about the number, I think there is broad agreement that we have a housing shortage. I believe this is one of the reasons homebuyers are quick to respond when affordability pressures can be eased.

One common message by all the players is that current supply is short, demand is returning and home builders will have to build many new homes to overcome supply shortage that will not resolve in the near term as almost 15-year production deficit will take years to resolve.

House Delivery Estimates by Big Housing Builders for 2023

Lennar is expecting new homes delivery to be flat with little de-growth by rest of the players. Small de-growth is a big boost provided 30Y mortgage has moved up from 4.25% levels to current 7% levels in last 18 odd months.

Many of the home builder’s stock prices are trading close to their ATH levels which implies that market is perceiving good times ahead for new house builders.

There is decent demand visibility from new home construction side for next 12-24 months. Can this demand help Pokarna do topline of 1000cr with EBITDA of 250cr? This is a million dollar question that we shall find out in next 12-18 months.

Adding some data points to support these amazing insights put forth by @rupaniamit

Why are inventories so low?

62% of US mortgage holders have a rate below 4% and 92% have a rate below 6%. With current mortgage rates at close to 7%, many existing homeowners are staying put, leading to a dearth of existing homes for sale.

Let us see if Pokarna is able to capitalise on this. One worry which I have is that this phenomenon is supply-led and not demand-led. What I mean by that it is clearly visible from Amit’s table of “House Delivery Estimates” that New House Delivery in CY23 is not expected to be 10-15% higher than 2022 and 2021. It is at the same level. So, why is it still interesting? Given the rise in mortgage rates, new home construction should have fallen but due to the re-seller market being dry, new home construction demand has sustained.

Given that another rate hike is on the cards, mortgage rates will go up from here. This does two things, dissuade more resellers to come into the market and also dissuade potential buyers. It is an interesting tug-of-war situation. Would have been more upbeat if this was a demand-led situation.

There is enough evidence of sectoral and regional tail winds for demand in US but somehow Pokarna has not yet benefited it. From container shortage/price hikes to now excess inventory in Channels (according to mgmt).

My primary concern is that Company’s important customer Wilsonart has started its own production. Company’s top-line is on decline ever since.

In last concall, management mentioned that they are now trying to venture into other geographies such as European countries, Germany was mentioned.

In same concall, they mentioned that it takes 4 months for product to reach Germany once it is shipped!!

Reading between the lines, if company is so desperate for orders that it has to reach such a far-away territory then that does not give me a bullish indicator.

In terms of tail winds, it can’t get much better for the company and we still have these margins and top-line numbers.

However, management may as well be right about excess inventory in the channels because of constant threats of ADD and CVD from US gov. I am willing to give Pokarna 2-3 quarters more to see how it pans out.

Not losing any client is one thing but if a major client reduces the order sizes then that’s similarly negative for the business.

Not sure what the buzz is about the results, margins have improved, yes but we need to see them sustain in the coming quarters otherwise it may just be an exercise to keep investors happy. Management has clearly mentioned that near to medium term is uncertain and challenging. I really want to believe in the Pokarna story but it’s time numbers do the talking. I had a significant position in Pokarna which I have exited as I would rather gain less by investing on reliable strong signal then be hopeful and invest hoping that future will be good. It would have been a different story if stock price offered good margin of safety and market was in lower valuation zone but neither of that is true right now.

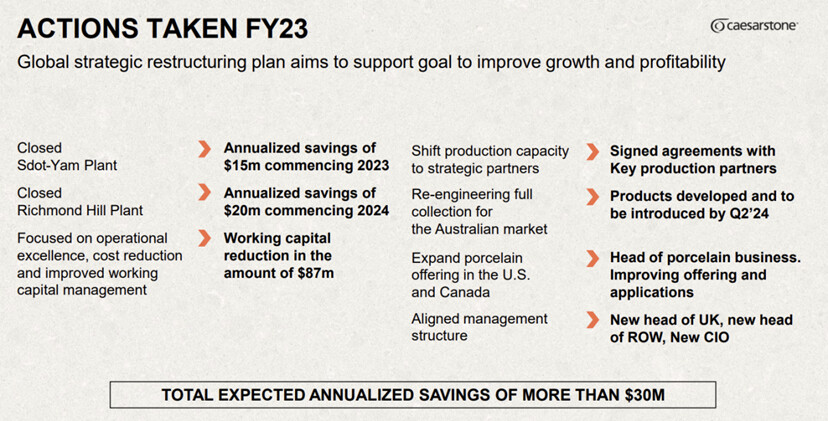

“In the second quarter of 2023, we made a decision to close our Sdot-Yam manufacturing facility. And in December, we announced the closing of our Richmond Hill facility. Following these strategic changes to our operations, we are now sourcing over 40% of our products from production business partners. We expect that percentage to trend up further as we move through 2024.”

Would this be beneficial to Pokarna growth prospects ?

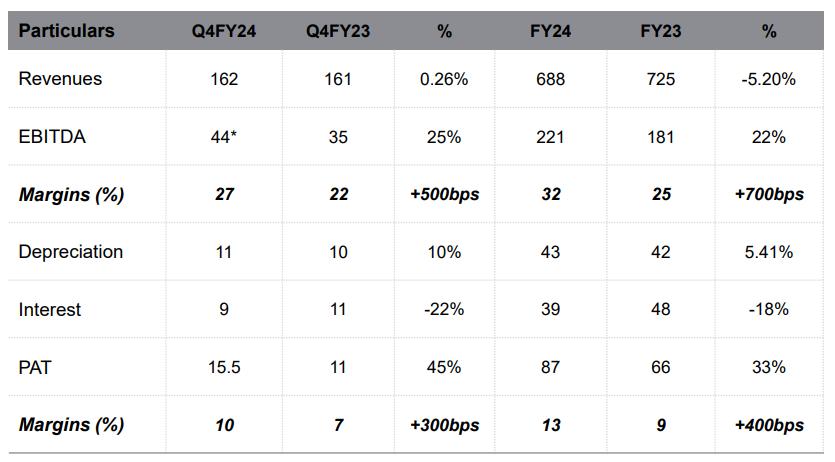

Company has discontinued operations in Apparel segment. In FY25, company is expecting to grow revenue by 15-25% with EBITDA margin of 30-35%. Kreos line to start from Q2FY25 and Chromia line from Q4FY25 - both of them would contribute to revenue primarily from FY26 + margins from these segments to be better than existing products