Have tracked this company for few months and liked the past performance of the company. I feel the co has good business model with a steady growth. At current valuations of less than 5 PE and good div yield, it looks to be a safe steady compounder to me. More of a defensive pick in the portfolio. Here is a small post done recently:

Poddar Pigments (BSE:524570)

Poddar is one of the largest company in themasterbatchindustry. Masterbatches are additives used to impart color or additional properties to polymers.

If one looks into the track record of the company, it has been delivering a consistent growth and has developed a good balance sheet.

It seems to be a safe value pick at these levels of Rs 52, due to attractive valuations:

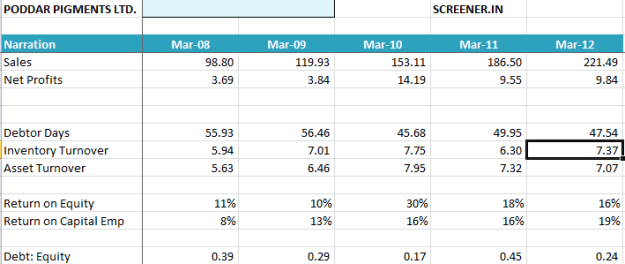

1). The company has been delivering a consistent growth of 20% in topline and much betterbottom-linegrowth.

2). The stock istrading at just 5 PE.

3). The stock is offering adividend yield of 3.90%.

4). The stock is trading at 0.80 times FY12 book value of 63.

The possible negative is that the company is operating close to full capacity and hence there may not be much growth for sometime.

Looked at Cochin Minerals & Rutile? Ratios wise this one looks much better & I also like the products I see good sustained demand for them. Though getting the AR(2011-12) of the company isnt easy and cant find any Quarterly Reports.

Also the AR doesnt have a balacne sheet!!! How can they get away with that???

I had bought Poddar early last yr but exited after getting a good return in the smallcap frenzy in Dec 2012. It still does look undervalued I guess. Maybe mkt perceives it

commodity like business. From what I understood the sector is fragmented, entry barriers are low and there is not much pricing power. Demand is strong though and growth for sector is still holding up at 14-16%. One thing I did not like was that mgmt used idle cash to play in the stock mkts and they had to write off 1.94cr in 2011. ANd they did not reply to my queries on future cash management either

1).

** betterbottom-linegrowth. 2). The stock istrading

I dont think this stock is good because it does not have any moat and pricing power. Better to buy stocks where they directly sell to customers and where customer base is wide.

Interesting reading on this industry. The per MT realisation for Poddar pigments is almost double that of Plastiblends. At a capacity which is 1/4th the size of Plastiblends, it is still doing very decent in terms of sales and net profits.

The only hitch as Ayush mentioned is currently they are operating at nearly full capacity and hence there perhaps is a capex expansion in the offing. Debt has been significantly reduced last year - which may perhaps go up if they need to fund the capex and that could increase the interest cost and thus hit net margins.

Having said that - this may not be a multibagger or an invest and forget kind of company. But at these valuations - particularly today at sub-50 levels - this looks interesting.

Disc - took a starter position in this company today and hence views could be biased.

Thanks for pointing the key thing, Mr. Pinto. Yes, its really interesting that the realisations for Poddar are almost double to that of market leader plastibends…perhaps it has do with more of value added and superior quality products.

Net profit of Poddar Pigments rose 41.94% to Rs 3.52 crore in the quarter ended March 2013 as against Rs 2.48 crore during the previous quarter ended March 2012. Sales rose 25.52% to Rs 74.67 crore in the quarter ended March 2013 as against Rs 59.49 crore during the previous quarter ended March 2012.

For the Audited full year,net profit rose 29.98% to Rs 12.79 crore in the year ended March 2013 as against Rs 9.84 crore during the previous year ended March 2012. Sales rose 24.17% to Rs 275.52 crore in the year ended March 2013 as against Rs 221.89 crore during the previous year ended March 2012.

Given that SEBI is not going to take the issue of auction seriously, can appealing to management for increasing the liquidity through bonus, split etc help ?

I know its been a long time since this thread has had some activity…I was looking at the financials and looks interesting…what are your thoughts on the stock…though not sure if you are still tracking it…

I exited it few months back as it was more of an under-valuation pick for me and though it continues to remain cheap (not as much as before ) but I wasn’t having much clarity on future.

Poddar Pigments still running good and i think it will run further now due to its nse listing , its almost debt free much better than plastblends and excel industries so definitely deserves a re rating of pe ratio between 17 to 20 on its consistent performance for last 6years. hopefully might get added to MSCI small cap index keeping fingers crossed.

can you please throw some light on current scenario of poddar pigments vs platiblends as valuation wise it is still cheap .

But any report like capital line you shared earlier regarding their realisation ,products type ,capacity utilisation ,future plans etc because i seems they may be thinking of capacity addition as had not done from long time.

Does anyone know if there is a relation b/w Poddar pigments and Poddar housing? I could find the managers of Poddar pigments also being directors in a number of affordable real-estate ventures, but couldn’t get it down to Poddar housing.

) but I wasn’t having much clarity on future.

) but I wasn’t having much clarity on future.