Could you Pls share the avg ticket size of Poddar houses or the sq feet rate of selling if you have this info ?

e. g for Ashiana it is 2900 Rs/sq ft if I am not wrong

Also if you can share the avg size of these houses, 600 sq ft or 1000 sq ft.

i searched a lot but couldnt find anywhere ?

Thanks @vivekbothra, I like the story and has been researching for quite few months and read your blog several times on Betankrich and I follow you on twitter also, liked your new Suven post.

What makes you believe that Poddar will not be affected by real state slow down ?

How it is different from Ashiana apart from size ?

and your take on valuations ?

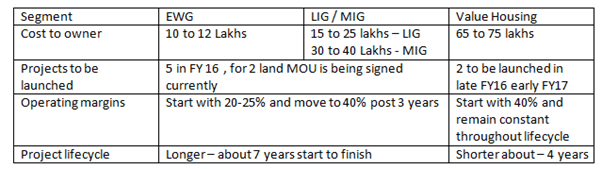

@sinha124 - Real estate slowdown impact will impact every player, Positives for poddar are

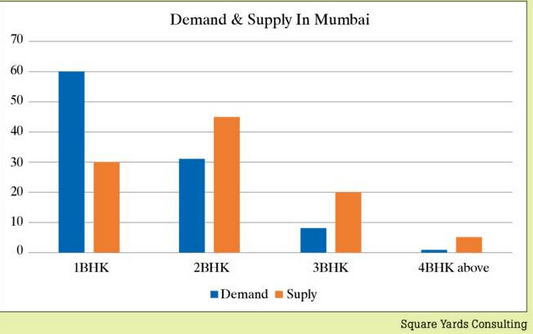

It is a local player (Mumbai) only and in Mumbai demand for 1BHK (the bread and butter of Poddar) is twice the supply

The very core operating model of the company is to build for delivery in next 3-4 years and don’t hoard land, So it has less debt on books thereby more capacity to suffer in trying times

It is similar to Ashiana and best is they don’t compete in same geographic regions, So its like owning GRUH and Repco together

Valuation is tricky with small cap - Rohit Poddar says his vision is to

To sell 10,000 flats – 5 million square feet every year from FY20 (I think that’s quite steep target) with about 15% PAT levels

Lets go by this

10,000 flats, rate 3600 per square feet Avg dwelling size of about 500 square feet

Sales - 1800 Cr

PAT - 270 Cr

At 15 PE - The business should quote at 4000 Cr market cap in 5 years

Today Rohit appeared on cnbc awaaz and informed due to change in rules all projects which were to be launched in april has been pushed by 6-8 months. So any meaningful growth will happen fy17 onwards. All QIP money will be used for maharashtra region only. No plans for gujarat.

Thanks @vivekbothra for the detailed reply, Appreciate the same.

The story is promising but I am not able to take a call, will further research and but thiswill help

Any idea what has triggered the steep fall in the price of Poddar? I presume the initial drop was owing to the general real estate slowdown but there has been a further decline in the past few days. Just wondering if there is some specific trigger/event driving it.

@Aragorn

Both Ashiana & Poddar have been telling of the general decline in real estate off take. Next few quarters are not expected to be good hence the froth is coming off the stock prices. With no near term triggers the stock is still positive on a YTD basis. No apparent reason for the same and hence the price correction. Saying all this there is no one who can predict near time price movements of a company. Do a detailed analysis on your own and you will have the answers

@karan

Yes you are right as both the companies management has raised the concern on the future sales guidelines to flat or negative on YOY basis. But I think this good time to be contrarian and load up the stocks for the next rally when interest rates in India drop and economy starts reviving.

This two are only quality stocks with great management available in the reality space which are very less leveraged.

Poddar developers is better placed than ashiana housing owing to customer segment it addressed where there is most demand/supply mismatched.

Anticipating multibagger returns from this two companies in the future.

Disc : Invested in both the companies and together forms 5% of the portfolio

For a company having such erratic performance, I feel it is richly valued at 38 PE. I understand huge potential for affordable housing market. But not many companies have been able to make money in this market on consistent basis.