Today’s move may have been because of:

JM Financial come up with report yesterday with the target of 1680

Today’s move may have been because of:

JM Financial come up with report yesterday with the target of 1680

Credir suisse initiated the coverage

And both the stocks are down today

Is the housing finance story over?

Almost all the HFCs are correcting (infact more than a correction), any views from the members.

My theory - interest rates have bottomed out, growth is slowing in the near term. I have also seen rise in NPA levels in many HFCs which could be an industry trend.

If there is no growth - hence no deemand for credit - why would interest rates go up then?

Interest rates do not depend on supply/demand for credit only. When I said interest rates have bottomed, did not mean it will start going up right away. A combination of domestic demand revival and cost push due to oil/metals etc is enough for RBI to start tightening. Also, US bond yields and INR fx rates also play vital role. I am more worried about rising NPA levels than interest rates. If you take any large city, majority of home loan customers over the last 10 years have been from the IT sector. Home prices have stopped rising and there is great possibility of rise in delinquencies.

Just check Manappuram, Repco, and Aspire (Motilal) which lend to self employed segments and their NPA have sky rocketed to 3%+. I would have been ok if they were available at much cheaper valuations.

Mumbai is a large city. How many people in Mumbai are employed in the IT sector? Do they comprise the majority of the home loan borrowers? Delhi is a big city. How many IT employees can afford to buy houses in Delhi? What about cities like Ahmedabad that depend more on trading?

Please be considerate while calling other’s analysis simplistic. Most of us end-up doing simplistic analyses sometimes.

Dear Forum members,

Let us focus on PNB Housing in this topic. For a broader discussion on EV and its impact, there is a dedicated forum. Kindly use it for deeper discussion on the topic.

http://forum.valuepickr.com/t/electric-cars-bus-call-it-a-disruption/?source_topic_id=8797well, I don’t even need data to prove that most of high paying jobs have been created are in the services industry over the last two decades. A large part of economy is about services. Real estate, both commercial and residential, in most of big cities in India are growing directly or indirectly due to outsourcing industry (IT, BPO and KPO).

Coming to mumbai, how many apartments have been built in colaba vs. suburbs like Thane, Navi Mumbai etc. Agreed, there could be good % of Indian corp demand in Mumbai unlike other cities.

Delhi - How many apartments in Chandani chowk vs. greater NCR? so majority of “incremental” customers buying properties in Noida and Gurgaon are govt employees or working in manufacturing?

Check the emphasis on the work " incremental"

Services comprise a majority of the GDP in India (54%). IT sector accounts for only about 15% of the services pie. 85% of the services are not IT. For a change, try looking at the data. http://ierj.in/journal/index.php/ierj/article/view/570

In a nutshell, people involved in services (54% of GDP) would likely comprise the majority of the home buyers, but it looks almost impossible that people from the IT sector (7% of GDP) would account for a majority of home loan customers.

~hope this helps. I am not going any further in this discussion.

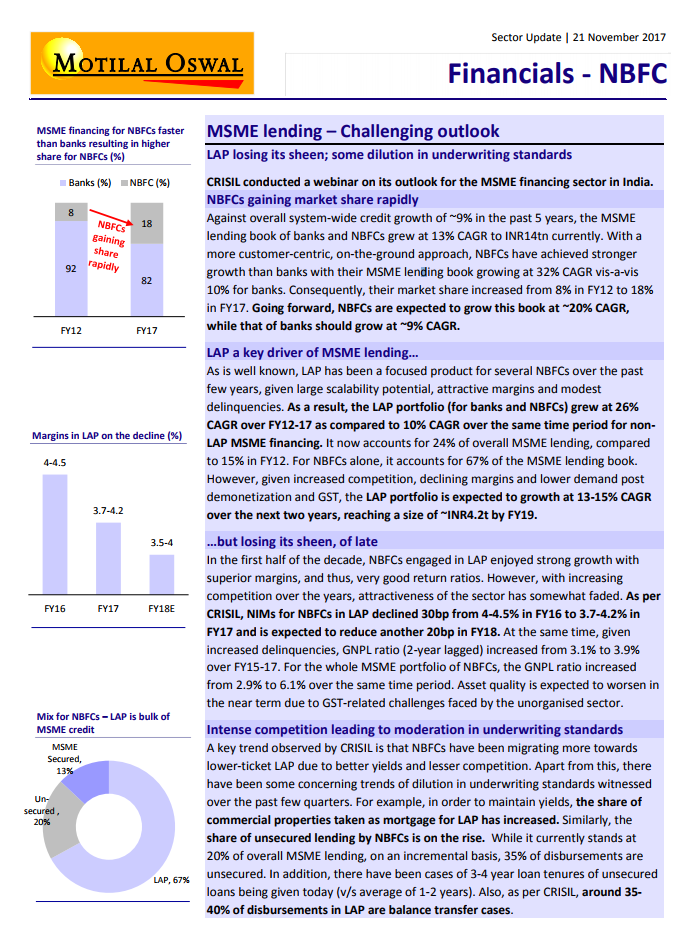

MOSL Report on MSME lending.

CRISIL conducted a webinar on its outlook for the MSME financing sector in India.

One means which PNBHF uses to increase its business is to increase its exposure to risky CRE lending.

Discl. Significant exposure to PNB HF

OFS on 29th Nov for Retail Investors. Floor Price at 1,325 per share.

Now it can be understood why price was not moving. I am disappointed as the price is kept high for retail investor at least more than 10 percent discount should have been given. Majority of the stakes is with institutional and big houses.

The OFS as evidenced from the notification to the exchanges, is made by the promoter PNB to the extent of 6 % of paid up shares of PNB HF. It is a good thing that PNB reserved 10 % for retail investors. Normally is is just direct sale or off market sale to institutions.

The company PNBHF wont get a penny out of this sale.

If am right the current promoter holding (PNB) is 39.08 % and after this OFS, it will come down to 33 %. There was some discussion (not able to trace back the source) that if it falls below 30 %, the HF wont be able to use the PNB name in it - again not sure on the validity of this claim.

Edelweiss initiated the coverage. Target price 1659

HFC general view at a glance

https://drive.google.com/open?id=0B3I0sldHkYdFNG9fcTNTNExCbnZ1Zk4xTjlTblVWb19qT09r

please scroll …it is there

Magicbricks Partners with PNB Housing Finance Ltd. to E-Auction Re-Possessed Assets

https://content.magicbricks.com/property-news/industry-buzz/magicbricks-partners-with-pnb-housing-finance-ltd-to-e-auction-re-possessed-assets/95795.html