Disclosure: Invested but looking to add more at lower valuations.

Some holes in your thesis could be:

Despite having lowest cost of funds, is it possible that the top 5 mortgage players not earn ROE of above 15% due to increased competition, in which case, investors may not be interested in funding these businesses? Given the commodity nature, how can we be certain they will continue to earn above 15% returns atleast.

PNB management looks great based on the current performance, but how can we be sure that their books will not release unexpected surprises in the future. High growth often masks hidden problems

Housing finance depends somewhat on housing growth and although long-term housing growth is certain, there could be cyclical downturns which could impact Housing finance companies performance as well

My holes are fairly benign as I am also an HFC bull and have significant portfolio allocation to HFCs but I am very cautious if ROEs start to deteriorate for them

I think like Microfinance, there is a section of society that are unbankable by large HFCs due to their lack of credit history which carries with it a higher risk. HFCs catering to this specific area can form a niche beyond the commodified housing loans which is ofcourse a riskier bet.

Wont the dilution be 30% / (P/B). So if they can raise funds at 3 times book which is where the stock is currently trading at, the dilution will be 10% for a growth of 50%.

@amitayu Sir, How does dilution affect retail holders negatively? Isn’t it that raising equity at higher p/b multiples actually increase the book valuefor all, thereby enabling it to grow (the bookvalue) at a faster rate than the ROEs permit.

Your singular focus on ROE is surprising. ROEs need to be looked at in conjunction with other metrics such as the type of borrowers being serviced ( which drive NIMs) default rates and other risk parameters like concentration risk to understand the attractiveness of the business as a whole.

Before the subprime crisis, country wide and northern rock in the US and UK respectively had high ROEs , that didn’t stop them from becoming bankrupt.

Closer to home, India bulls has high ROEs because it has high margins from lending to weak borrowers, the default rates are likely to shoot up in case of a recession. Repco another HFC that boasted high returns is now paying the price for its high risk strategy of lending to the self employed in a few states.

PNB is so far increasing its returns in a prudent manner which will reflect in ROEs over time.

@ricky76 ,I am not focusing ROE/ROA singularly , Quality of book is also equally or more important to me . But that does not mean I will ignore ROE /ROA because at the end higher ROE indicates the company generates better return on share holder’s equity / ROA indicates How management efficiently executing the operations and these are most important metrics to me along with NPA .Provisions and Spread. During PNB Housing IPO /Quarterly con-call management indicated they were targeting 1.9% ROA by next FY end by reducing cost to Income which was not met.

@abhishkjain2626 Yes raising equity at higher P/B multiples (4/5 or more ) is indeed good but don’t think whether it will be good for existing shareholders of NBFC which is quoting at 2.75 PB . Also market timing is important to get traction on capital raising.

Increasing Book value through Higher ROE by maintaining Low NPA will always command greater valuation . Example Gruh which never diluted Equity and maintained good growth due to its consistent Higher ROE.

To me PNB Housing should focus on improving ROA/ROE than Growth for next few years . Once ROA/ROE get improved , company need not to go to market frequently for raising equity .

Lets assume their loanbook was somewhat riskier… yields being 50 bps higher (10.5% vs 9.9% currently), in FY18 they made a topline of around 5500 cr, in this case at 10.5% yield it would have been 250 crs more. Taking an extra % for higher credit costs and taxes, they would still have made approx 150 crs higher profits i.e around 980 crores giving an ROA of 2%.

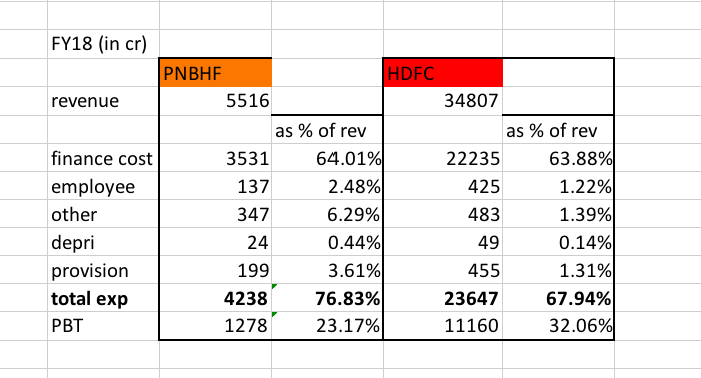

On another note, HDFC & PNBHF have very similar yields and cost of funds i.e the same spreads. Still, HDFC has 4% NIM while PNBHF has 3.1%. Why the disparity?

Will suggest fellow members to read through the following -

1.Amit Keerti has provided a crystal clear analysis of the company. The best part is that he has compared management’s commentary in prior quarters with latest result.

2.Company’s latest call transcript -

Sunil Tirumalai: Last question is how low do you see the Tier-1 ratio, at what level are you comfortable before you re-capitalise again, thank you?

Sanjaya Gupta: To be very frank, the Board guidance is at about 10x lever to our Tier-I capital we should start preparing ourselves to raise additional capital or go to capital market and I think at about 11x to 12x lever of Tier-I capital, we will be raising fresh capital and I think that should come in our sort of forward journey somewhere in the last calendar quarter of 19 or the first calendar quarter of 20 and let us not forget that internal accruals are going to be smart for this Company since economy of scales are playing up and I guess by that time our NOF should be somewhere in the vicinity of INR 8,000 crore when we go to the capital markets next.

Koteshwar Rao: One last question in the last concall like it was being told like the ROA levels can be maintained from 1.7 to 1.85 by the time we come back to market for the capital infusion?

Sanjaya Gupta: Give us eight quarters and we will be there. It is also the way the management works, as I was saying if I would have not done the contingency provisioning, my ROA is already 1.62%, but it is a conservatism that sort of makes us do what we are doing because we do not want to be totally going berserk and calling out great numbers and tomorrow because of cyclical aberrations or something, we have nothing to fall back upon.

CRISIL has reaffirmed its ‘FAAA/CRISIL AA+/Stable’ rating on the debt instruments and bank facilities of PNB Housing Finance Ltd (PNB Housing). Rating on the commercial paper programme and short-term bank facilities has been reaffirmed at ‘CRISIL A1+’.

Attached is the image of Consensus Analyst recommendation on the Stock. I would be obliged if someone could source the report from Morgan Stanley Analyst (Subramanium Iyer) - who has given a price target of 1,100 for the stock (Sr. No. 12 in the list). This report is of significance because Carlyle has appointed Morgan Stanley for it’s Stake sale in Company.

Really appreciate the analysis @Yogesh_s and experience you have shared @suru27.

Thinking more on the low Run Down rate of PNBHF -

Does a low Run Down rate actually helping PNBHF to keep the NPAs under control? Ideally, longer the period of loan more the chances of it becoming NPA.

Generally, In all the schemes of loan payments, interest amount is to be paid very heavily in initial years and then Principal amount becomes heavy in later years. So, if major chunk of loan book is closed or transferred to other HFCs after 4 years then this generally doesn’t imply a bad thing for PNBHF company as such, right? What the HFC companies or any lender actually earn is the interest component and i assume that this company is able to skim the cream of interest anyways in initial years + they are able to disburse new loans with good growth.

I am novice in investing and might be wrong in my assumptions. I welcome views from valuepickr junta on my assumptions/understanding.

Discl: Invested recently and eager to add more if price falls further.

1.longer the individual loan to individual buyers especially salaried person, better it is for the financier.As the loan payment progresses, the risk gets reduced.

2.The interest quantom is higher in initial years due to the high principal amount.however the rate of interest being same and spread out does not mean that financiers skim out high interest in initial years.

3.Its only process and other charges which add to income in first year.

I held this share but sold it sometime back when saw that even after great increase in profits EPS never increased much because of constant dilution of equity. Constant dilution of equity when your business does not really needs it is a sign of not so good management for me so I had to sell. Any thoughts on if I made right decision?

PNB housing has less than 100 branches against 200 odd for Gruh finance and can fin homes. Sanjaya Gupta seems to be gunning for HDFC. He has informed in the concall that current years performance will be even better than last year’s. Also there will be around 8 crores equity dilution next year (to give 8000 crores). They should be having 200 branches in 4 years with profits of atleast 2500 crores plus ( assuming 19% ROE). Hence the 1.75 times market growth is in place atleast for 4 more years. They can grow with internal resources slowly. But Sanjays seems to be gunning for HDFC. This is the reason for going berserk. Also Private equity who call the shots in the board always dream big. Disclosure: Heavily invested.