Does somebody know why PNB Housing is under performing for the last 6 odd months. It is trading at a PBV of 3.36 where as peer group like India bull @4.6, Canfin @ 4.8 etc despite stellar results. Is the market worried about asset quality or their aggressiveness in LAP segment? Appreciate learned views

ROE is less. So BV is throwing less EPS. Can Fin and Indiabulls have better ROE. That’s why P/B is less for PNBHF. Please check P/E is high in comparison to Can Fin and Indiabulls. It means market is anticipating ROE to increase. Once ROE is increased P/B will increase.Even if P/E is same price will go too high.

Yeah. ROE will increase as ROA and Leverage both will increase. In next couple of years, ROA will be 1.85(C/I will reduce further) and leverage will be 10-12 times. ROE is less in this financial year due to raising of IPO Fund in nov,16. P/B also depend on management pedigree,Quality of Assets etc.

As per the RBI report on affordable housing, GNPA numbers were the lowest for >25Lacs segment loans. GIven PNBHF’s avg ticket size is also around that, which is usually higher than most HFC’s, does PNBHF seem to be a better contained in terms of future NPAs? Also this stock seems to be neglected by the market for the past 6-7 months.

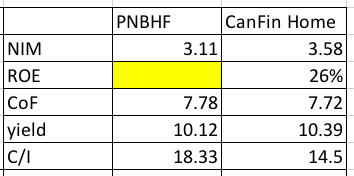

is PNBHF comparable with Canfin? There is further scope to increase leverage in PNBHF, and C/I to fall. CoF are almost similar. Could we expect ROE to rise to similar levels?

I think one should look at LAP exposure of these 2 companies . Risk associated with LAP is different from housing loan. Also , PNB has loans towards builder schemes of doubling money where lot of people ve taken loan for the sake doubling money and we know what’s happening to such projects . Analysis of loan book type is most important to differentiate in my opinion

Will it rise to Can Fin levels it is doubtful. But Sanjay Gupta has clearly indicated the RoE could rise to north of 16%. This will happen as OPEX and CIR come down and leverage is taken to 10x-12x from < 8 now. This is as per his statement.

industry level segment performance is an average indicator. Performance of PNB book will be function of their own credit quality. e.g. NPA in commercial loans vary from 25% to 2% depending on lender (PSU vs good private bank).

We tend to visualise LAP as dangerous because we hear such kind news from industry and align with the same perception. But it all depends on how the loan is given. Based on what assessment and how the product is structured.

But Sanjay Gupta has indicated they have done appropriate product structuring and hence the NPAs for LAP is 0.59% which is similar to Hsg loans 0.49%.

Don’t the yields on LAPs compensate for the higher risks? And surely the management is smart enough to not risk their asset quality chasing high growth rates

@abhishkjain2626 , Don’t think ROE will be the correct parameter to value NBFC ,ROA is more meaningful as ROE depends on leverage also. Canfin leverage is around 11.5 where PNB Housing is 7.So there are scope of ROE expansion .As per management it could reach 19-20% by 2020.

@suru27 ,Canfin /PNB HFC is not only the company which provide LAP loan . There are other companies also like Edel ,Piramal which provide LAP loan and Builder wholesale Loan but in respective of asset quality, PNB Housing are far better than other NBFCs because they don’t provide Loan on Assessed Income. We will get an idea by Looking at NIM to check the loan quality because generally it has been observed that for riskier loan assets NIM are comparably high i.e in microfinance companies NIM is higher than Retail Housing Fin companies. PNB HFC only provide Loan to TOP quality developer hence their NIM,Yield is comparatively lower but it also ensures better asset quality.

LAPs are always priced higher and at times more than compensates for the risk. But when housing cycle turns then LAPs are the first to go bad and in larger scale as well. Hence, through the cycle LAPs are considered a riskier asset class. So, to summarise, housing loan losses are chunkier and during downturn, risk based price will not be enough to cover for the loss.

Basically, for any finance companies, Asset quality is much depended on Management pedigree /execution skills. It was assumed that affordable Housing loan is safer than traditional Big Ticket Housing Loan/LAP, but latest result of few NBFCs like MOSL Housing Finance subsidiary (Aspire)busted the Myth. We saw it’s low ticket housing subsidy clocked 6.5% GNPA which is much worse than LAP loan. Actually, all depend on the parameters which company are checking before providing a loan, If any loan provided without analyzing cash flow then it bound to be default irrespective of the type of Loans.

. There are other companies also like Edel ,Piramal which provide LAP loan and Builder wholesale Loan but in respective of asset quality, PNB Housing are far better than other NBFCs because they don’t provide Loan on Assessed Income. We will get an idea by Looking at NIM to check the loan quality because generally it has been observed that for riskier loan assets NIM are comparably high i.e in microfinance companies NIM is higher than Retail Housing Fin companies. PNB HFC only provide Loan to TOP quality developer hence their NIM,Yield is comparatively lower but it also ensures better asset quality.

. There are other companies also like Edel ,Piramal which provide LAP loan and Builder wholesale Loan but in respective of asset quality, PNB Housing are far better than other NBFCs because they don’t provide Loan on Assessed Income. We will get an idea by Looking at NIM to check the loan quality because generally it has been observed that for riskier loan assets NIM are comparably high i.e in microfinance companies NIM is higher than Retail Housing Fin companies. PNB HFC only provide Loan to TOP quality developer hence their NIM,Yield is comparatively lower but it also ensures better asset quality.