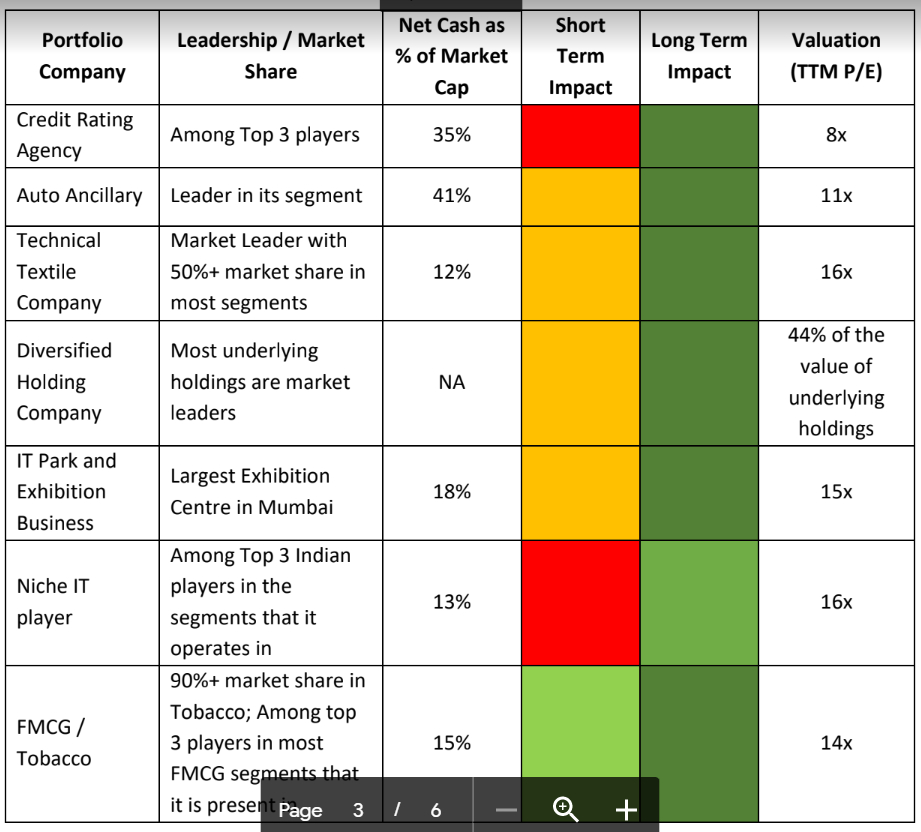

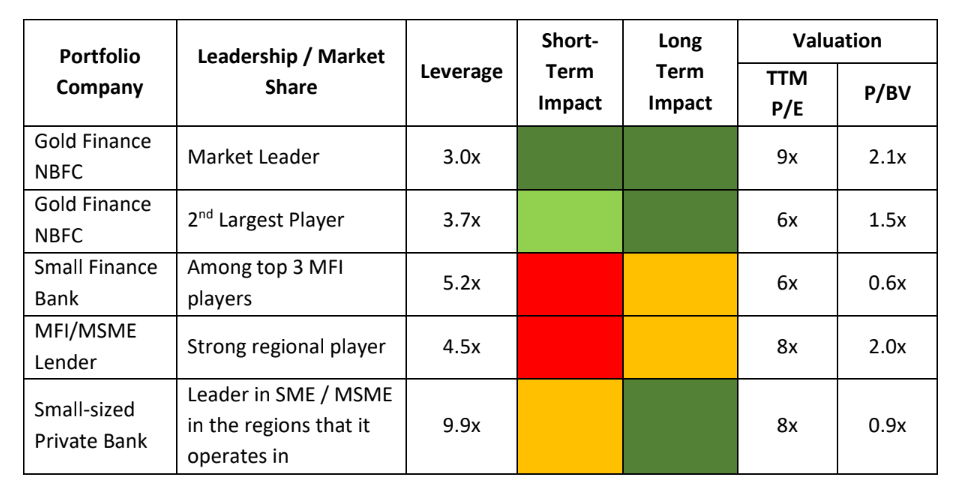

Latest 2Point2 Capital newsletter: http://bit.ly/2xVrcLaQ4FY20

Could identify only a few companies from the list - CARE, Nesco and ITC. From the financials in the portfolio - Muthoot, Manappuram

This time they have sort of disclosed their portfolio:

Latest 2Point2 Capital newsletter: http://bit.ly/2xVrcLaQ4FY20

Could identify only a few companies from the list - CARE, Nesco and ITC. From the financials in the portfolio - Muthoot, Manappuram

This time they have sort of disclosed their portfolio:

In a falling market any support is good

If lots of people trust them to be good at picking stocks and markets are generally falling, by revealing their stocks, they will have more buyers looking for “easy” bargains where things are checked by someone reputable

It’s generally in their interest to reveal their stocks as you want many people to buy what you already bought and the price to go up but at the same time you want to make it a bit difficult so it’s not common knowledge and someone who finds it with bit of analysis feels he really found something of value for free and puts his money there

My guess would be:

CARE, SRF/ Garware, NESCO, LT Infotech and ITC

Muthoot, Manappuram, Cholamandalam and DCB Bank

Hi

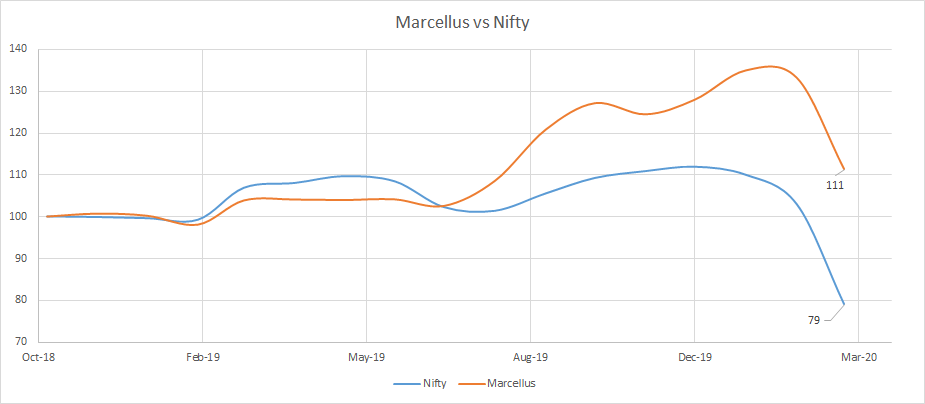

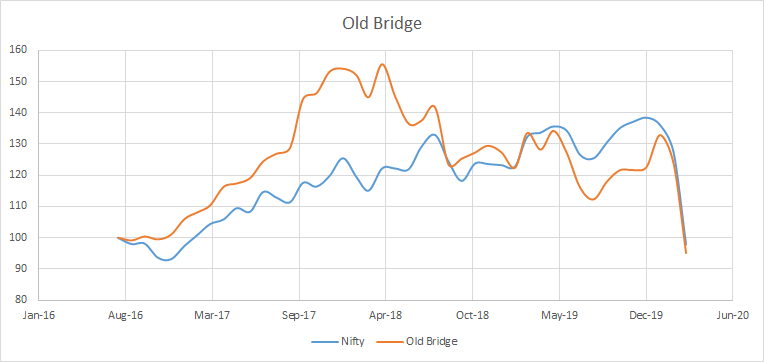

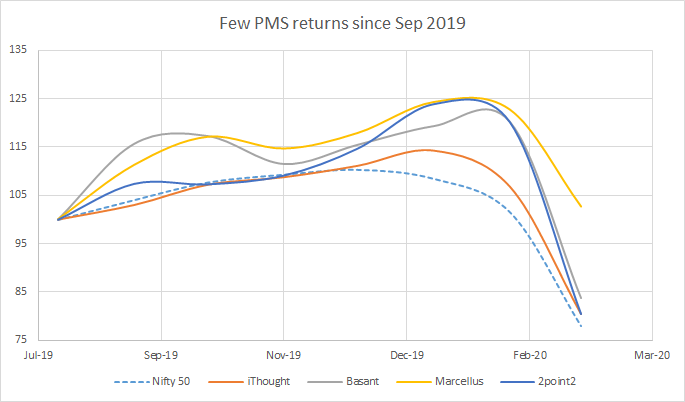

I keep a tab on few of the PMSes out there. I get their returns and AUM data on a monthly basis from the SEBI website. Sharing a few of the charts which I have. Maybe a few find it helpful.

Disclosure: I am not associated or invested with any of them.

Marcellus

They have done quite well compared to others. A CAGR of 8.4% since inception. 100 rupee invested with them became 111 at the end of March 2020 vs 79 for the Nifty. This is not including fee. 1/3rd of the investors came in Dec '19 they are down 11% vs 29% for Nifty. Their max drawdown is also respectable at -17.5%.

Old Bridge

This was one fund I had reached out in 2017 I think. They were not taking any money. So I didn’t invest with them. Their March data is not out. But their performance has been quite mediocre till Feb. I am assuming with a 25%-30% drop in March they will have a negative CAGR and below Nifty also. Poor performance actually.

ithought

Led by Shyam Sekhar this is the youngest PMS I track. They have kept ahead of the Nifty so far. Since Shyam, Basant Maheshwari, 2point2 and Marcellus are the ones most active on social media I tried to compare them from the time ithought PMS started.

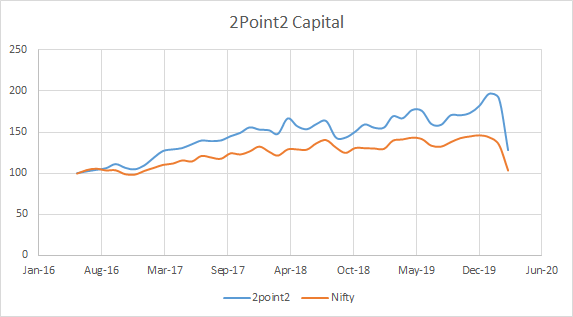

2point2

These guys have also done average actually. Lifetime CAGR is a mere 6.9% before fee with a Max DD of 35%.

I can estimate that their time to recover to peak CAGR at historical median monthly rate is 30 months. Meaning only after 2.5 years will their investors likely see their portfolios return to peak rates. But this wont happen perhaps it will taken even longer.

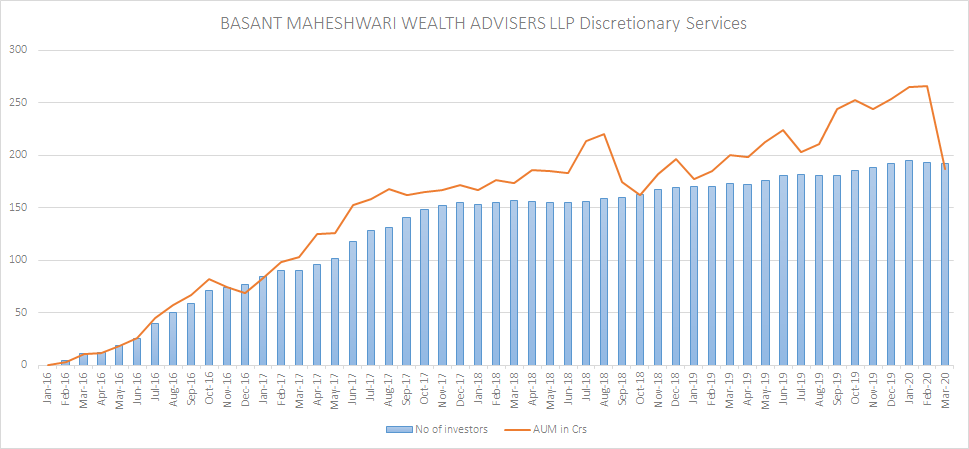

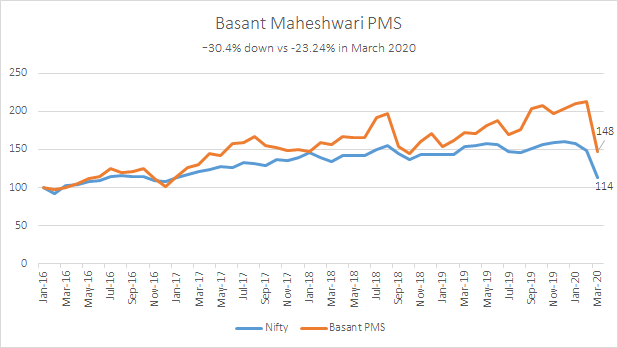

Basant Maheshwari PMS

The PMS was down 30% odd in March 2020. The CAGR since Jan 2016 of 9.61% vs 3.06% of Nifty annualized. Absolute Returns since inception of 48% vs 14% of Nifty. Max Drawdown of 30.4% vs 29.3% of Nifty. Current AUM around 190 crs vs peak at 266 crs. Effectively rewinds 1 year in AUM value. Still a good CAGR.

Regards

I could not see Marcellus March data from SEBI website. Its available only till Feb 2020.

Hi

They released their notes on their returns from Jan 2020 to March 2020 and also for the FY20. So you can back calculate.

Rgds

Hello @deevee @ajaymu @zygo23554

Is it possible to see current constituents / script holdings of PMS like

Marcellus

2point2

Basant Maheshwari

Old Bridge

ASK

Motilal Oswal

And changes from March to April

If its for cloning its a very bad idea! People who have cloned has lost big time.

Hi @deevee, thanks for this data. However, there are a few points I would like to mention:

The strategies of these funds are very different and just looking at the returns vis-a-vis NIFTY can create extrapolation bias as few themes have done very well in the past few years but whether they would continue to do better than other themes is a completely open question. I am writing this because most investors when it comes to investing amongst various strategies focus excessively in the recent performance which in my opinion is like trying to drive a car looking at the rear-view mirror. As such I want investors to understand this data in the right context. My points will also be valid while looking at the performance of other fund managers.

1. Market cap related differences

In the last two years, large caps have significantly outperformed midcaps which has outperformed (not significantly) small caps. Just to give some sense, large caps indices like SENSEX and NIFTY made their all time highs in Feb 2020 while the small and mid cap indices had made their all time highs almost two years back in Jan 2018 and have since been on a downward trend.

Hence strategies like that of Marcellus (mostly mega large caps), Old Bridge (mostly large small caps and small midcaps), ithought (I have no idea) and Basant Maheswari (large caps to large midcaps) are very different. Hence comparison with NIFTY (which is a large cap index) will obviously skew the picture in favour of large caps and so on and so forth. Ideally each of the strategies should be compared to their relevant benchmarks as in the long run all the benchmarks returns more or less converge towards the same number. Of course, for someone looking for a shorter time-frame like a few years, I think that investor should also focus on what kind of strategy and theme will do well in that time-frame. But for long term investors, what should matter is the alpha generated over the relevant benchmarks rather than a common benchmark.

2. Quality/Growth vs Value

The second defining trend in 2018 and early 2020 has been the focus on few highest-quality stocks. This is because of three reasons - a) very low level of interest rates globally and this foreign money has been chasing a select few stocks (mostly in large caps) because of lack of liquidity, b) high inflow of domestic money in mutual funds and most fund managers afraid of taking contrarian views and happy to go with momentum and c) a number of frauds like DHFL, PC Jewellers coming in at the same time reinforcing the trends mentioned in the above two points.

For the first time in the history of stock markets, ever have so many stocks traded above 40x P/E in NIFTY. For the first time we have seen such low PEG for so many select quality stocks.

As such funds from the above pick and in general who have focused on quality and not valuations have outperformed others. For instance Basant’s (Highest growth at any price), Marcellus (quality with reasonable growth at any price) would do well in such an environment while an Old bridge (value) will underperform.

In fact, value investors have been underperforming growth stocks for a long time now, the more this continues, the more there are chances that this cycle will take a turn. The reason value beats growth over the very long term as per multiple studies around the world is that it does get beaten by growth quite often (as has been happening for the last many years). When it gets beaten, there is skew - like the one happening in India even before the Coronavirus situation - on one hand, companies are trading at 20% free cash flow yields with 5% growth and on other hand, companies are trading at 2% free cash flow yields with 10% growth. This is a cycle that will auto-correct.

3. Indian economic growth

Weak economic growth environment since demonetization and other structural changes like GST is restricted to very few pockets resulting in their over-valuation while taking outgrowth away from a large number of sectors pushing them to under-valuation. A patient long term investor should take advantage by embracing sectors where growth is currently cyclically down (like good stocks in utilities, PSUs, metals and so many other sectors). However, most fund managers live under the pressure to perform and come to CNBC TV18 to talk about their last month and one-year performance. As such most are actually chasing momentum stocks. A few of us had high weight to pharma (because obviously pharma stocks went into a cyclical low) before coronavirus scare but what was the weight in NIFTY - just 2% and what was the weight of financials - 40%. The reason is very simple - most people are happy chasing just the momentum stocks.

So again, coming back to performance data - fund managers who were choosing to invest in the very select sectors where growth was visible like private banks and select consumer discretionary stocks would have shown a better performance as the economic cycle was subdued. As and when the change in gears happen, this would mean better performance for the others.

**Over a long enough time from now, the returns from all these caps & themes would converge. Which means large caps and small caps would have given largely equal performance, sector-wise returns would have normalized (caveat: some sectors are more inherently more attractive than others but most of these fund managers who are acting contrarian are investing in the less attractive sectors from a very low point while the momentum managers are investing in more attractive sectors from a very high point, hence the difference), cyclical with good balance sheets will converge in the returns with defensives (again the caveat before). **

What will matter hence is alpha over the long term which will depend on the skill of the fund manager in picking stocks from a given theme rather than which theme as such (which is all which matters if past few years of data is looked at).

Hope this will help investors try to look at these performance data through a more thoughtful lens and using second order of thinking. And try to drive their cars looking forward and not backwards.

Regards,

Sarvesh Gupta

PS - I am a SEBI registered investment adviser and my views might be biased given my own theme of picking stocks for clients and how close it is to some fund managers and away from the theme of others.

PS - On value vs growth, people who are interested to read more can go through the recent article by James Montier of GMO - “Dare to be Different”. EM Shiller PE for value stocks at 10% earnings yield seems to be at the all-time low.

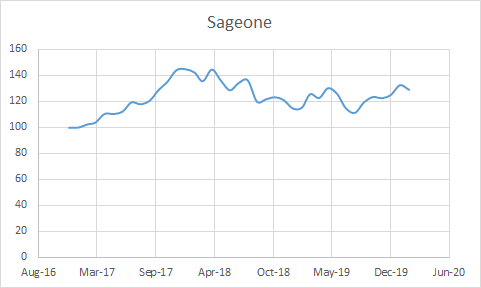

Thanks a lot. This is indeed useful. Can I please request you to include SageOne as well ? Have not invested with them, but based on public interactions, Samit Vartak seems to be a good mid/small cap investor focussing on growth stories. Will be good to track their performance as well.

Separately, just a general question to PMS investors who have been invested for 3+ years - how has the returns been post charges and taxes ? Has it handily beaten a good midcap fund ? The numbers published by PMS portray a rosy picture, but what effectively is of relevance to investors is whether they have beaten decent mutual fund returns after considering all charges / profit share / taxes, etc. Can you please share experiences ?

Hi

I dont keep a tab on Sageone other than reading Samit’s letters which is very good.

Nevertheless from the data on SEBI which starts from Jan 2017 for Sageone below are the metrics. Please note March 2020 is not uploaded yet so this is till Feb 2020.

CAGR till Feb 2020 +8.4%

Max DD till Feb 2020 -11.9%

Unfortunately if Sageone performs as well as the index in March the overall CAGR will drop down to a negative ie ~ -3% odd.

I hope this helps.

Rgds.

This analysis is not perfect IMHO.

You should look at returns in the same period. Since inception makes less sense. (Primarily because u get the benefit of bull run or negative of bear run) Most funds look very bad if u look at only 2020.

Also you can add a percentage to the old horses like with a track of 10 years. (Because its like comparing sachin with vinod kambli)

PMS funds are charging minimum management fees + profit sharing.

They are NOT part of sharing loss!! - subscriber only pays for loss!

This make most of PMS as momentum chase PMS. They buy more and more momentum stocks so that they show profit in short-term and take profit sharing from subscribers. When tide turns down only PMS subscribers are bearing loss but still PMS manager will earn minimum management fees. (EQUITY Intelligent PMS during 2017-18 is great example!!)

This is get repeating for new subscriber in his PMS fund! Hence, PMS manager having good flow of new subscribers are earning more !

SEBI shall make rule for PMS to share loss also. If this rule implemented, PMS manager will take care more cautious step and manage money in better way than only momentum.

Contd…with above post…

Another data point one must be careful -

Normally, PMS guys showing overall portfolio return over a period of time/years. Believe me, individual return from such PMS is always lower than overall return shown by PMS. Why? reason could be -

(1) PMS subscriber normally don’t invest in SIP form but lump sum (mostly looking at past performance they invest one time !! - like in 2017 - many subscribed EQUITY intelligence PMS, many subscribed in 20118-19 - Basant PMS, many subscribed in 2019 - Marcellus , etc) . That’s why such momentum PMS manager are very much vocal /advocate on TV/media and showing excellent return during their momentum stock up cycle to capture more subscribers. Once cycle turn down they go hibernate!! e…g Porinju Veliyath presently enjoying in his farm house (look his tweeter timeline!!) but his PMS subscriber does not get sleep looking at PMS return!!)

(2) PMS manager uses new funds from new subscribers to invest in momentum stocks at that time looking at maximum profit at the earliest to get max money as part of profit sharing! Many PMS take profit sharing in quarterly performance of portfolio also !!)

(3) With above two points - PMS manager able to average out return for overall PMS portfolio. However, investor might lost money or only got below Index fund return due to deduction of management fees, profit sharing and correction in momentum stock price over a long time!!

Above points is based on my personal learning (burned fingers) - My PMS (well known name) claiming good CAGR return but when I look performance of my individual investment in his PMS is far below what he is claiming !

Hence, I started direct SIP in MF and Index fund also!.

Request to share your experience as PMS subscriber.

Alternates in India (PMS and AIF), have been hard to analyse due to the way the reporting is done. The platform at Fintuple breaks down the industry into a granular way. Fintuplist is a monthly edition the platform comes up with as a concise summary of funds that are doing well. A user could also register and do his/her analysis on the platform.

https://fi.fintuple.com/insights/the-fintuplist-marginal-fall-in-pms-performance-in-may-2020

Does anyone have first hand experience with First Global Sec - esp their Global PMS offering ? Shankar Sharma is very vocal on the need for diversification (asset classes, geographies, currency) and rightly so. However wanted to understand if their performance matches their marketing talk.

Separately are there any points that one needs to be careful of ? - for eg there were some articles of him / wife focussing more on start ups in their personal capacity in the past, some SEBI bans, etc.

I don’t have specific answer for first global but I think Ramdev A (Motilal Oswal) seems more vocal than SS.

I had Motilal PMS which is down by 20%. The Hugh downside is contributed by their expenses. Expense is No.2 worries you need to address.

No. 1 worry is their outdated mindset. “Buy right, sit tight” you need to understand to wake and walk up if you are sitting on shit.

e.g. Quess co: purchase price ~925. That’s also ok. But they hold till it reached below 165. What’s logic to hold shit till -80%?.

So don’t go on commentary, prefer to invest by self, even you lose, you will at least learn. If you can’t than - get idea of expenses and see the efforts they are putting in PMS. Efforts is more imp than past record or any other thing - my pov. Past record is distorted.

The small companies like head by Samit vartak, One small cap from south indian guy (Forgot the name) PMS - explore alone with FG if required.