Here is a rear view mirror for a very well known story Of Balkrishna - with unique business model characteristics ( growing exports, replacement focus hence less cyclical , large SKU& client customization , David vs Goliath where it went on increasing world mkt share ) -most of which have resemblance with Pix - including Senior investors here who have ridden on BKT decadal story

- First thing first did rerating happened over journey - quite nicely it did.

-

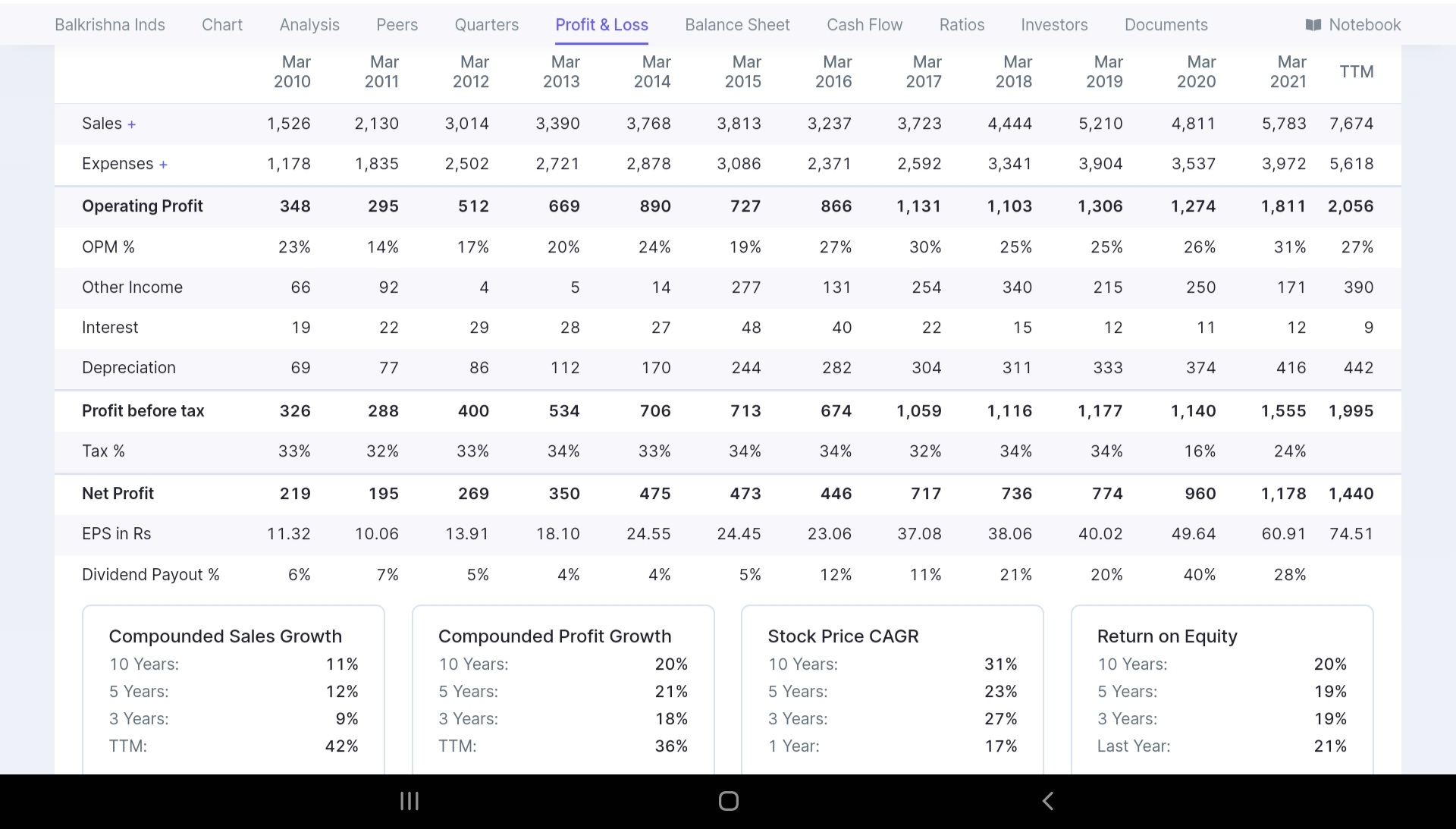

How Was growth quality - did margins improved, sales growth over longer time, RoE? Everything looks good at P&L broadly( looked even better before last few weeks BKT beating after Russia issues over EU focused businesses)

-

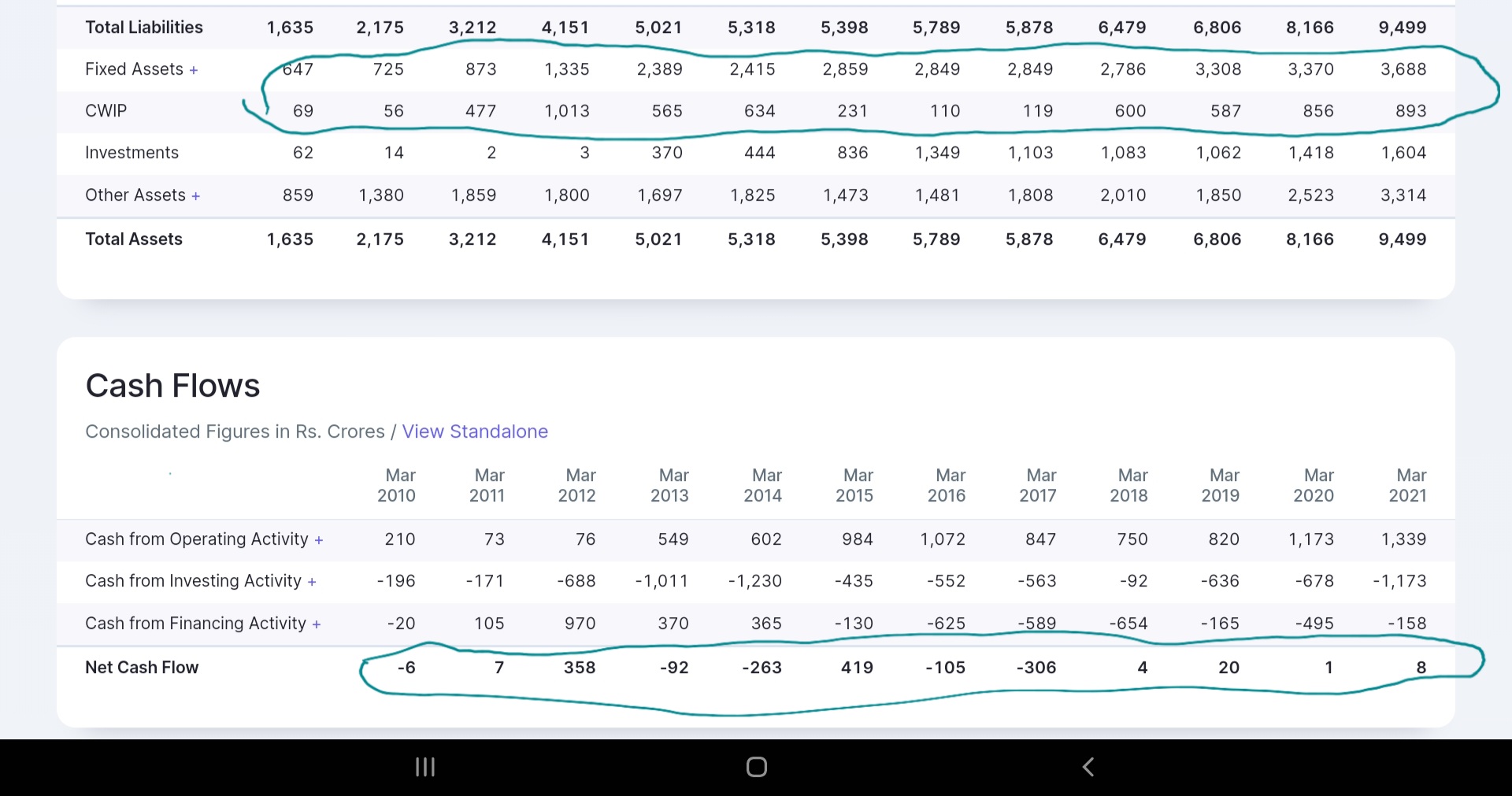

How was growth quality underneath the surface - Look at perpetual CWIP and abysmal net cash flow.

-

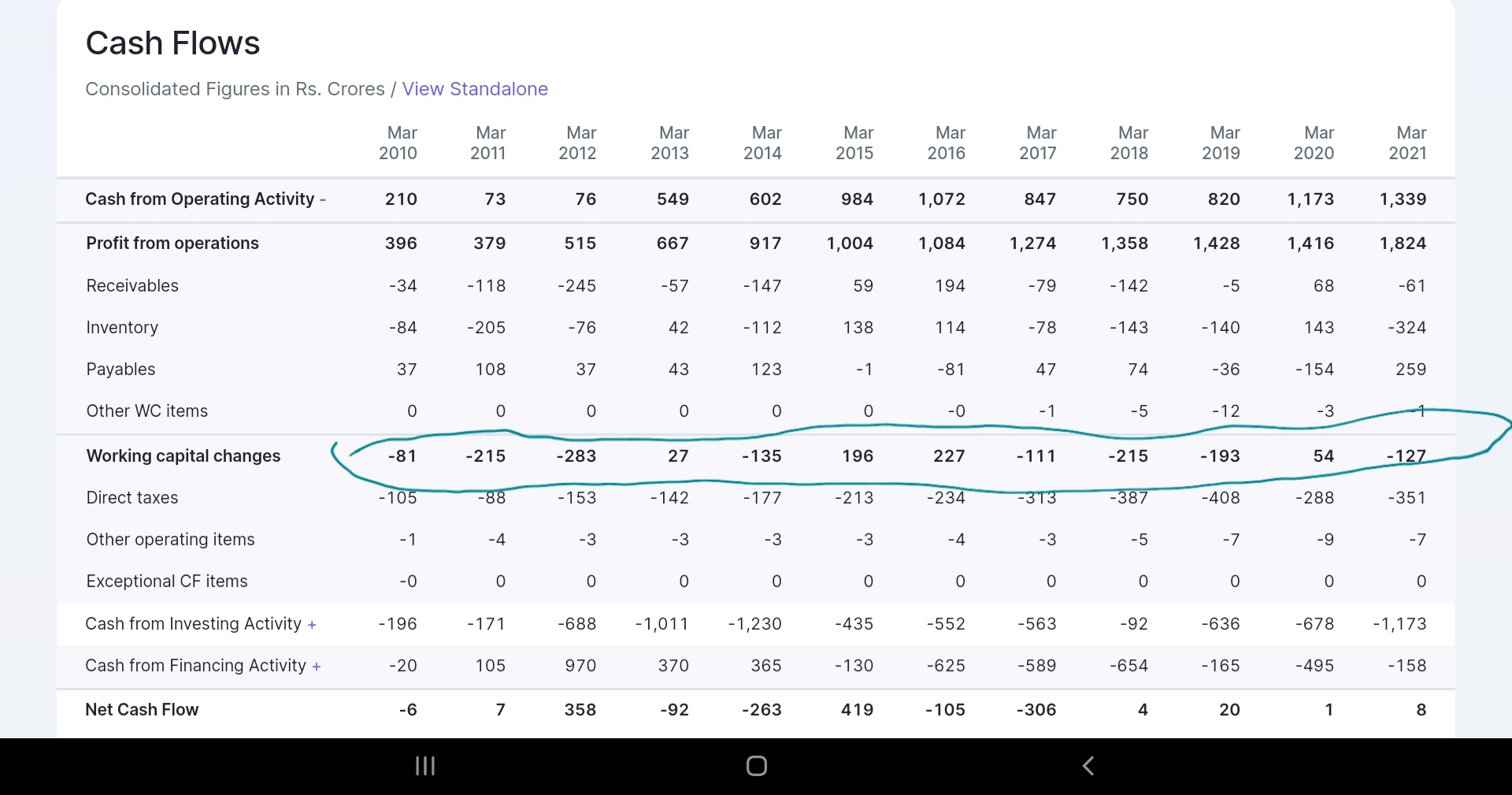

Let’s also look at working capital as well

Summary - BKT had a business model where working capital will grow linearly with scale due to increasing no of SKUs and inventory required. That means free cashflow is unlikely as long as both CWIP and WC grows linearly. Infact Balkrishna WC, Inventory reduction years are when topline degrew/flat.(e.g. 2015 and 2016)- despite that it’s a known compounder.

If Pix has similar excecution & destiny, we might still have a winner at hand despite negligible cashflow and regular Capex. Key will be qualitative aspects of, global expansion driven opportunity size, mkt share gains against competition ( India and global). And ability to show non cyclicality and consistency over longer time frame growth.

Bit far fetched & optimistic expectations but a distinct possibility. BKT thread is a good read.

( Another very good read with wealth of knowledge on quality of businesses

Mayur uniquoters scored as a favorite over BKT per this VP thread due to better quality of earnings( increasing asset turns, higher cashflow, opportunity size etc)

However - it was meant to turn out bit differently ![]() and BKT went on to become a compounder)

and BKT went on to become a compounder)