I understand that the sales pick up in the month of June post the lock down has gained further traction in the subsequent months. Exports are surging & even the domestic sales are almost back to pre-Covid levels. So, all in all, the Co, should have a good 20-21 despite the Covid setback.

3 Likes

Have just received the latest share holders list of the Co. Had recd one earlier in May as well.

Top-100-16-10-2020.pdf (16.6 KB)

Top-100-24-05-2020.pdf (16.6 KB)

4 Likes

Excellent Results

Sales for Qtr increased by 26% from 75.40 cr in Sept 19 to 101.60 cr in Sep 20

Profit before tax increased Increased by 228% from 7.87 cr in Sept 19 to 25.85 cr in Sept 20

Results 30th September 2020.pdf (1.7 MB)

3 Likes

Pix came out with an amazing set of Q2 numbers. It turns out to be the best ever by a long shot. Sales have broken the 100 cr barrier for the qtr for the first time. As mentioned in my post of October 19, the traction in the sales growth has shown remarkable strength & has continued into the current qtr as well (Q3). The 50:50 breakup of Sales between Exports & Domestic is gradually shifting towards higher exports where the margins are superior. PAT of 19.5 crs for the qtr alone as against a PAT of 30.23 crs for the entire previous year (2019-20) puts the results in perspective.

The capex carried out over the last few years have started bearing fruit & the Co. has reduced debt aggressively by about 25 crs since March '20 with negligible further capex. The strong Sales growth could re-rate the Co., given the high operating margins that it enjoys which means a disproportionate growth in profitability with increased Sales, as has happened in Q2. No surprise that the stock was locked at 20% upper circuit today. Despite todays gains, the stock is still available at book value & at a ridiculously low multiple of 7.

8 Likes

Thanks RajeevJRajeev Jawahar for your updates. Can you please throw light on, will revenues and profitability can be sustained give or less minor changes (comparing with this quarter results)?

Management is super good.

Concalls may help for opening another line of communication.

Disclosure: Invested

2 Likes

Cresta Fund - which was holding 1.41Lakhs shares, sold out their entire shareholding (1.04%) in the company in a bulk deal yesterday at 198 Rs (refer bulk deal under pix in BSE).

Seems entire selling was bought ‘on the spot’ by some buyer(s).

Moot question is whether, Q2 was an aberration (one-off quarter) or there is an structural change in the demand/sales of the company’s products?

Company should have been suo motto forthcoming on this point but neither they have mentioned about it in the result’s foot notes, nor have they come up with any ‘press release’ to throw some light on this point.

Any insight on this point by any fellow investor would be highly appreciated.

2 Likes

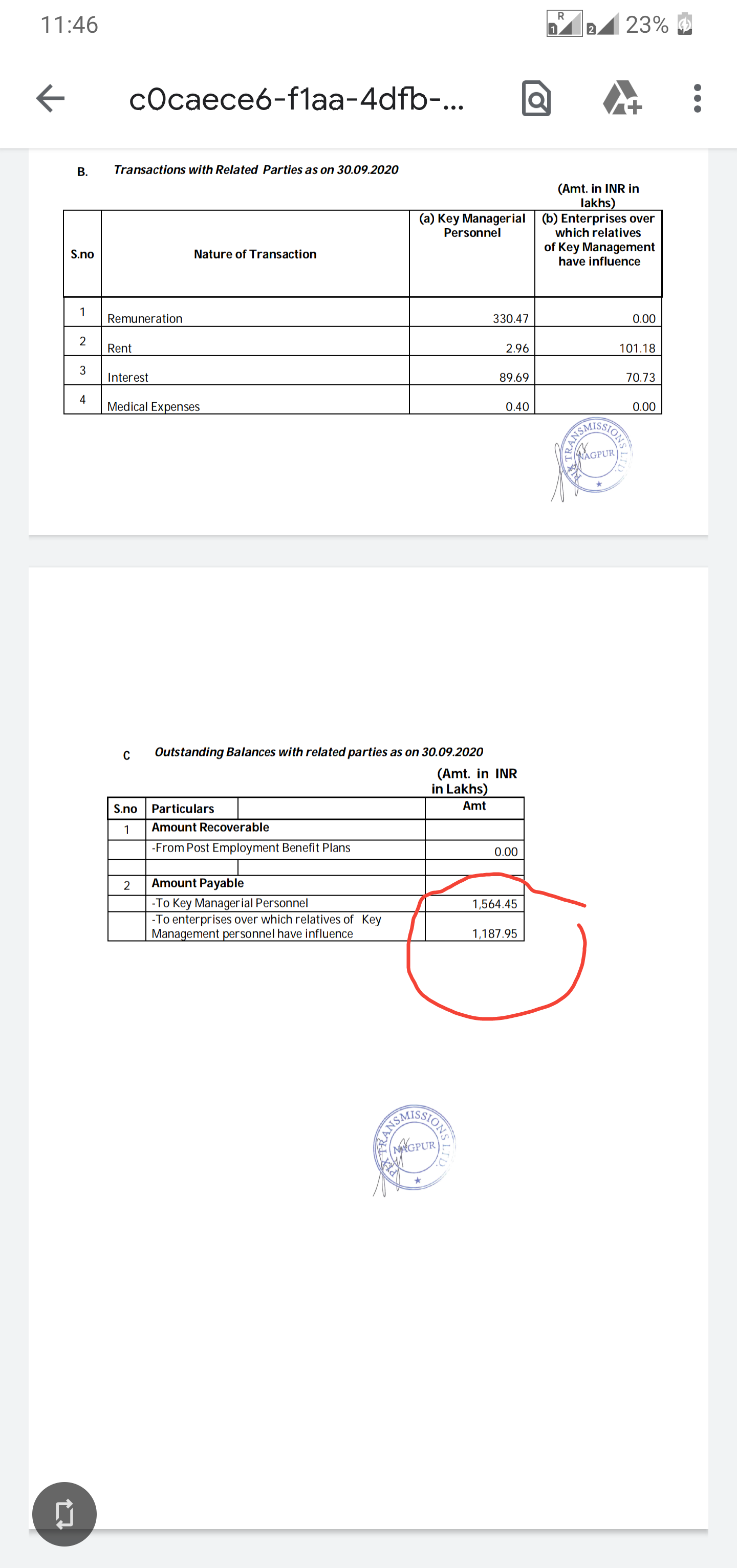

Isn’t this is very large amount or there is nothing to be worried about. This is from recent related party transaction report.

5 Likes

My disclosure first: Today I made my first 400 shares purchase of Pix transmissions(PT),

I came to know about this company through a friend of my friend who worked there till mid 2019, what I will share here is more than 1 year old information which could have changed recently. He has very high respect for management’s focus on quality. PT sells it’s products to some marquee names in India. In spite of stiff competition from established player, PT finds loyal customers. Also, this company exports to developed markets like US, Germany, Australia, UK, Russia and other countries. I believe PT V-belts are used in Garden movers, tractors, helicopters, automotive, washing machines and others. He also told me that PT has repeat customers from these countries. He has no clue about financial aspects.

I extrapolated the information I received and arrived at the following conclusions:

- Garden movers can be considered as consumer items in the western world, in the US, almost every home has 1 garden mover. Companies manufacturing garden movers are very conscious about customer feedback, hence they would do proper evaluation before including any product in their assembly.

- I have limited knowledge in helicopters, but if V-belt is part of any moving parts in an helicopter, I am sure PT V-belts must have gone through a thorough evaluation process

- Washing machines will follow the same logic as point 1

Financials in general are on an upward trend for the last 5 to 6 years. Will keep buying PT stocks on every dip for the next couple of years

9 Likes

I believe it is a matter of concern. Company having annual PAT of 30 Cr showing related party payables of 27 Cr

3 Likes

Need to closely monitor if there are governance issues.

I inquired to company about sustainability of profits, as expected they can not comment on that. “You can be rest assured that the Management is working extremely hard to ensure that the Company delivers formidable results consistently but we’re unable to provide any further insights.”

Let us wait for results or anybody have insights?

According to my estimates, the Co. should do annual Sales of about 425 Crs a year going forward. That is perhaps the new normal. Not to say that Sales in 20-21 would be that much, with Q1 impacted by Covid.

Even if the operating margins revert to mean, with Sales of 425 Crs., the Co. can comfortably do an annual PAT of about 55 Crs with an EPS of about Rs. 40/-. I have considered “Cost of Goods Sold” at the long term average of 39%, instead of about 34% which was the case in Q2. I have further provided for the normal yearly increase in Promoter salaries as well. With no immediate Capex, the Balance Sheet for March '21 would be a lot leaner with further reduction in debt. As stated many times earlier, when Co.'s like Pix, with low material cost & high operating margins increase their Sales, it leads to a disproportionate increase in the bottom line.

I think Pix is now ready for higher levels.

Disc: Have added after Q2 results.

11 Likes

Thanks Rajeev Jawahar for your views. Indeed your views are conservative and should achieve easily by company. Operating leverage can kick in, which may make PIX more lucrative. All eyes on Q3 and Q4 results to have confirmation.

But as always, after confirmation of results, will (hope) not available at this cheap of 8 PE.

Disclosure: Forget to mention on last post as well holding since 2017.

Another strong quarter for Pix. Nice reduction in finance costs too both on qoq and yoy basis.

Company to undertake a capex of 60cr.

Congrats to @RajeevJ for his conviction.

8 Likes

Another great set of quarterly numbers from Pix, much ahead of expectations. For starters, it confirms that Q2 was not an aberration but is the new normal as mentioned in earlier posts. Q4 is the most productive qtr for the Co. so expect a topline in the vicinity of 120 crs. The Co. is well on its way to doing an EPS of about 45 in the current year (2020-21) itself. Markets are forward looking, & even at the current run rate could comfortably do an EPS of 60 in 21-22.

With strong momentum in sales, the mgt is going for an expansion to the tune of Rs. 60 crs to take care of future growth. As the sales grow, its only a matter of time before Pix comes in the notice of the big boys. There would be few companies earning the kind of operating margins that Pix enjoys & at the same time available at these valuations.

Looks good for higher levels despite the recent run up.

11 Likes

Pix announced expansion plans of about 60 crs. to be carried out over the next 12 months or so. This includes a state of the art centralized logistic hub which will store the finished goods of all the different plants. This will greatly reduce the turn around time for the containers that come to take the goods. As of now each container has to go to the different units for collection slowing down the whole process.

The still bigger impact of this logistic hub would be in releasing plant space in both the existing units currently used for storing finished goods, which can now be used for the proposed expansion at the respective plants. This is a big advantage as it makes the expansions brownfield with the entire infrastructure already in place, resulting in huge savings both in terms of development cost as well as the time taken as would have been if the expansion were to be greenfield i.e. setting up a new plant altogether.

The Co. expects the logistic hub to be ready by August 2021 which means that the effects of the expansion would be felt in the latter part of 2021-22, even though the full expansion would be completed only towards the end of the financial year. The rubber mixing plant is also being expanded, which only a year or so was looking at job work opportunities to utilize full capacity, is not being expanded to take care of the Co.'s growing needs.

The next couple of years should be years of growth & excitement for the Co.

28 Likes

The Agricultural sector is a major growth area for the Co. The attached video will give some valuable insights.

Belts are not a commodity product. As is clear from the video, each type of belt has a different construct & this video is limited the Agricultural sector. Pix has presence in about ten different verticals.

20 Likes

Rating update: Revised from Stable to Positive.

Disclosure: Invested

3 Likes

Hello everyone. I found this great article about PIX Transmissions that provides lots of key insights, especially regarding corporate governance red flags.

https://www.drvijaymalik.com/pix-transmissions-equity-research-report-fundamental-analysis/

Hope other VP members find this helpful.

1 Like

Ratings revised by CARE is significant as it confirms that the Co. is going from strength to strength.

Financials improving while the Co. is in the midst of expansion is not a very usual occurrence.

2 Likes