Not much to add on fundamentals with excellent data points in thread above from @RajeevJ @sahil_vi. And fellow VPers.

Promoters continues to increase share holding every quarter - albeit smaller pace

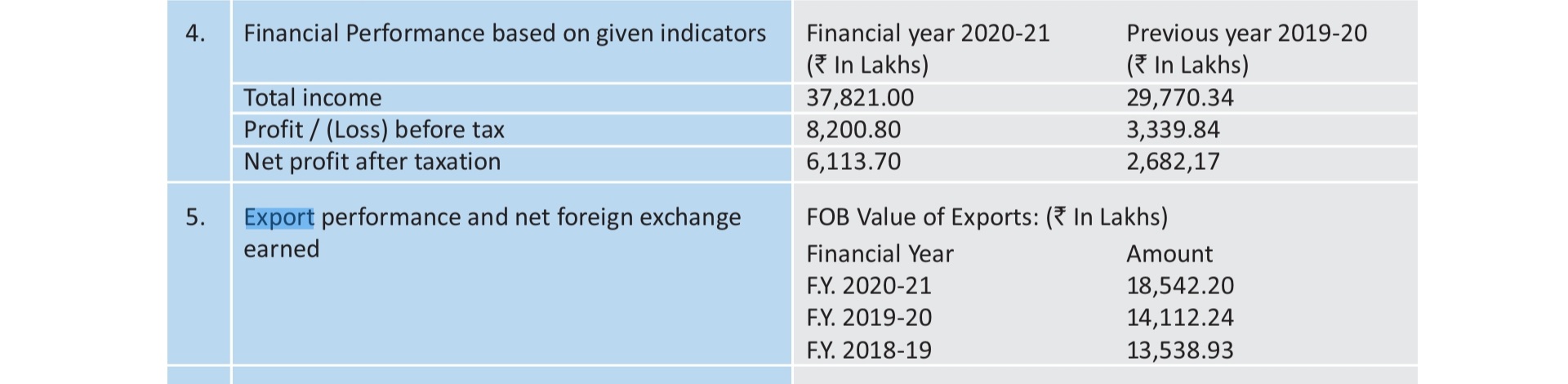

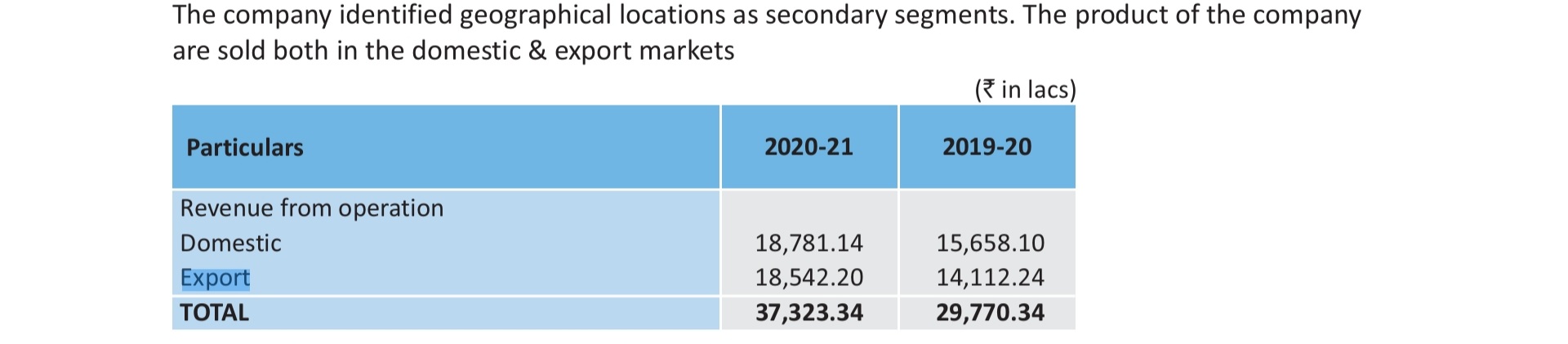

Higher Export mix seem to be reason behind margin expansion, faster export growth than domestic - small data set from AR but seems logical explanation of margins expansion in a tough year, besides Op leverage and pricing power. Also export seem to be on FOB basis thus no impact of global shipping turmoil.( FOB - FREE ON BOARD)

- Margins per recent quarters trend seem to stabilize around 26-27%, gaining market share while delivering high margins surely reflects excellence in execution.

On technical seems to be in narrowing triangle pattern with 5+ months consolidation, currently near breakout point - stable in last few sessions volatility

Company may be eligible for MEIS credits, scheme is being replaced with RodTEP and can help boost bottomline as transition to new scheme seems WIP - applicable to all exporters. ( basis NIC code)

- Q2 21 to Q2 22 performance looks subdued on bottomline ( flat bottomline vs 20% topline growth) on account of elevated margins in Q2 21, going forward since Q3 21 was at normal margins hence Q3 22 to look decent numbers in line with topline growth.

All in all a good Capex cycle play with large opportunity size relatively to Pix current size n scale. Being a microcap, rerating has been swift in last few quarters, runway for growth and potential to rerate further as long as they deliver.

Besides numbers it’s a good business model with customers stickiness resulting from customization reqmt for each customers, Opex play from customers lens thus consumable with repeat business, requiring large no of SKUs with growing customers base ( to some extent reminds of BKT model - Balkrishna tyres).

Added in recent correction.