To be fair, the analyst categorically said in the video that he likes the pharma business of PEL. However, he is definitely not enthused by the lending arm. Also interesting is that he says JM Financial real estate lending has been much better (so he might not be biased against real estate lending in general).

3 Likes

Some Brokerage views

3 Likes

Thanks for sharing the detailed video. Part of intelligent analysis is to analyze the presented info with reference to wat one already knows before-hand. Another part is critical analysis whereby looking at the presented info critically helps in garnering insights.

With all due respect, the analyst btw seems to have gone thru pure ratio analysis in classifying the NBFCs. A screener.in run with ROE ranges from high to low would have given same classification to anybody.

Wat he missed out and wat’s to consider are these imp points - ( In general for NBFCs and in particular for Piramal )

-

Reversion to mean and Narrative fallacy are still powerful enough universal laws. Some of the NBFCs categorised in non-Evergreen classes are those whr certain things didn’t worked out as expected over last few yrs. They are cognizant of thr underperformance\mistakes and are taking steps to strengthen themselves for future. Money will be made whn thr delta improvement will result in revision frm thr present valuations.

-

In banking and NBFC industry, conservatism and prudence is of far more value than pursuing pure growth. Some of the non-evergreen candidates in the list e.g. JM Financial are those cases. Yes, they might have lagged in growth in recent times but at the same time the’ve managed to strengthen thr balance sheets which prepares them for next leg of business cycle upturn

-

Speaking specifically for Piramal, they’ve done thr cleansing part and somewhr it was the strength of thr pharma business which helped them tide over the tough NBFC business phase. The valuations at this point seem reasonable enough to provide good returns over medium term vis-a-vis the businesses mentioned in evergreen category whr the valuations fully price in the expectations.

2 Likes

That is precisely the point I am trying to make. PEL is not a fully NBFC nor Pharma. Hence it is not good idea to paint PEL with the same brush as with other NBFC. If there is a separate NBFC for PEL, then I could understand, but now that is not the case. But that does not prevent people from generalising.

By the way, this is fertile ground for people who would be understand the business in great detail and capture market efficiencies.

Just to be very obvious- I am not referrring to the above analyst again, but this observation is in general.

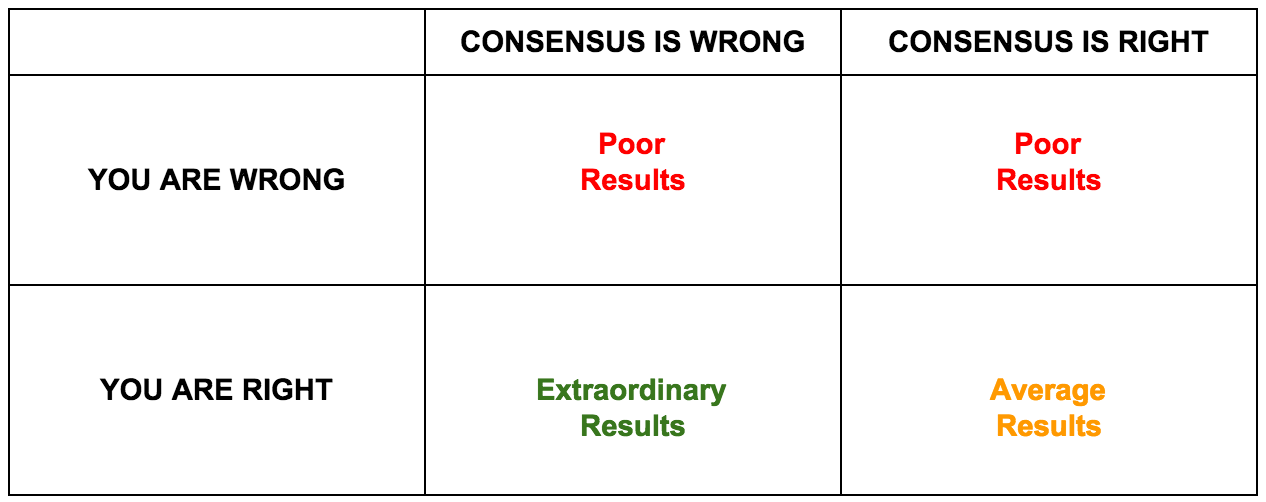

The thing is whatever he is talking about is consensus, All the stocks in good category already trading at 4-8 x book and all the stocks in bad category (like PEL) are trading around 1.5 book or below.

Nothing extra insight he gave that saying " This nbfc market thinks is bad but due to xyz reason markets perception is wrong (trading at or below book) ".

Although he gave some beautiful insights & consensus views about why something is trading expensive & why something is trading cheap.

but he almost sounded like some businesses models are too good to be disrupted (which i disagree) .

Anyways if PEL will be able to prove that although they did some risky lending but not as much as markets think & they have learnt which will enable them to not make same mistake again meaning creating more value adding growth in future then consensus view will change. And you make extraordinary returns only when you are right & consensus is wrong -

Anyways Piramal is known to pull of one amazing “billions of dollar deal” every decade, today its DHFL it needs to be seen if this goes through but if it does there will be re-rating of the stock for sure.

and i don’t think they were as reckless as PNB in builder financing or as good as HDFC but these are highly rational , smart people like of Khushru Jijina who know mumbai real-estate market really well (better than average market participants) to play with risks. Remeber he used to run Piramal reality - then they realized financing might be better business & started financing operation.

Lets not put the guys like Khushru Jijina , Ajay Piramal into the management category of DHFLs , India bulls or PNB or even guruth. (but this analyst in the video bucketed them into that category - that’s the problem i have with analysts who like to work with excel )

PEL acted fast in de-leveraging for IL&FS default company looks much healthy today, A lot of risk mitigation work has gone in last two years - in terms of selling portion of book and raising capital.

It has to been seen but if i have to bet on turn around i’ll look for guys like piramal otherwise betting on turnaround is foolish in general.

may be this will help -

11 Likes

The story is playing out perfectly (or even better)

- Real estate up cycle means nearly zero NPAs for Q4 and potentially going forward

- PELs demerger may not be far off i think

- Consumer finance groundwork also in progress

- Re-rating of price-book multiple on the cards because of all above

My biggest holding. Reduced 1/3 after three days upmove

Can someone clarify the unallocated equity part as mentioned in equity allocation presentation.

It says 12,375 crs. - includes investment in Shriram Grp, DRG receivables and Deferred tax assets. Now as per info : -

Invesments in Sriram Grp - 3000-3500 crs.

DRG cash - 6000 crs.

So does that mean deferred tax assets are total of arnd 3k crs.?

This is what my point was - Even if Some luxury apartment builders primal funded are in trouble, they have enough brand equity / reputation to even come to markets raise equity - (These are not not fool that they funded dud projects / chor builders - Lets not put them into the bucket of DHFL, PNB etc )

1 Like

Lodha IPO, as mentioned above by @AmitContrarian shall a go a long way for PEL.

As of Q3, PEL has exposure of 2600 cr to Lodha. With some refunds coming from Lodha (after successful IPO, when it happens) will release equity for PEL.

Lodha is a single biggest risk for PEL due to large exposure. IPO, along with debt restructuring (created SPV as mentioned in Q3 call), it is likely (imo) that PEL’s exposure to Lodha can be reduced in half in next 12 months to around 1500 cr.

It may be first time after 2.5 years or so (post ILFS fiasco), that PEL is amongst top 10 large cap shares purchases of mutual funds for any month. From the recent run up, it seems similar trend is continuing for February. Good sign for the days to come.

Disclosure - my single largest exposure… holding for last 3+ years. No transactions in last 6 months

holding for last 3+ years. No transactions in last 6 months

6 Likes

2 Likes

From the below article:

By March, we expect the Lodha exposure to be around ₹2,500 crore, which will be split into two. One will be to Lodha, exposure to which will be around ₹1,000 crore or lower. And the balance will be an SPV exclusively charged to us which is fully ready inventory. It will help us monetise quicker and stay away from the insolvency and bankruptcy risks

3 Likes

Piramal Enterprises_Motilal Oswal.pdf (728.8 KB)

2 Likes

With DHFL takeover and Lodha IPO, this stock could show its full potential in the next 3 months i feel.

2nd largest position now & ready to buy the dip.

Q3 & 9MFY2021 Earnings Conference Call - https://www.bseindia.com/xml-data/corpfiling/AttachLive/fd28f2fa-5bf6-41c9-92ee-36fa74f27e4c.pdf

or

https://www.piramal.com/wp-content/uploads/2021/02/PEL_Q3-9M-FY21_Transcript_vFINAL.pdf

1 Like

What will implication for this on existing bid for DHFL? ET is quoting fraud of 6100 cr.

Piramal did not pay for the corporate book i think - they only got the retail one.

Above news is not relevant.

Piramal also get the corporate book, but it’s heavily marked down as per concall. So should not be significant I think

PEL has made the bid based on the available information at the time of bid. However, as per the article the fraud came to light only yesterday, so it is likely that PEL might not considered the above traction in the bid.

Additionally, the amount is not small. Even though they have marked down (in assumption) wholesale business, 6000 cr is not a small amount and it does change assumption.

I think this is the downside of going for big transaction. One small transactions like this could be fatal.

2 Likes

according to the concall, DHFL’s wholesale book will be hugely marked down from the Rs 28,000 cr claimed by the erstwhile management.