#CNBCTV18Market | Piramal Ent slips after ED raids Omkar Builders in Mumbai. Piramal has tie-up with Omkar Buiders for a few projects pic.twitter.com/QrpsAFgpX1

— CNBC-TV18 (@CNBCTV18Live) January 25, 2021

any one knows whats going on with the DHFL acquisition ? Not hearing much about it …

It looks like an interesting deal that could add 5000 to 8000 Cr to revenue on capital deployed around 37000 Cr

Huge Q is will it go through ?

so far there is no news of Oaktree legally challenging Piramal’s take over of DHFL. So all eyes on NCLT’s court which will decide by the end of this financial year.

Big question is whether Piramal wants to lighten its wholesale book which will get heavier with the merger with DHFL. Will there be a white-knight who will be interested in the wholesale book of the merged entity? Its a Rs 60,000 crore question!

disclosure: holding Piramal and hence biased.

Why NCLT has to wait till March i don’t understand, this has be going for a while already more than a year.

I think some NGO FD holders went to High Court, that could be a reason.

lenders, including FD holders, want recourse to the proceeds recovered from the Wadhwans that were fraudulently siphoned off from DHFL. It is not clear as of now who will gain access to the recoveries from the erstwhile promoters.

Have a look at this video. PEL has lot of challenges to face even if they secured DHFL. Retail depositories, FD holders, NCD holder of DHFL may come back consuming PEL’s energy.

Moneylife has given lots of details about this deal, although they are from DHFL side.

I think it will be a miracle if Oaktree does not challenge the decision. They have said it openly in a letter that they may challenge the decision and the decision has gone what they feared. India is on Oaktress’s horizon, so they would not leave this case without giving a fight.

PEL is acquiring DHFL via the IBC process and hence will not be responsible for creditors.

The way I would look at is roughly 5,000 to 6,000 Cr. of income against a cost of 3,500 Cr. (Rs.37,000 Cr. of acquisition cost is also directly/indirectly debt funded at Piramal’s cost of Debt of 9 to 9.5%)

So you would be making a net profit of 1,000 Cr. on the book and this book would get paid off in 7 to 10 years so you would make further profit of 20,000 Cr. This would be an equity available to them for further growth.

Further indirectly Piramal would get a benefit in improving its Rating and reducing the cost of debt by 50 to 100 bps over the next 2 to 3 years as its book would now be a diversified book and I expect a rating upgrade. Also, funding cost also to come down as PEL would have developed good connect with all the major lenders of DHFL (they would now lend to PEL at lower rates). Which should again add Rs.250 to Rs.500 Cr. to the existing book of Piramal.

So overall a very profitable trade for Piramal. If somehow Piramal learns from the NBFC crisis and stops lending in an aggressive manner - after HDFC & Kotak they are the only NBFC of substance which has survived (DHFL is gone, Indiabulls, Motilal and Edelweiss are no longer what they were). They should be able to grow their book to 2 to 3 lakh crore without any equity raise.

In one stroke their aggressive and reckless lending of last 4-5 years has been made good.

I see there are some legal issues , specially related to fraud money which is getting investigated.

Not sure how things going to pan out in terms of duration, its a highly complex case.

Agree -

- Diversification away from real estate / wholesale lending, leading to improved rating,is the major tenet of re-rating of this stock

- Another key point is that the real estate exposures themselves would have lower NPAs and provision write-backs due to improving real estate cycle (upcycle)

Good days are coming for this company i think - can move up to 2500 in 3-6 months

Disc: invested. my largest position since 1200

While the market is focused on DHFL acquisition, Piramal is moving ahead in pharma divisions as per the news below

Q3 Result. PAT of 799 cr.

25% drop in finance cost (Y-o-Y) is the biggest highlight for this quarter in my opinion. So looks like business is slowly regaining its momentum

Another highlight is move towards separating two companies. I think this will become a key point as PE is on board.

“We are in parallel, making strides towards creating a large differentiated listed Pharma company, post the growth capital raise from The Carlyle Group, through both organic as well as inorganic investments. These are focused steps towards a shift from a multi-sector conglomerate structure into one with focused listed entities within the Pharma and Financial Services sector”

Ya good for shareholders…but isnt the demeger some good 2 or 3 years away?

Q3 Con Call Notes.

Financial Services

Undergoing Multiple Transformation

- First- Wholesale based to a well-diversified financial services business.

- Retail will be 50% of the business. This will be through organic as well as DHFL.

- DHFL will aid with additional branch and customer reach.

- Launched 6 products and will be launching one product every month.

- No disbursement in Affluent Housing Busines.

- With Real Estate (RE) we do not expect any NPA going forward (immediate future).

- We do not expect any growth in Wholesale at all.

- All growth shall be from Retail Segment.

- Retail loan book 5300 cr.

- Move from concentrated to Granular exposure.

- Moving from high debt to high capital adequacy ratio.

- Moving from Regulatory to Conservatory provision ratio.

- Net Debt/Equity- 0.9.

- FS (Financial Services) does not need any capital requirements for next 3 to 5 years.

- High Cost of Funds- Overall, it will come down as we move toward retail lending more.

- Personal Loan Segment-

- We are in the urban market. Have not gone to rural market yet. This is just a trial period.

- There more fintech partnership are line-up for secure and non-secure products.

- Want to be well-diversified across partners.

Asset quality

- One Time restructures- 740. cr (3.8% of loan book).

- Only one RE structure is getting restructure.

- Other infra/hotel and other non RE.

- One in RE/Hostile/Infra- We do not expect any more in Q4.

- Auto ancillary section. We are liquidating the business to get money back. Exposure is 430 cr

Conservatory provision 2900 cr. Believe this is more than adequate to take care of Covid related stress.

DHFL-

-

We are examining DHFL Wholesale book (28 K DHFL wholesale). We believe there is an upside.

-

Wholesale (Gross Block)- Much more than 28, 000k. We are assigning lower value.

-

Network- Around half of our branch is good position. This is based on known public available information.

-

Retail- AUM and securitisation–> Around 28,000k. We do not anticipate significant markdown.

-

DHFL Integration Timeline

Application to RBI for clearing proposal. Expect approval in a couple of weeks

Then NCLT.

The proposal may go to April may assuming no litigation.

Around June we shall be able to consolidate into our business.

Single Borrower Exposure

-

The overall reduction in top builder payment-

-

All our exposure are bringing down.

-

Top 10- Steady fall Q0Q.

-

Lodha- 3200 to 2670 in Q3.

Split into two.

Moved our loan to SPV-

Exposure to Lodha builder- around 1000cr.

Exposure to Residential housing remaining exposure.

Pharma

- PEL planning to organise Pharma day virtual event in the current month.

- Revenue grows at 15CAGR since 2011.

- EBITA growth 31 CAGR.

- CDMO showing good growth demand. Intend to invest organically and in-organically.

- Started invested organically and inorganically.

- Margin Expansion-

- Significant expansion is happening.

- This will drive margin as they are operating in the niche segment.

- With Carlyle, we can leverage with the acquisition if needed, in case of big acquisition.

- Q2 CDMO was lower and Q3 lower, but Q4 will be higher.

Hospital Genetic Business

- Impacted. Expect getting better in new few quarters.

- PEL finding lots of opportunity for inorganic.

- Big backlog of surgery. This business shall come back in Q1

Note- I have scribbled notes during the call. Please feel to correct/amend

From yesterday’s concall, it seems the demerger is not far off. Since financial business and pharma business are now segregated into 2 entities under PEL and both of them are flush with capital, I think demerger can happen post DHFL merger into Piramal Capital & Housing Finance. If no legal challenge to DHFL acquisition, I guess demerger can happen as early as 2022.

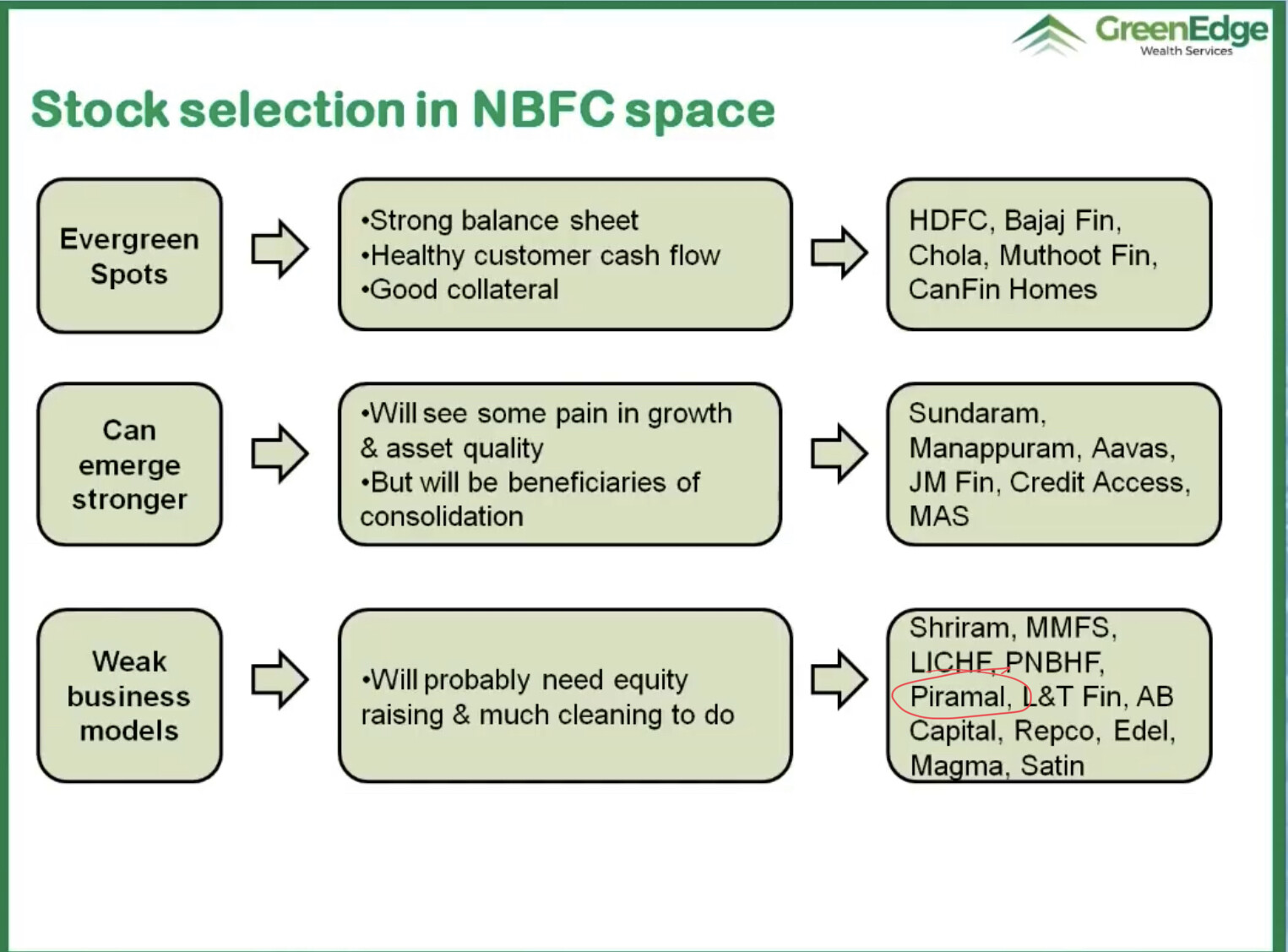

There is a fantastic session on NBFC Sector Youtube by Omkara where an analyst have deep dive into NBFC sector. There is the last slide on the presentation which I would like to dwell for a min. Putting it here due to the relevance to PEL

The presenter has deep knowledge about the sector, and he does not have high regard for PEL, which is fair. We know how PEL has performed in the last few years and how they grew in Real Estate business rapidly, and it is public knowledge. We have discussed this on this thread on this great at great length. I would agree to his critical assessment that of PEL.

Over many years, I have seen analysts and so-called experts (I am not picking on the above analyst) tend to paint the whole sector with same brush. By the way, this is not only an India phenomenon, but it happens globally all the time and offers an excellent opportunity for an investor who knows who plays the game well.

Take an example here. The analyst has negative views on PEL, but PEL is not only an NBFC. In fact, even today, around half of the profit is from Pharma, which is ignored. If the Pharma business is separated today, I won’t be surprised if there is a scramble for people to get their hands on the Pharma business. I am sure he is not the only person doing it, but many experts call the same verdict wrt PEL. However, for the investor, what matters is what is in the price.

Many experts (analyst) focus on what is hot and good to talk. Until last years, not many people were talking about Pharma. It was hard to find people/analyst/experts who has positive views on Pharma.

Same can be observed in the IT sector in the last five-seven years. Many analysts/expert were worried/concerned about the single-digit growth of Big IT players that they had an average view on the market.

And once a sector turns and eventually (it turns), the whole lot goes up (Hide Tide Lift All Boats) e.g Pharma, IT.

I think something similar shall play out on NBFC sector.

I am hoping so, but if I go back in history, this has happed many time before and I have a reason to believe to this time won’t be different. David Dreman has made a fortune by following contra investment strategies, and S Naren has beautifully explained the same concept with Indian example in the current context. I think the NBFC sector as such will eventually bounce back. However, what happens to PEL is very much dependent on how PEL adapt to changes.

Note- Invested and views are biased.