Entrepreneurs take risk to grow their companies…some ventures may work and some may not.what would have happened if RIL just stayed with petchem business…what is the EV of Jio now…what if M&M only stuck with manufacturing of tractors? we simply buy some shares and think we know better than the promoters and call him he should have put money in that business and not this…atleast i think he has skin in the game…just leave share price performance for a minute…how many good ethical corporate companies we have in India?I still think he will weather this out…

11 Likes

Reading complete shows that they are quite prepared to face challenges up ahead.

but would they really be able to compete against the set and default players of HFC, NBFC with their venturing into new type of loan distribution areas?

What shows they are prepared? Asking for moratorium when your peers like JM and Bajaj finance are not asking?

Even large corporates are opting for moratorium eve if they dont need, everyone just wants to keep extra liquidity.

OK what about JM>?

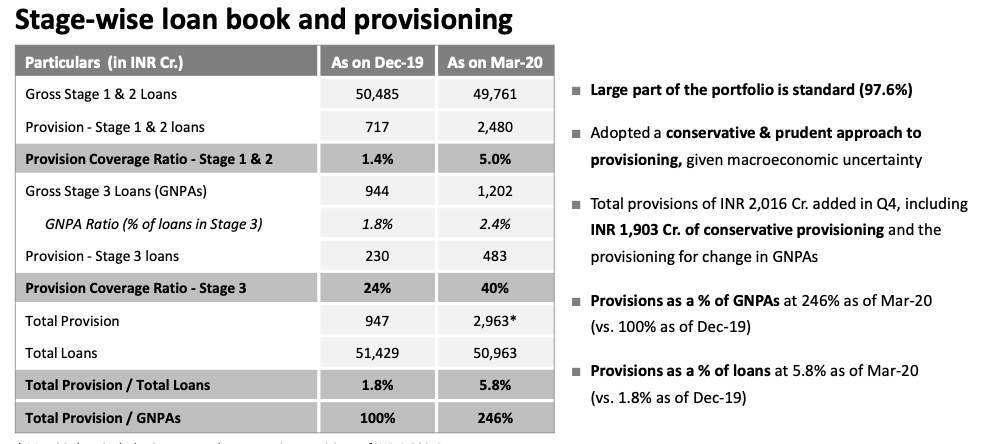

Also what does it show when your top clients whom you have lent to are omkar and Lodha? If you have massively increased your retail housing finance book in a year and your part of the wholesale book is under moratorium what is your net NPA figure? Look at December 2019 concall and results.

pdf copy of concall for Mar 20 results submitted to BSE

Omkar direct exposure is 0 now; Lodha is the biggest RE developer in India

These two should help the company to get adequate liquidity and ride out the storm. Add to this 4000 cr in cash and cash equivalents, 4000cr already drawn and 4000 cr more available in bank lines and 1000cr LTRO

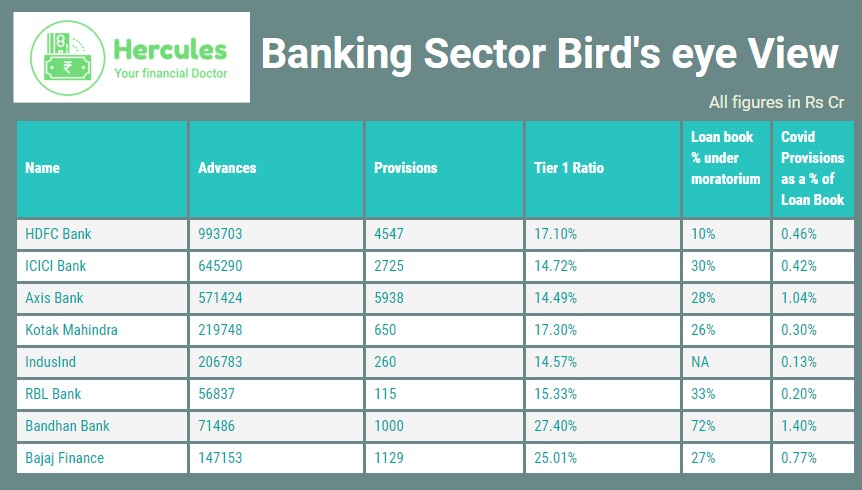

Comparison of Piramal’s Covid-19 provisioning vs other lenders:

-

Piramal has provided for nearly 4% of their portfolio going bad whilst the highest amongst other lenders above is 1.40% for Bandhan Bank, a micro-finance lender which has to deal with both Covid-19 + Amphan cyclone now.

-

Piramal’s entire portfolio is secured unlike these guys. Yes - their loan book is chunky, real estate has been under tremendous pressure, some of their developers are stressed - but there are also some reasons to believe Covid-19 might spur demand for real estate (desire for hard assets after market crash, work from home, all time low mortgage rates, NRIs moving back etc). Developers should be able to clear their ready inventories if they slash prices meaningfully and Piramal has the money and execution ability to help them finish unfinished projects or even complete these projects themselves.

-

As noted in my earlier post, Piramal has enough liquidity to run their business for even 12 months with 0 repayments in the financial services business.

-

They have paid out a decent dividend (after taking all this into account). Net debt to equity at 1.2x is probably the lowest in the industry.

-

With the above in mind, consider Piramal’s balance sheet vs. current market cap.

Assuming they have to allocate 100% of the unutilized equity to the FS business, acc to my calc the market is pricing ~55% of their loan book of 50,963 cr going bad currently (including ~4% already provided for).

This doesn’t seem reasonable to me which is why I remain invested + cautiously optimistic (together with qualitative factors like accounting quality, promoter skin in the game, large institutional partners and potential Piramal-Jio synergies going forward).

The biggest downside in Piramal aside from the obvious is their inferior liabilities profile - they really need to develop a low cost stable funding base like HDFC, Bajaj Finance if they want to do well long term.

Disc. Invested, no transactions in last 30 days

4 Likes

Isn’t it more like 3.7% Covid-19 provisioning? Since we are comparing to other lenders’ Covid-19 provisioning (and not total provisioning)

I think perhaps the market is pricing in not just dismal performance of its developer financing book, but also a misadventure on the upcoming retail focused fintech business, where they would be competing against formidable entrenched entities.

Yes thanks! Needs to be like to like, edited my post.

… going by comments on Twitter I think people have basically written off their FS business and put them in the same bucket as DHFL, Indiabulls, Yes Bank etc ![]()

1 Like

Any idea on what is the loan moratorium as a % of overall book for PEL? I saw it at sub 10% level. Is it correct?

About 80-90% of wholesale borrowers and about 20% of their retail housing finance book have availed moratorium.

Source: Q4-20 concall transcript: https://www.google.com/amp/s/finance.yahoo.com/amphtml/news/edited-transcript-pel-nse-earnings-061728088.html

Disc: Invested

“80-90% of wholesale borrowers availed moratorium” …can you please explain this is impact terms?

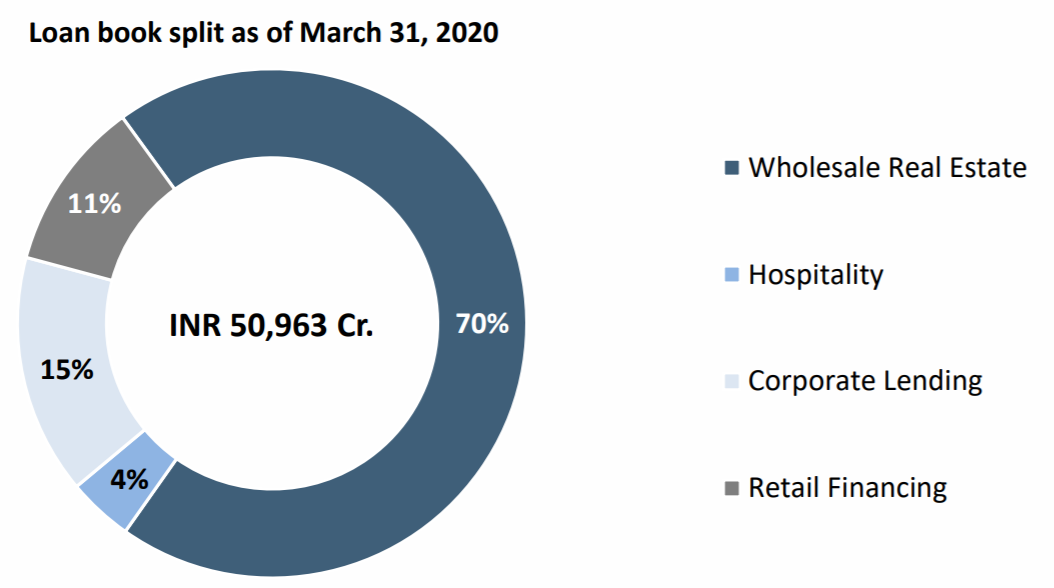

Here is Piramal’s loan book as of 31st March 2020. The overall book is ~51K Cr of which Real Estate book is 70% and retail is 11%.

Of the retail loan book of 5600 Cr, 24% is under moratorium. On the wholesale real estate front, out of the ~36K Cr loan book, most developers (mentioned as 80-90% elsewhere in the concall - not very clear) have availed moratorium. The concall isnt clear on what proportion of the remaining loan book (corporate + hospitality) is under moratorium, but given the stress in those sectors in general, as well as Piramal borrower specific issues (e.g. Mytrah), it is likely that most of those loans are also under moratorium.

So to summarise, the bulk of the loan book is under moratorium and with RBI extending it by another 3 months, I would assume that the risk of default in future would only increase.

4 Likes

and with that default rate, headache for Piramal is also going to increase. That’s bad for PEL even if are trying to be more diversified (reducing in real estate and increase in other areas)

However, they have loans with big names so chances would be less.

Need to watch. Thanks

Most important statement in the news is given below

Carlyle’s offer would value the business at around Rs 20,000 crore ($2.6 billion), almost as much as the Rs 23,131.21 crore current market capitalization of the combined businesses.

I believe this could become turning point for this stock, which got severely beaten down due to head winds in real estate sector in past 2 years whereas completely ignoring thriving successful pharma business which contributes almost 50% of the company’s revenue.

6 Likes

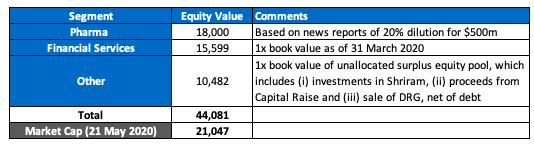

@Marathondreams - such deals generally quote enterprise value and not equity value which is enterprise value net of Debt. Most probably Carlyle would be valuing the company on Enterprise Value of ~Rs.20,000 Cr.

We need to net off the Debt to get the equity value of the Pharma Business. Pharma has rougly Rs.5000 Cr. of Debt so equity value is ~Rs.15,000 Cr.

So market is valuing the financial services business at ~Rs.7,000 Cr.

With equity of Rs.13,000 Cr. and Cash of Rs.4,000 Cr and investments in Shriram Group of Rs.5,000+ Cr. financials are been given a discount due to likely loss. I feel they would need Rs.4,000 Cr. to Rs.10,000 Cr to clean the book. Which nets of the available cash and investment in Shriram Group.

So its trading at 0.7x of P/B. Not to bad for a business which has a lot of uncertainty at this junction.

5 Likes

Piramal Pharma Solutions Announces Acquisition of Solid Oral Dosage Drug Product

Facility in Sellersville, Pennsylvania from G&W Laboratories Inc.

Disc: Invested.

1 Like