JM financial is not seeking any moratorium and doesnt plan to also as per yesterdays call. Piramal if seeking moratorium doent mean they will default but definitely cant be going into new businesses. If you need moratorium for 3 months of liquidity that is not the time to start going into a new segment like consumer finance.

4 Likes

There is a long list of almost all NBFC asking to give morataurium from banks. This is to push rbi & banks to recognise them as eligible borrowers and rules should not single them out. Banks obviously don’t like NBFC as they are competition. The NBFC industry in total is pushing for morataurium as it helps liquidity planing in these times. Wont be surprised large ones like Bajaj also write to banks. Piramal consumer finance launch is before Diwali before Ecommerce sale timing. Money is no issue for Piramal. All good AA /AAA in this market get money. It will be interesting to see Q4 results commentry and q4 corporate presentation.

Piramal Q4 results are on 11th May , i.e Monday.

No one asks for moratorium for the sake of moratorium and that too just because other below average NBFCs are asking for one . Its contradictory to say money is no issue for piramal while it is asking for moratorium. Again im not saying it will default but the fact is better NBFCs are not asking for moratorium. And when i say Better obviously they are few because by definition average and below have to be more. I dont see HDB, HDFC, JM asking for moratorium. Quality is Quality.

1 Like

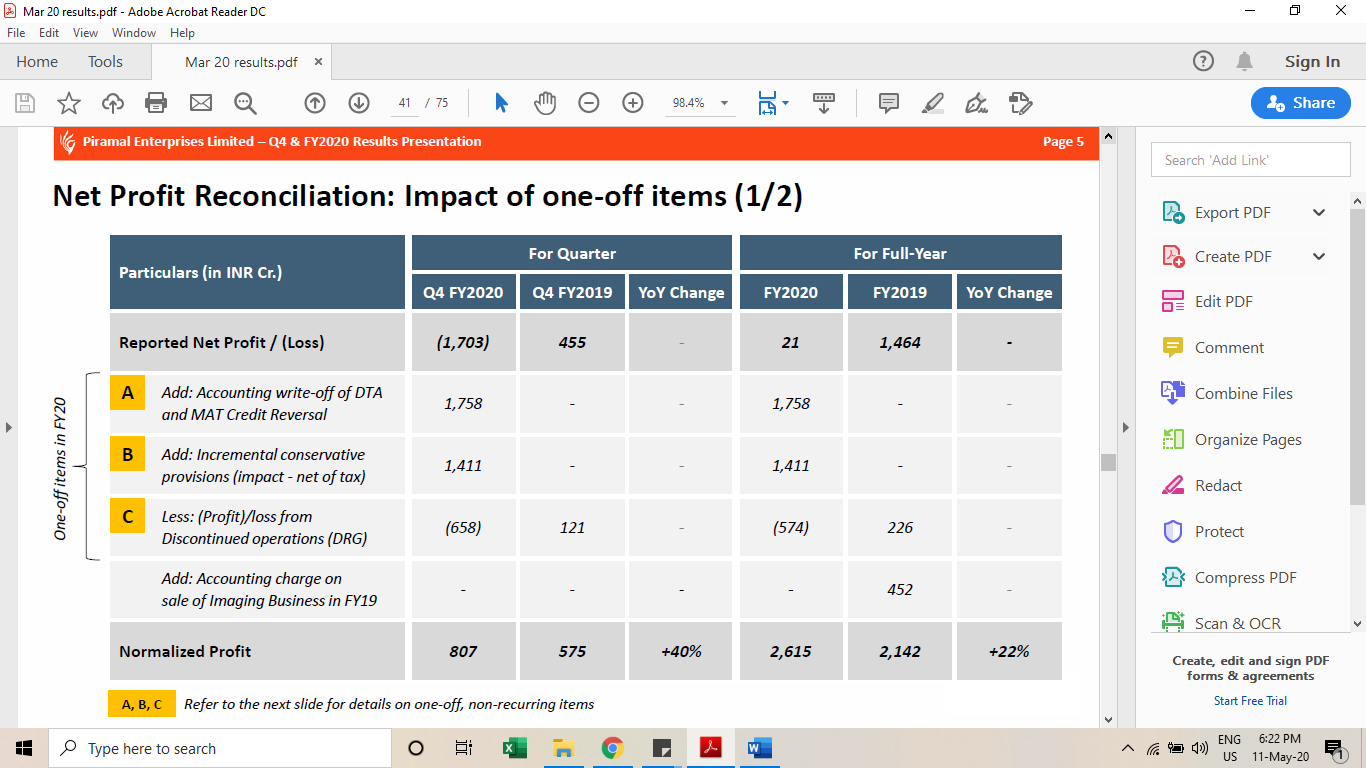

PEL Q4:

Net loss of Rs 1,702.6 Cr vs Rs 454 Cr profit (YoY)

Revenue down 2% at Rs 3,341 Cr vs Rs 3,408 Cr (YoY)

Additional Covid provisions of Rs 1903 Cr.

Pharma:

https://www.bseindia.com/xml-data/corpfiling/AttachLive/1ea1ae21-d114-47c5-8619-3bbea6ee68cd.pdf

2 Likes

Is it good that when you have put a huge sum aside for covid provisioning and asking for moratorium and declare a 14rs as dividend? should be capital preserving the utmost priority right now?

1 Like

Asking for moratorium is not good as it will impact their reputation and should have been a measure of last resort.

As far as the dividend,that is not dividend,that is special dividend after sale of DRG ![]()

1 Like

Huge provision of Rs 1903 Cr is shocking to say the least. That exposes risk management practices of Piramal.

But also hidden in the numbers is one time accounting write off of DTA and MAT credit reversal of Rs. 1758 Cr. See below.

In absence of DTA/MAT reversal, number may not have looked as bad as it seems.

Disclosure - invested substantial portion of my portfolio and hurting badly.:- ![]() …so heavily biased…

…so heavily biased…

5 Likes

Sir,

DRG?

Did not understand.

If you could explain.

1 Like

DRG refers to Decision Resources Group(their healthcare insights and analytics business) that they had sold in Jan 2020 to a US-based company Clarivate for $950 million.

2 Likes

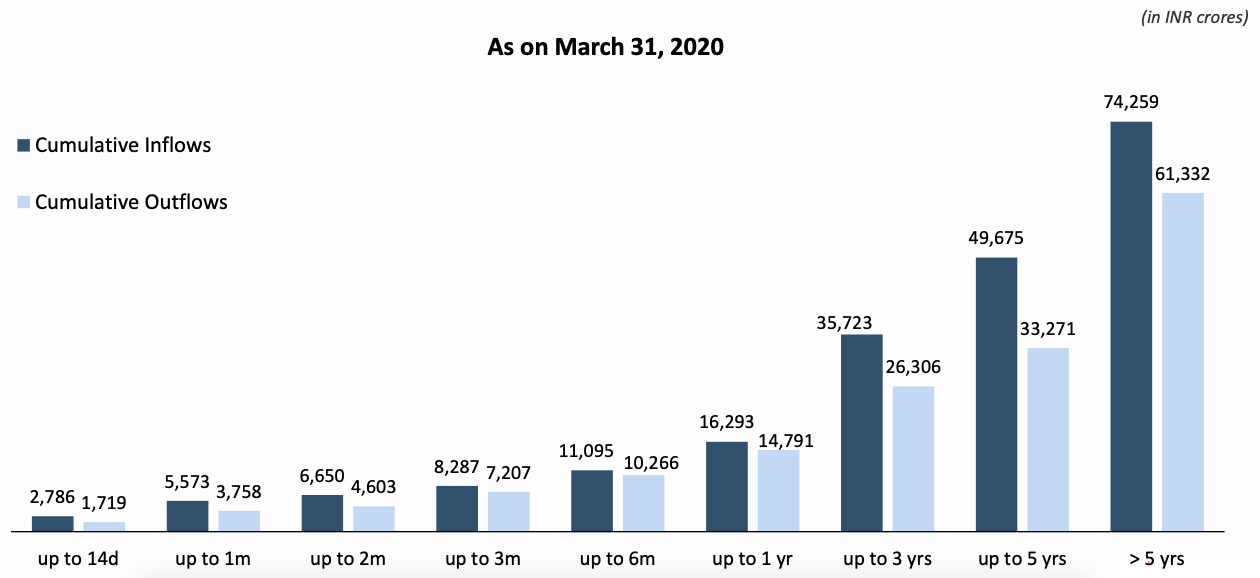

From the concall on moratorium:

They said 20-25% of the retail customers wanted moratorium and on the wholesale side most of the developers have asked for moratorium,total coming to Rs 1500 Crores worth of installments and almost 85-90% of the AUM.

They had guided about bringing Lodha exposure to Rs 2500 Crores from Rs 3000 Cr by end of march quarter,but they could not do it instead have guided to reduce exposure now by Sep 2020,they say they have 2 times security half of which is in the form of ready inventory.

They have exposure to Marvel Realtors,was sole lender to the projects,they did the ‘settlement’ as in they would need to complete the project and they wanted Marvel to bring an investor who brought in equity and PEL agreed to write off 31 Crores out of Rs 208 Crore exposure.

Another problem asset in stage2 is Mytrah group,negotiations are on for selling assets for recovery,they have signed NDA so cannot give any more details,taken provision of 340 crores for 1200+ Cr. exposure.

2 Likes

Mr. Piramal on dividend payout rationale -

- The two large charges taken to P&L - Covid provisioning and DTA are non cash

- In this environment, felt it is important to give some liquidity to our retail shareholders who may not be able to manage as well as promoters/institutions

- Exceptional gain on sale of DRG business and part Shriram stake

- Investors participated in the rights issue recently at higher price

- The dividend is half of last years and only entails an outflow of 316 cr

They did not seem overly concerned with liquidity on the call -

- 9000 cr of cash + credit lines available at March end.

- Post March raised 1,000 cr from banks and expect to raise another 5,000-6,000 cr in the short term.

- Pharma business ~ 125 cr / month in EBITDA

- Pharma minority stake sale ~ 3,500 cr (hypothetical)

- Shriram investment sale ~ 5,500 cr (hypothetical)

Given this position it seems they should be able to navigate even 12 months of zero collections.

-

Wholesale lending (70%) - Almost entire book is under moratorium. They talked about preparing for a stress scenario of 6-9 months of no collections and then a gradual pick up in business. Mr. Piramal repeatedly said there is no point discussing growth and the only focus is on liquidity. They are running down certain assets on the wholesale and retail side by either encouraging them to shift to other lenders or selling the assets. For most of their developers they have spent the last month increasing security cover, forcing them to lower prices, and helping them to complete their under construction projects.

-

Corporate lending (15%) - Planning to bring this book down by at least 50% by exiting the renewables portfolio.

-

Retail lending (11%) - Around 25% of the book is under moratorium and rest are repaying normally (not sure if I heard it correctly). Average ticket size is 70 lakhs which they are working to bring down to 25 lakhs.

-

Hospitality lending (4%) - Worst affected sector with severe impact expected. Exposure is only to best groups like Marriott & Taj which might help

-

Misc - Mr. Piramal was tight lipped about the upcoming retail focused fintech business and did not commit to any timeline for launch other than saying work is going on behind the scenes. Also did not say where capital allocation is going to happen going forward other than saying plenty of opportunities will be available post Covid…

-

On liquidity again, he mentioned in the BQ interview that they have made early repayments on some loans to Franklin Templeton to help them out

4 Likes

Shriram capital enterprise valuation is Rs5500-6000 crs.Mkt cap of SCUF us Rs 5000 crs.He will not get more than Rs2500-2800 cr for the stake there.

The mgt has no bandwidth to run a financial co and the Shriram grp realised it early and decided to call off the deal.

Some where it looks like PEL will sell off the financial division to Ambani who also has a financial divn in RIL…

1 Like

Ajay Piramal On Covid-19 Impact On Piramal Enterprises’ Q4

3 Likes

What is this consumer lending tech platform reporter is talking about ?

PEL is planning to get into Retail funding sector maybe on the lines of Bajaj Finance

PEL is the best example of the poor capital allocation. They are just allocating good money after bad one. Their core competence was in Pharma and they jumped in NBFC and now consumer finance. If they could have focused only in Pharma, hopefully PEL market cap and return for investors might be far better than current one.

Sometime overconfidence in one business success could prompt to do something different and spoil everything!

5 Likes

When company’s core business generating huge free cash flow and promoters don’t redeploy it in core business to grow it better and stronger in-spite of huge opportunity but jumps in unknown territory / out of core competency, in 99% case it is looser’s game!!

Great research from Saurabh Mukherjea on this aspect - read this article -