fyi

2 Likes

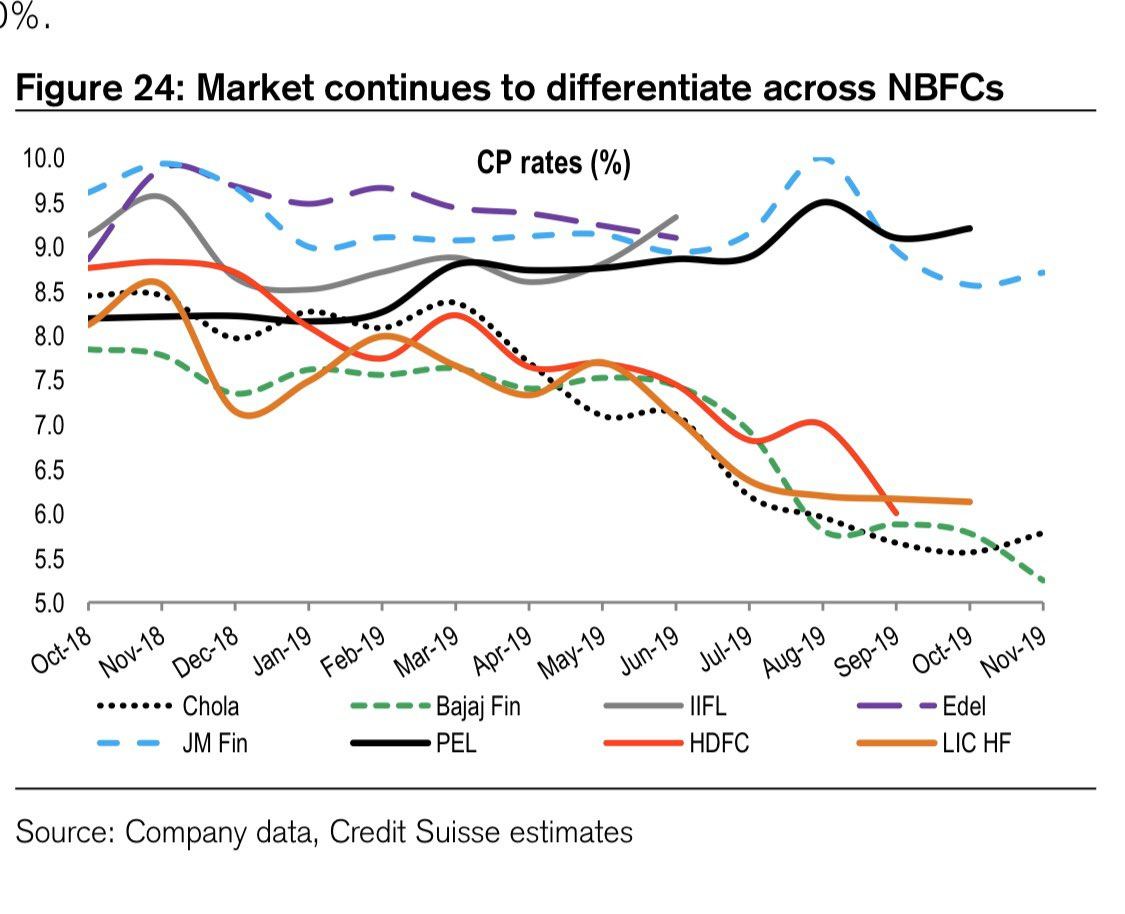

PEL has been reducing its CP exposure. Here an excerpt from the Q2 con call.

“During the past year, we have raised long-term debt of INR 24,000 crores. Bank borrowings now constitute 69% of overall borrowings, significantly higher than the 49% we had in September 2018. Although we did resort to some short-term borrowing during the last few quarters, we have reduced our exposure to CPs from INR 18,000 crores, which was at the end of September, to INR 1,480 crores at end of September 2019. More importantly, CPs from mutual funds have reduced to nearly INR 615 crores compared to INR 15,600 crores a year ago. And by the end of November, we will have no CPs from any mutual funds.”

1 Like

The BANKS/Bond market are themselves not willing to lend and if in any case look at the COST.

As Mr. Ajay Piramal says … Market differentiates between MEN and the BOYS …

Anyways … Investing is about future outlook with eyes firmly grounded on today as well.

1 Like

could you also share the url for the report incase its not propriety ?

PEL will come back. You have to hold your patience. In case you are expecting results in next qtr, you should be disappointed.

They have corrected all the wrong steps. Mkt taught them a lesson.

Hold your patience

In the book Master Class, Mr. Hiren Ved, mentioned, in Financials, you have to trust your Jockey.

Mr. Piramal learnt huge lessons of perils of funding Long term Assets with Short term liabilities.

Hold you nerve…

1 Like

I think it comes from the recent Abbakus report: link is

1 Like

Piramal Enterprises management comments at a recent investor interaction forum:

Capital raise to strengthen balance sheet and reduce cost of funds – Piramal

expects its Rs36.5bn rights issue to conclude by February 2020. The planned capital

raise of Rs54bn (20% Sep ’19 consol. net worth) via this rights issue and issue of

compulsory convertible debentures to CDPQ will increase capital buffer. The

company believes that this, along with a normalization of funding environment and

‘retailisation’ of assets, should help to reduce cost of funds (11% in 1HFY20).

Capital allocation key – Piramal can allocate the capital raised to existing

businesses or use it for inorganic growth. The capital raise will increase outstanding

shares by 20%, so it’s neutral to consol. BVPS, per our estimate. If 50% of the capital

is allocated to financial services, it will increase the segment’s net worth (Rs144bn as

on Sep ’19) by 19%. Promoters have a 46% stake pre-rights issue and have said that

they will fully subscribe to the issue in case of under subscription (Mint). Pro forma,

CDPQ will hold 8-9% stake in the company (details of capital raise in Figures 1-5).

Targeting 50% retail assets – Piramal plans to increase the share of retail to 50%

of loans (vs. 12% currently) and will build an analytics-based consumer financing

portfolio. On the wholesale side, it plans to partner with funds which are looking to

leverage its expertise and commit capital. Piramal believes a more granular asset

book / less client concentration will help in fundraising as well. Gross NPA was stable

QoQ at 0.9% in 2Q. Piramal had resolved 14 of the 18 real estate deals (out of total

242) which needed some corrective action.

Strategic actions – Over the long term, Piramal will monetize investment in DRG

and separate financials and pharma into independent companies. Mr Piramal has

stepped down from chairmanship of Shriram Group and PIRA will exit this over time.

It remains open to inorganic growth in retail (including portfolio buyouts).

3 Likes

Any link to the video or transcript ?

This is a synopsis of comments during a day of meetings, this is also in line with their views suggested in the earnings call.

Piramal Enterprises’ management commentary at Edelweiss Emerging Ideas Conference this month:

PEL, a well-diversified company with interests in financial services, pharmaceuticals and healthcare insights & analytics (HIA) clocked INR 13,215 cr revenue in FY19, with 40% of it generated outside India. Financial services contributed 53% to revenue, pharmaceuticals 36% and balance was contributed by HIA.

Key takeaways:

According to management, business activity in the country has slowed down since the past couple of quarters. This, along with tight liquidity for NBFCs especially for those lending to some specific sectors, has led to slower growth for PEL’s Financial Services business.

For FY20, the company will not chase growth, but will focus on strengthening balance sheet and preserve liquidity to position itself for any favourable opportunities. The company has demonstrated its ability to largely pass on the increase in its borrowing costs

The company has reduced its reliance on short-term borrowings and its CP exposure has reduced to INR 1,483 cr from INR 18,017 cr in the same period last year.

Going forward, PEL is planning to use the co-lending model with public sector banks, global banks or global pension funds for its wholesale lending business. This, it envisages, will boost fee-based income in future, enabling company to maintain its ROE, despite diversification.

Initially, with the fund raise, the company’s leverage shall come down to below 2x. As the company shifts towards retail and grows the loan book in future, management is confident of clocking ~18% RoE in the medium-to-long run.

Management is planning to commence consumer financing in the next 1-2 quarters.

Over 3-5 years, management intends to diversify its loan book with retail housing and consumer finance to be around 50% of the total book.

PEL is currently only a financial investor and not a strategic one in the Shriram Group. It intends to monetise its investments in the next couple of quarters.

In the renewable segment, PEL will remain cautious, especially in Andhra Pradesh. As of now, no major stress has built up for PEL as majority of its loans have been cross-collateralised across assets in multiple states. Renewable constitutes 40-50% of the company’s total corporate exposure (which is 18% of the overall book).

Total exposure to Lodha currently is around INR 3,000 cr and the company is planning to cut it to INR 2,000 cr in the next 6 months. PEL has full escrow control on cash flow of Lodha’s projects towards which loans are outstanding.

Exposure to Omkar Realty is largely through 2 projects (Piramal Mahalaxmi and L&T Crescent Bay) is around INR 2,000 cr. Re-branding both these projects has accelerated sales momentum.

PEL’s focus is to pare individual corporate exposure below 15% of net worth in the ensuing 6 months. Currently, 66% of the portfolio in the developer book is mid to late stage.

The company may demerge pharma and finance divisions in the medium-to-long run.

In the pharma segment, PEL has debt of around INR 3,000-4,000 cr. The company expects to grow this division by 15-16%. It is delivering healthy EBITDA margins in a range of 22-24%.

DRG and India OTC business have shown strong signs of pick-up in their performance.

4 Likes

Never expected that he will sell some bits of Pharma to raise funds ![]()

1 Like

Demerger has been on the cards for years. Remember, Ajay Piramal sold the formulations business to Abbott for US $ 3.72 bn in 2013. So this is really no surprise.

disclosure: holding and planning to apply for rights as well.

wasn’t it always bad to sell good assets to get into more leveraged business? not sure what he will do with the funds raised from selling…will he reenter pharma or put more money in financial services…I think AJ is losing his Midas touch

P.S Highest allocation…not sure what to do

1 Like

IMHO, whether it is good or bad depends on multiple things. What price he will sell this 20%? How is he going to use the money? Earlier he sold part of the company to Abbott at 9 times sales and 30 times EBITDA. I think it will be a huge positive even if he can sell at 4 times sales or 10 times EBITDA. If not, is he going to acquire a good company at mouth-watering valuation? In any case, This exercise can unlock the value of Pharmacy business. There are so many ways this can be a good deal. At the same time, it can be desperation …but, he is raising 5K in a month or so…so, I am hoping it is not desperation…Let’s wait and watch.

2 Likes

The funds will be raised through the issue of a minority stake of up to 20% in the pharma business, which will be “purely growth capital and infused into the pharma subsidiary,” the company said.

Disc: Invested

PEL Management doing Lots of things to improve its Position

Last week launched a AIF in which PEL will transfer some of its existing exposure.

#HoS Raising Cheaper Foreign Debt

Raising Equity From Canadian Pension Fund

Planning Right Issue

Now Diluting 20% in Pharma Business.

Cutting Down exposure with troubled Developers.

Selling Non Core Investment

We may see New Avatar of PEL in next 2-3 Years.

Very Interesting to watch out

1 Like

The right issue ratio is out here.

Fixed rights entitlement ratio as 11 (Eleven) Equity Share for every 83 (Eighty Three) fully paid-up Equity Shares held as on the Record Date by the Eligible Equity Shareholders of the Company and the holders of CCDs who may participate in the Issue.

1 Like

Thanks, and the record date is fixed as December 31,2019.

I have a doubt. If I buy eg 83 shares on 30 Dec and sell all 83 shares on 2nd Jan, am I still eligible to buy 11 shares @1300 as I was a shareholder on record date of 31st Dec?

Technically Yes.

But given that thousands of other trader would be looking to do this as well, the price on Dec 30th would most likely be higher than that on 2nd Jan in proportion to the gains you’re planning to pocket coz of arbitrage.

1 Like