One of the reason for PEL to underperform the market is exposure to real estate financing and the market’s concern about coming out of the crisis.

The obvious question “How much will be losses in the worst case?”

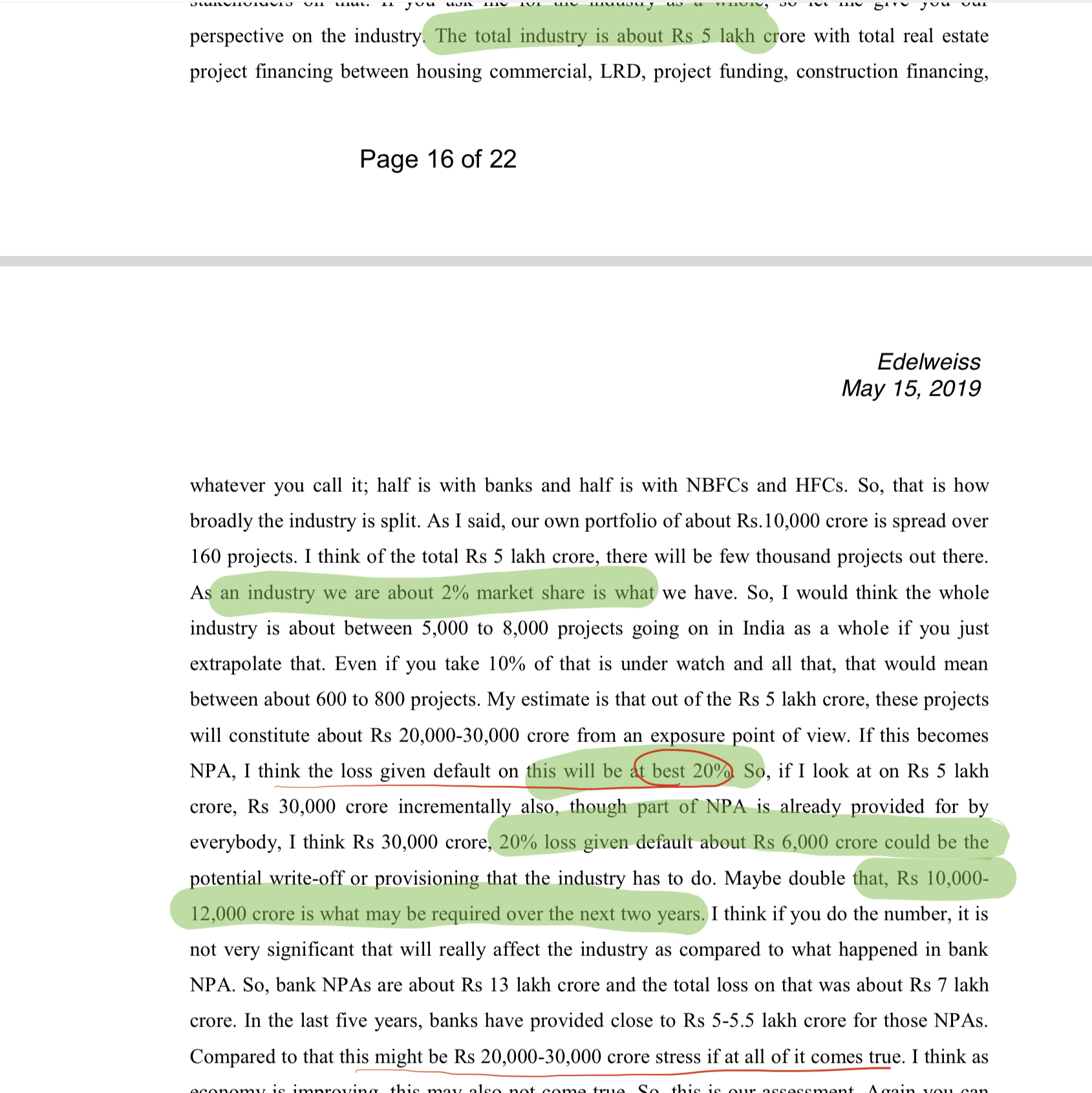

In Q4-FY19 conference call, Mr Rashesh Shah (Edelweiss Finance) gave back of envelope calculation about the real estate financing industry and potential losses that may happen.

I have attached the screenshot here as the same answer is relevant to PEL.

From the figures disclosed (total amount, rights issue price ) so far, one can estimate the ratio to be between 1 rights share for every 10 or 11 shares held in PEL. Market first reacted almost as if it is 1:1 rights issue…

two years ago ratio for rights was 1:23 when Rs 2500 cr . those who applied for extra shares got nearly double of their quota. this time PEL is raising Rs 3500 from rights when the stock price has fallen by nearly half. I expect poor retail interest and those who apply will get very high number of shares. Ratio could be 1:16 or 1:18

Don’t you think it would provide the opportunity tio existing shareholders to average their cost of ownership at lower levels and for the company an opportunity to differentiate its position by maintaining liquidity for good opportunities - liquidity is hard to come by in the current circumstances…

PEL price touched 1300 for a day or two, but Ajay Piramal worked frantically, to secure a deal with CPDQ at that time. Furthermore, he also announced rights issues which entitle existing shareholders a right to buy shares at 1300.

Most of the shareholder has few or few hundred shares, but Ajay Piramal has few lakhs shares. When the market was worrying about the overall health of the economy/real estate sector, he was busy doing what he is best at- making a deal. Even at the current price, he has handsomely earned a return, without investing a single penny so far. Remember, he –other shareholders too- has an option to buy PEL at a later date at a predefined price of Rs 1300.

What a stroke a genius when others were predicting doomsday !!!

Yes, the price is correct. Please check earlier messages where they have announced the price. PEL wants to complete the issue before Feb 2020, so hopefully, they will come up with announcement in Dec/Jan.

So how does promoters generally get cash to deploy in these type of right issues?

where can we see this in accounts which gets debited after the transaction?

Its not that they borrow at 11 % and lend at 9 % for retail housing loan. For Retail housing loan their cost of borrowing is 8.5 % and they lend at 9.3 % Avg. Their construction finance cost of borrowing is 10.5 - 12 % and they lend at 15 - 17 % . Since their construction finance % of loan is higher their avg cost of borrowing is high . Please read last quarter conference call transcript to get more details.

COF for Retail Housing = 8.5% … Average Lending Rate = 9.3% … So spread is 0.8%.

Now add slippages and OPEX and think you would like to be in such business.

Coming to the second part … In valuation its all relative …

Instead of asking me to read the last qtr report though i am updated on qtr reports of all NBFCs i would like you to go and spend time reading peer COF and think WHY IT IS that someone BLENDED COF is less than 9% and why for PirAMAL it is 10%+.

Having said this … Kindly know I am not for or against any business … It is just a perspective and if it makes sense do factor in while tracking the business.

The reason for most of the other companies COF is less is because they are primarily retail focused such as retail HFC’s and companies like Bajaj Fin , Chola , Sundaram etc and the market perceives that there is relatively less risk and hence lower cost of borrowing … However for whole sale NBFC’s such as Edelweiss , Piramal L&T Finance etc the market believes that there is too much risk in the system ( Especially in Real estate ) and hence their cost of funds is higher … BTW for PEL in retail HFC lending they don’t have an NPA and its started recently and over a period of time they have said that the spread will increase … We will get to know whether its right only as times goes by.

A relevant excerpt from the Q2 con call transcript.

“You have to – let me explain. Housing finance, we are 2-year old. At the end of the day, you have to look at housing finance in a 5- to 7-year horizon. And why are we doing housing finance? It’s because there are a lot of advantages. It gives you granularity of the book. As we move towards the 20%, 30% of our book being more granular, the entire cost of funds of the entire book, including wholesale comes down, which more than pays for the low yield of housing finance. So that’s the way you have to look at housing finance.”

Shriram Capital return will be over 100%; they invested at a valuation of 10,000cr and as per media reports are in discussions at a valuation of 25,000cr for their stake. 150% return in 5 years.

PSU Banks lent 3,000cr in Sep alone, see the details in their press release.

Go and check COF for L&T finance or for that matter Aditya Birla Finance and you will have an answer handy.

On the sidenote … Here I am not for or against Piramal as bulk of my own investment lies in NBFCs and hence just making points so as everyone can make a prudent decision.

I am sure Piramal will come back strongly but the points is to demonstrate the situation as-is.

We need to question WHY on our investment all the times …