Timeline for fund raising was announced at the last AGM. AP refused to comment on how the funds will come: selling stake in Sriram group, SoftBank or by some other method. But fund raise by year end was sure, he said.

Very well captured. I was trying to do the same exercised and you have saved my time by thorough research.

One good thing is moving forward, there will be more retail loans by the Piramal and this will further improve the valuations.

Hi Prash

I am not very enthusiastic about their housing finance business.

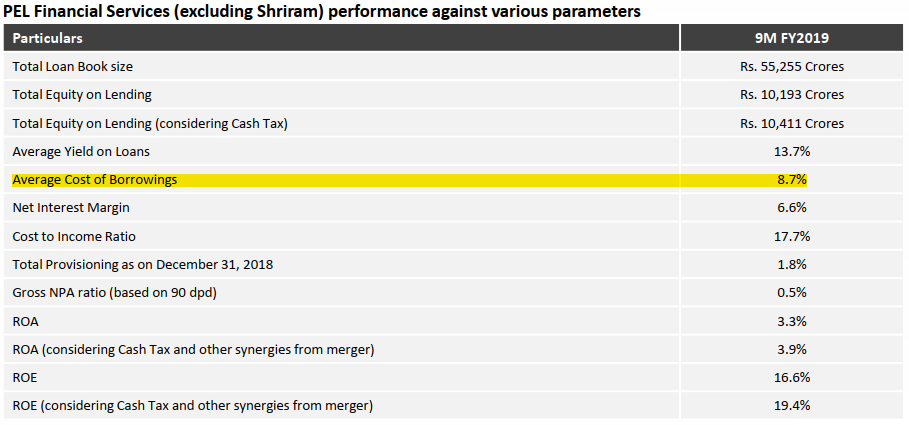

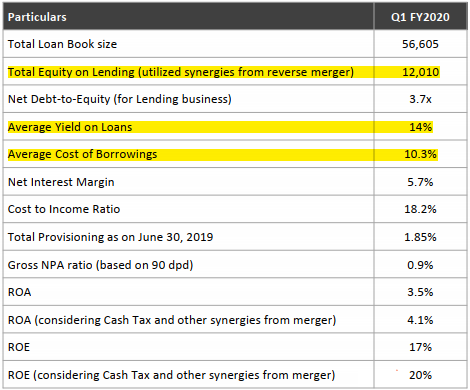

Cost of borrowing has went up from 8.7% in Q3FY19

to 10.3% in Q1FY20.

They are lending to retail customers at 9.4%. Thus every incremental “home loan” is right now being lent at a loss. Unless this trend reverses quickly, Piramal is in shit - question is how deep?

4 Likes

Exactly why the borrowing cost has increased drastically any specific reason, that too at the time when RBI is continuous cutting repo rates.

Nice observation, It is strange Piramal has a Housing Finance licence also, so it’s not pure NBFC company, I think we have to look at it from an Industry perspective and not in isolation. I wonder what would be the borrowing cost for other peers like BajFin, HDFC, LIC Housing Finance. This cost escalation is for new incremental capital anyone else has raised capital recently ? Any idea

Hi amey, thanks for sharing your detailed analysis. Would like to pick your brain on how in q1 roa and roe is higher from q3 despite higher cost of funds, lower nims, higher credit costs, higher cost to income, higher provisions. Doesn’t make sense to me.

1 Like

Though their cost of funds is 10.5 , for the housing segment their borrowing rate is 8 % and lending at 9 % . They are planning to increase the ROE by generating fee income. This is told by Ajay Piramal in the conference call . Please check the transcript.

at the AGM also he spoke of increasing fee income. L&T Finance generates working capital entirely from fee income. piramal too may follow suit.

Some comfort on liquidity position in the market from such news updates.

1 Like

Further news on Lodha groups sales in first week of Oct. It could be part marketing, part truth…![]()

2 Likes

This is a paid advertisement by Lodha, please see the disclaimer.

One needs to triangulate these news bits with quarterly repayments recd. by PEL to understand the liquidity situation. If the trends pf Q2 hold up, any investor in PEL has little to worry about.

Isn’t it curious they chose to call themselves Lodha here and not Macrotech? Small things one must pick up on.

7 Likes

Not trying to negate your view or something maybe just maybe there is light at the end of tunnel

1 Like

Present is not great but the future is bleaker as per this report. Around €10 billion of real estate loans are due for renewal in the first half of FY20.

Another news to suggest green shoots in real estate sector. This is in addition to Lodha and Godrej properties news above

Nice investigation from Business Quint (require subscription, but you can try free for 7 days).

PEL unlisted subsidiary-Piramal Fund Management has given some guarantee to 1000+ cr to a trader based on one shop in Mumbai suburb. BQ tracked down the shop, and it does not have nameplate.

On that guarantee, the trader raised 800-1000 cr from the market from Kotak and other companies.

7 Likes

From the above Bloombergquint article:

“Curiously, the company that plays a starring role in this financing structure and whose debt was supported by none other than an Ajay Piramal company, features nowhere in the balance sheets of Piramal Fund Management and Piramal Enterprises. Neither makes any mention of any undertaking or letter of comfort to Karelides. Ordinarily such an undertaking would show up as a contingent liability.”

2 Likes