I think it will take some time to discover the price for Pharma and financial service considering the complexity of both businesses despite the spin-off. Some investors are selling one or both stocks, which they do not want. Hence the market is creating distortion. This is not new in spin-offs and it does happen often.

The current price reflects what Caryle bought a stake Piramal Pharma, and the price paid was determined before Covid happened (please refer to one of my earlier posts where I posted a video of Ajay Piramal). Essentially it was not hyped price (In early 2020, as was the case in many pharma stocks in 2020/2021). It is all almost 2.5 years, and Carlye has not earned any returns. As it is PE funds, they would expect 15 CAGR to justify their investment and considering separation; they will be much better position to drive value for PPL.

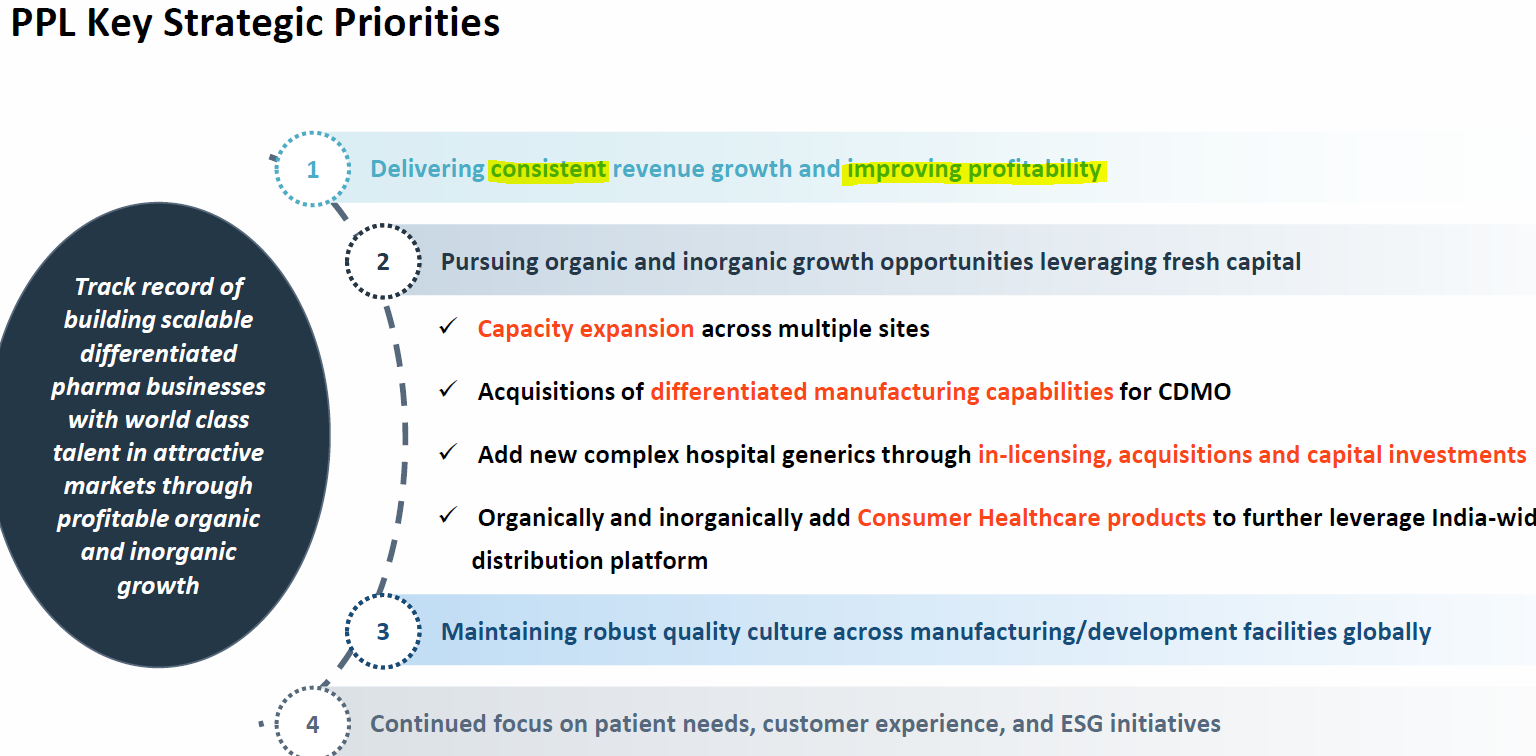

From Q1 PPT,

One thing that stood out was Consistent revenue growth. PEL revenue and profitability were highly erratic and inconsistent (huge intermittent losses). PPL can bring stability and consistency in revenue, profitability and, hopefully, cash flow. If they deliver what they are saying now, PPL will be trading a lot higher than the current price.

Note- Invested and views are biased.