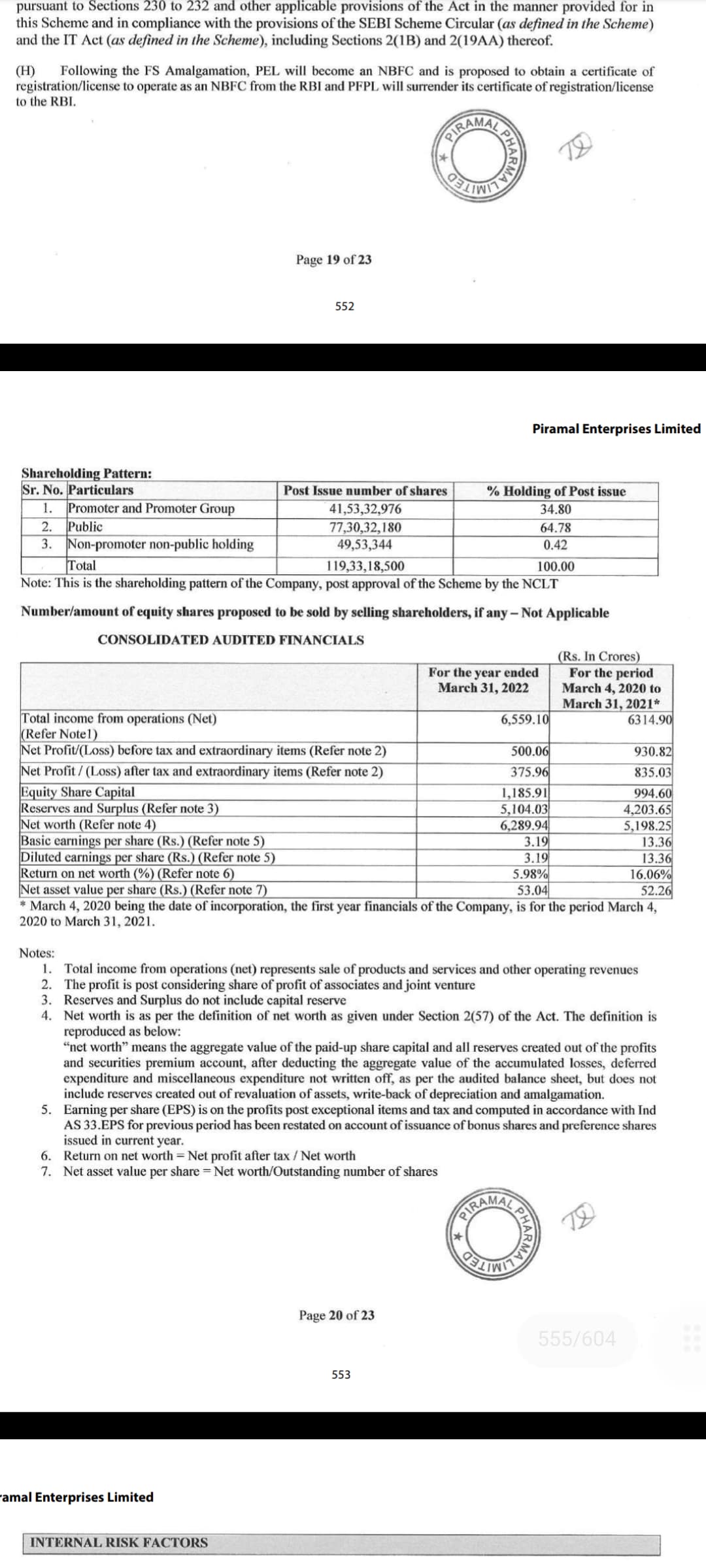

Incase someone is trying to figure out piramal Pharma accounting numbers.

Revenue looks stagnant probably because of DRG business sale at the end of FY21. else, there its a 16% topline growth.

ROE numbers look horrible, partly because of one time acquisition expenses, some new equity raise from Carlyle. Adjusting for this ROE would have been some 10% types.

PPL folks have guided that their EBITDA margins should move back to 22% levels from current 18% in the medium term… factoring that, normalised ROE will be close to 15%.

Also, their depreciation growth in the last 5 years is about 50% and EBITDA margin growth is also close to that- seems like incremental reinvestment is very high to maintain growth in CDMO & Indian OTC brands. PPL folks always talk about EBITDA in their presentations and never about PAT numbers.

Maybe with more phase 3 molecules commercialisation & incremental brownfield expansion utilisations operating and profit margins will shoot up and take the ROE numbers above 20%- I think this should take some time to reflect.

Atleast today as the facts stand, it’s a mid teen topline growth company -growing at the expense of PAT margin and aggresive acquisitions.

Source of PPL financials :