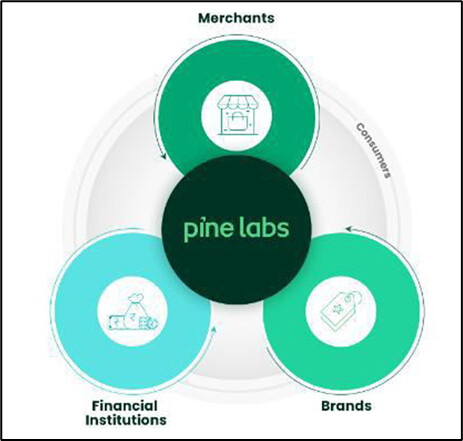

Business Overview

Pine Labs is a merchant commerce and payments infrastructure company built mainly around the checkout point. The company started with in store digital payments and then expanded into affordability, online payments, fintech infrastructure, and gift cards. The clean way to think about Pine Labs is that it first gets control of the merchant checkout through devices and software integration, and then it monetises that checkout through higher value products such as EMI, cashback, value added services, transaction processing, and issuing. This is why Pine Labs is more than a POS company. The POS terminal is the entry point, but the real value sits in the software layer, the merchant relationships, the bank and brand ecosystem, and the ability to push more services through the same merchant base.

Pine Labs is a two engine business, where the payments side is the larger part and the issuing or gift card side is the second large business. Important point to highlight that Pine Labs should be seen as a B2B payments and merchant infrastructure business, not as a consumer facing wallet or app company similar to PayTM or PhonePe. That matters because Pine Labs built its franchise around large enterprise merchants and large banking relationships, which creates stickiness, especially where reconciliation, EMI offers, billing integration, and reliability are important.

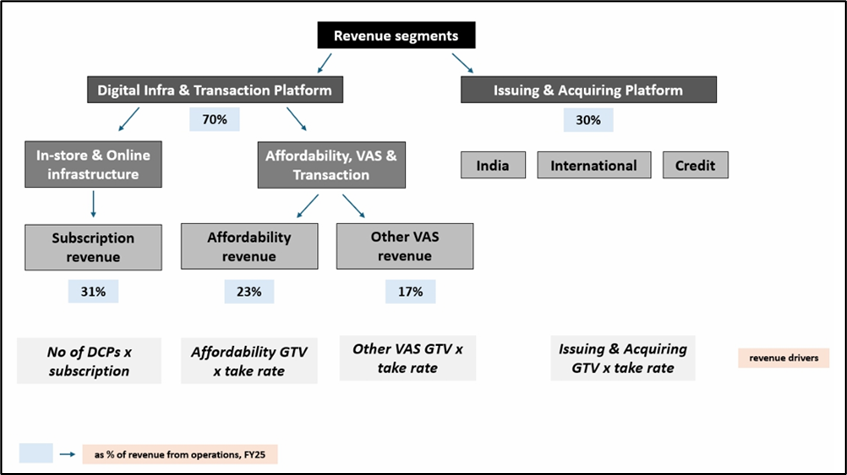

The business today can be understood in 2 segments:

· Digital Infrastructure and Transaction Platform:

This is the larger business and the heart of Pine Labs. In simple terms, this is the payments and merchant commerce platform. It includes in store payments, online payment acceptance, affordability solutions, value added merchant services, transaction processing, and fintech infrastructure.

The most important thing to add is that this segment is not one single revenue stream. It is a layered stack. The lower layer is device deployment and subscription revenue. The middle layer is payment processing and merchant services. The upper layer is affordability, where the company earns better economics because it is solving a more valuable merchant problem.

The expert call discussions add a very useful industry view here. Former insiders repeatedly say Pine Labs’ real edge came from three things. First, its depth of integrations and bank relationships. Second, its EMI and affordability strength. Third, the fact that it built merchant relationships in large accounts first, which are stickier and harder to displace. At the same time, some experts also warn that in the more basic transaction side, Pine Labs does not have as strong a proposition versus players who own payment aggregation, direct merchant acquisition, and UPI better similar to PayTM. So this segment has both strength and limits.

Going into Depth of the this segment’s Sub-segment which contains 3 sub-segments:

1. Payment business

Pine Labs’s payment business is built around POS devices, which enable merchants to accept card and UPI payments in stores. The sub segment becomes stronger if we add that Pine Labs is really an offline first merchant infrastructure platform. The device is the starting point, but the deeper value comes from being connected to the merchant’s billing system, settlement system, financing offers, and service workflows. We can call offline POS the top of the funnel for Pine Labs, and that is a very important observation. The machine is how Pine Labs enters the merchant, but the company makes better money when it can sell more software, more checkout finance, and more services through that merchant.

The online payment gateway business is still smaller than major peers. Pine Labs has built an online and omnichannel layer, but it is still not the primary reason the company is differentiated. The offline merchant base and the EMI led checkout layer remain the more important parts.

Pine Labs’s USP is integration of payment devices into billing software and enabling EMI transactions. This is exactly the right core point and should be given more weight. In large chains and enterprise merchants, payment reconciliation is a real pain point. When the device is integrated into the billing software, the merchant gets cleaner reconciliation, easier settlement tracking, lower manual effort, and better visibility of store level transactions. That is a practical operational edge. The second edge is EMI and affordability. In categories like electronics and high value discretionary products, the ability to turn a purchase into manageable instalments directly at checkout can lift conversion and ticket size. This is why Pine Labs historically built strong brand relationships in this area.

There is one more important nuance from expert calls. Pine Labs historically earned a lot through being a service provider to banks and through multi bank acquiring structures, rather than fully owning merchant acquisition like a pure payment aggregator. This gave it a strong distribution route through banks and large merchants, but it also limited how much of the transaction economics it could capture in some cases. That is one reason why some experts believe Pine Labs has lower net payment margins than players who own more of the acquiring stack.

This business is monetised largely through device subscription fees, along with hardware sales, installation and deinstallation, automation services, annual maintenance, and other related services. That said, UBS makes an important distinction. Subscription revenue is stable and predictable, but growth here is slower and closer to market growth. So this piece is the annuity base, not the main future growth engine.

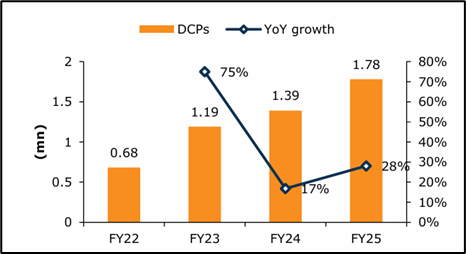

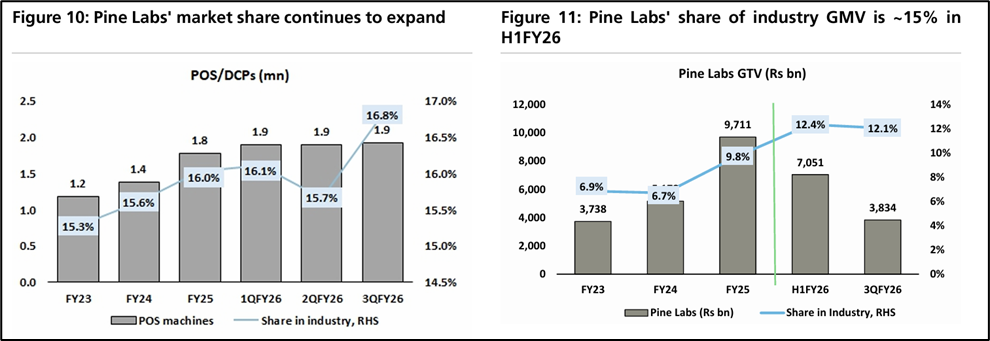

Pine Labs had around 1.8 million digital checkout points in FY25 and remains one of the leading POS providers in India. Its market share in POS devices has stayed roughly stable in the mid teens. UBS adds another useful angle here. The more important metric than just number of devices is the GMV that runs through those devices, because that creates opportunities for cross sell. This is a key insight. In a mature POS market, just adding more terminals is not enough. The real game becomes increasing utilisation per terminal and attaching more services to each merchant relationship.

Pine Labs competes with Paytm, Mswipe, Razorpay, and banks. The competitive intensity needs to be spelt out more clearly. Multiple expert calls say the plain vanilla acquiring business has become far more competitive, with pressure on pricing and weaker differentiation if the merchant only wants basic payment acceptance. Pine Labs is stronger where the merchant needs integration, EMI, dynamic value added services, or a more complex checkout flow. It is weaker where the merchant only cares about low cost transaction acceptance.

There is also an important industry point from the expert interviews. Experts say India is still under penetrated in POS in a practical sense, not because payment acceptance does not exist, but because merchant needs are becoming more complex as ticket sizes increase and use cases diversify. Terminals have evolved from bulky card swipe devices to Android terminals, mobile POS, NFC, QR capable terminals, and multi use checkout devices. So POS growth is not dead, but it is changing. Future growth will depend more on richer form factors, deeper merchant use cases, and software linked monetisation than on simply flooding the market with devices.

Pine Labs Online is online first and omnichannel and helps merchants accept online payments while offering checkout finance and other flows to consumers. This business is still much smaller than large gateway peers and should be presented as an adjacency rather than a core thesis point. It is useful because it helps Pine Labs become omnichannel and defend enterprise merchant relationships, but it is not yet the scale engine of the company. In expert conversations too, the stronger brand association remains around offline checkout and EMI rather than pure online gateway share.

2. Affordability, value added services, and transaction processing

This is the most important section and it deserves the most emphasis. Pine Labs connects consumers, merchants, and brands with credit partners for offline instant cashback and EMI payment options. This is where the company has built one of its strongest moats. Brands typically bear the interest cost through subvention while the financial institution underwrites the consumer risk is the right economic structure. Pine Labs is not taking credit risk in the core EMI model. It is enabling the transaction and monetising the network.

Pine Labs enables merchants and consumer brands to offer instant cashback and flexible instalment options at checkout, including the conversion of a purchase into EMIs. This improves affordability for the consumer and drives conversion and sales for the merchant or brand. This part should be stated very clearly because it explains why Pine Labs matters in merchant economics. The company is not just helping process the payment. It is helping close the sale.

The ecosystem depth is the key moat here. The company has relationships with many financial institution partners and a large base of brands and enterprises. This network matters because an EMI or cashback offer at checkout only works if the brand, the merchant, the bank, and the technology layer all come together in real time. Pine Labs has spent years building this network. Pine Labs has well over 50% the share in offline EMI at POS and strong long standing relationships with OEMs, retailers, and banks. Expert calls also repeatedly describe Pine Labs as the pioneer in offline EMI at the terminal level.

The network of credit partners, brands, and enterprises is crucial should be retained and strengthened. The deeper the network, the harder it is for a new player to replicate the business quickly. This is especially true in categories where EMI is embedded into consumer purchase behaviour, such as mobiles, electronics, and appliances.

But important to highlight that competition is now catching up. Several experts say Pine Labs is still strong, but the market is no longer uncontested. Paytm, being the key player have entered parts of the affordability market. Some NBFCs and specialist lenders are also trying to take share through tactical offers. In other words, Pine Labs still has first mover advantage, but future growth will depend on expanding use cases and maintaining ecosystem strength, not just relying on history.

A major positive insight is that affordability is likely to remain the fastest growing and margin accretive part of the company. Growth not only from consumer electronics but also from non electronics discretionary categories. Pine Labs is trying to extend EMI beyond the traditional stronghold of mobiles and appliances into sectors like fashion, home products, high value services, healthcare, dental, IVF, and selected lifestyle categories. Expert discussions also mention beauty clinics, dental chains, furniture, and high end apparel as emerging use cases. The white space outside electronics is very large.

VAS and transaction processing under this sub segment: These services include dynamic currency conversion, payment aggregation related services, reconciliation, settlement linked tools, and other merchant solutions integrated into payment flows. These services are monetised through transaction linked commissions and can meaningfully lift monetisation per merchant, though take rates in some of these products may compress over time.

For these transactions, Pine Labs earns fees from merchants, brands, enterprises, and financial institutions, mostly linked to GTV processed on the platform. The economics here are better than pure machine rent because the revenue scales with transaction flow and service intensity.

3. Fintech infrastructure

Through Setu, Pine Labs offers API enabled digital public infrastructure solutions across payments, data, and insights. Setu helps financial institutions across onboarding, underwriting, collections, engagement, eKYC, digital contracts, account aggregation, UPI payment collection, bill payments, and recurring payments. This business is more infrastructure led and software driven than the POS and EMI business, and it gives Pine Labs exposure to the wider financial stack beyond merchant checkout.

Structurally, Setu fits well because it expands Pine Labs from merchant checkout into financial workflows and digital public infrastructure rails. But some expert calls are not very positive on how much value Setu has created so far inside Pine Labs. One former executive explicitly suggests that Setu was bought at a high valuation relative to the revenue scale it was doing at the time. Setu gives Pine Labs a useful technology layer across eKYC, account aggregator based insights, UPI rails, collections, and recurring payments. It expands Pine Labs’ capabilities in fintech infrastructure and can help financial institutions manage more of the customer lifecycle digitally. Revenue here is transaction linked and scales with usage rather than with physical deployment. But compared with the core payments and affordability engine, this is still a smaller and less proven earnings contributor. It is interesting, though not yet central to the Pine Labs story.

Hence, Can be understood that within the first segment, the most important earnings driver is no longer just the machine rent. The installed device base creates recurring revenue, but the bigger growth driver is affordability and other transaction linked services layered on that base. We can sees device subscriptions as the annuity core, but affordability as the key growth and margin driver going ahead.

The business also has a clear enterprise skew. Pine Labs is stronger with organised merchants, large format retail, branded stores, and use cases where merchants need more than a basic payment acceptance device. This helps explain why Pine Labs has historically had strong share in offline EMI and value added checkout services, even when pure payment competition increased. On the other hand, multiple expert calls also point out that Pine Labs has not been as strong in the small merchant and pure transaction acquiring side as some newer peers, especially where UPI driven payment aggregation became important. So the company’s positioning is strong in complex merchant use cases, but weaker in plain vanilla acquiring if there is no extra service layer.

The company today should, therefore in this segment can be seen as a mix of 2 things. A device led merchant infrastructure player and , a checkout monetisation player through EMI and value added services

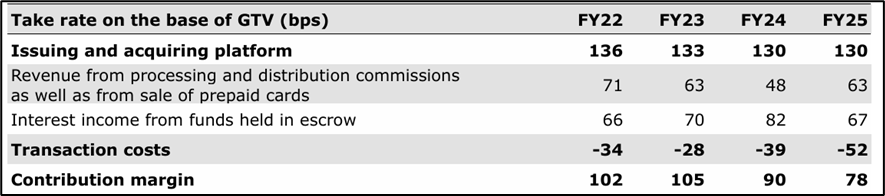

· Issuing and Acquiring Platform: which is the prepaid, gift card, loyalty, and issuance side.

This is the gift card, prepaid, loyalty, issuance, and stored value side of the company. It includes prepaid instruments, gift cards, incentives, rewards, employee benefits, and broader issuing infrastructure for enterprises and financial institutions.

This business is important because it is not dependent on physical device expansion. It is more transaction led and enterprise led. This is an API first issuing stack for prepaid cards, gift cards, debit cards, and credit cards. This segment earns through processing fees, commissions, interest on customer balances, and sometimes breakage. That makes it structurally a better contribution margin business than plain payment acquiring.

A strong point that the acquired gift card and voucher businesses have been meaningful contributors to Pine Labs and in some expert views have been among the more profitable or cash generative parts of the company. At the same time, there are mixed opinions on whether Pine Labs has fully captured the long term value from some of its acquisitions. Some former executives are positive on the economics of the prepaid and voucher business, while others are less positive on newer acquisitions outside the core.

Pine Labs enables issuance, processing, distribution, and management of gift cards and connects the brand with the distributor of the gift card. It becomes stronger if as we go ahead. It covers prepaid products used for rewards, promotions, cashback, refunds, incentives, employee benefits, and in some cases even broader programmatic payout use cases.

Pine Labs’s issuing and acquiring platform enables online and offline merchants, brands, and enterprises to create prepaid products that help drive sales and engagement. This is an enterprise workflow business. It is less about consumer app usage and more about enabling brands and institutions to run a stored value programme efficiently. The company helps create digital and physical prepaid instruments and manages much of the underlying processing and lifecycle stack.

Unlike the device business, it is not dependent on putting more hardware in the field. Growth here depends on programme volume, enterprise relationships, and use case expansion. That means it can scale well without heavy physical infrastructure additions.

The key participants are the brand, prepaid card issuer, distributor, end consumer, and merchant. Pine Labs often plays the issuer and processing role, helping brands create and distribute gift cards through multiple channels. Revenue comes from processing fees, commissions, distribution economics, interest income on escrow balances, and sometimes breakage, depending on the agreement structure.

This business is also one of Pine Labs’s strongest leadership pockets. RBI data showed Pine Labs with dominant share in outstanding prepaid cards and large share in prepaid transaction value and volume. Even where exact numbers may shift over time, the key point remains that Pine Labs is a market leader in prepaid issuance and processing in India.

The expert call adds another important angle. Several expert conversations suggest that Quickcilver and related acquired voucher and gift card businesses have been meaningful contributors and in some views among the more profitable parts of the broader Pine Labs portfolio. One former executive even describes Quickcilver as a cash cow within the system.

Typical gift card issuance and distribution flow:

1. Brands contact the issuer and distributor to issue, manage, and sell gift cards to end consumers. Pine Labs enters here as the technology and operating layer that helps structure the programme and manage issuance.

2. PPI issuers issue gift cards and are responsible for lifecycle management and compliance. This is an important role because the issuing entity needs to handle the regulatory and operational side, not just the customer facing sale.

3. Distributors make these gift cards available to end consumers through multiple channels such as online marketplaces, corporate channels, merchant channels, and other sales routes. Pine Labs’s scale and enterprise relationships help widen this distribution.

4. End consumers buy the gift cards through these channels. In many cases, the use case goes beyond gifting and extends into refunds, rewards, or promotional value.

5. Distributors keep their commission and pass the rest of the value to the issuer. This is where part of the commercial economics of the model sits.

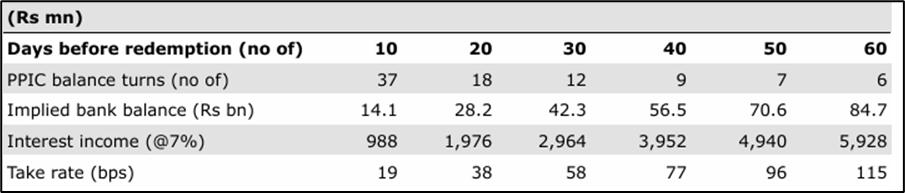

6. The issuer deposits funds in the escrow account and earns interest on these balances until redemption. This is one of the reasons this business can have attractive economics versus plain payment acquiring.

7. When the end consumer redeems the card at the brand’s store or website or app, the issuer debits the escrow and passes value to the brand. This closes the loop between stored value and merchant consumption.

8. In some cases, if the gift card is not fully redeemed before expiry, the unredeemed value or breakage is either returned to the brand or retained by the issuer based on the commercial agreement. This can also support business economics.

The right insight to add here is that this business benefits from scale in a different way from the POS business. In POS, scale comes from merchant installations and payment flows. In gift cards and prepaid, scale comes from enterprise programmes, distribution breadth, processing efficiency, and float economics. That makes the issuing platform an attractive second engine for Pine Labs.

Industry Overview:

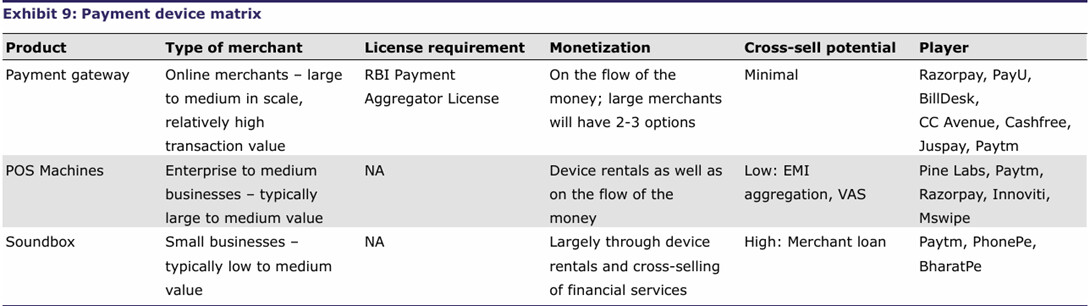

Digital payment channels can be divided into three buckets:

1. Payment aggregators and gateways, which power payment acceptance on apps and websites across UPI, cards, wallets, net banking, BNPL, and other methods.

2. POS devices, which are primarily used for in store card acceptance, higher ticket checkout, and affordability led transactions such as EMI.

3. QR codes and soundboxes, which are used heavily for UPI led merchant acceptance, especially among small merchants and long tail retail.

To expand the addressable market, most successful players in one product category try to move into adjacent categories. That strategy makes sense on paper because all these products sit within merchant acceptance. But in practice, success in one product does not automatically translate into success in another. Online gateways depend on technology reliability, API integration, and merchant onboarding. POS depends on device deployment, bank tie ups, service quality, enterprise relationships, and in some cases EMI integration. QR and soundbox depend heavily on distribution, sales force scale, last mile servicing, and cross sell capability. This is why the Indian merchant payments ecosystem has remained diversified even as large players try to become full stack.

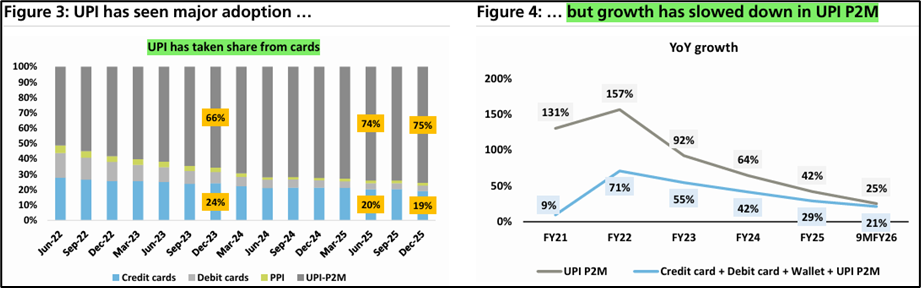

One important insights is that the broader digital payments market in India is still growing well, but the composition of growth is changing. UPI has already seen massive adoption and now forms the dominant part of digital payments. As a result, headline digital payment growth is still healthy, but the hyper growth phase driven by first time UPI adoption is moderating. At the same time, card acceptance infrastructure continues to expand, but the pace is becoming more measured. This means the next phase of the industry is not just about putting more acceptance points in the market. It is increasingly about better monetisation of each merchant, higher utilisation, software layers, credit linked use cases, and cross selling adjacent services. That is a very important lens to keep in mind while analysing Pine Labs and its peers.

Different products within merchant acquiring serve very different merchant cohorts. Large enterprise merchants usually value reconciliation, stability, multiple bank relationships, card acceptance, EMI availability, and store level integration. Mid market merchants care about cost, ease of onboarding, and operational simplicity. Very small merchants often care most about zero friction UPI acceptance and low monthly cost. So the market is not only divided by product, but also by merchant segment. This helps explain why some players are stronger in enterprise POS, others in online payment aggregation, and others in QR and soundbox.

Online payment aggregator and gateway

On the merchant side, acquiring banks ensure settlement of online payments into merchant accounts, but the job of onboarding and servicing a very large number of merchants at scale is done by payment aggregators. Aggregators remove the operational burden on banks of doing KYC, onboarding, compliance, monitoring, and day to day merchant management for every merchant individually. Payment gateways then provide the technology rails that securely transmit transaction data between the customer, merchant, issuing bank, acquiring bank, card networks, and other payment participants. In practice, both the aggregator and gateway roles are usually bundled by the same provider, which is why market participants often refer to them together.

Online payment aggregators and gateways support a wide mix of payment methods including UPI, cards, net banking, wallets, BNPL, and in some cases loyalty linked or embedded finance flows. This business is regulated by the RBI and providers need a Payment Aggregator licence to operate. The licensing process requires a fit and proper assessment of promoters, adequate net worth, secure technology systems, compliance controls, data protection, and standards such as PCI DSS. This regulation has raised the entry barrier somewhat, but the industry remains highly competitive because several scaled players already have strong merchant networks and technology infrastructure.

The business model is primarily MDR or payment processing fee based. Providers charge merchants a percentage of transaction value and sometimes a fixed fee per transaction. Pricing varies materially by merchant size, category, and throughput. Large online platforms such as ecommerce, quick commerce, travel, food delivery, gaming, ticketing, and other scaled digital merchants generally integrate with multiple payment aggregators at the same time. Their routing engines dynamically allocate transactions across providers based on transaction success rates, cost, downtime, bank performance, and payment mode level efficiency. This multi gateway routing system limits pricing power because large merchants are in a position to negotiate hard and switch traffic if economics worsen or performance drops. As a result, take rates for large online merchants usually stay in low to mid single digit basis points. Smaller merchants can see higher take rates, but they also come with lower throughput and higher support costs, which means the operating expense to revenue ratio is less attractive.

Another important structural point is that this business does not enjoy meaningful moat from hardware or physical deployment. The moat, where it exists, comes from reliability, integration depth, merchant workflows, success rates, and ecosystem breadth. Also, once a merchant scales, it is very common to add multiple gateways, which means even a successful integration may not be exclusive. This keeps the market structurally competitive and means long term winners are those who can combine scale, tech quality, merchant trust, and efficient servicing.

Source: Redseer And Pine Labs DRHP

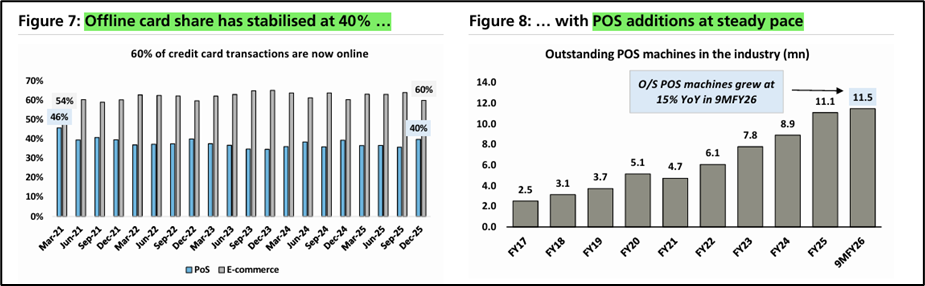

A growing share of card transactions is moving online, which means the offline card share has stabilised rather than expanding endlessly. Also, while the number of POS machines in the industry is still growing, the pace of new additions has moderated from the earlier surge. This suggests that the next stage of offline payments will not just be driven by more devices but by better usage per device, more attached services, and new monetisation models such as affordability, software led services, and credit enablement. That matters directly for Pine Labs because the company’s model is strongest when it can monetise the installed merchant base beyond simple machine rentals.

One expert argues that India is still nowhere close to saturation in POS form factor penetration because merchant needs keep changing as ticket sizes rise and digital acceptance gets more sophisticated. Earlier the terminal was bulky and basic. Over time, the market moved to GPRS terminals, Android terminals, mobile POS, NFC capable devices, QR capable machines, and hybrid payment devices. So while simple card acceptance may mature in some pockets, the broader category of digital checkout hardware and software still has room to evolve. In other words, the offline market is expanding not only by number of merchants but also by richness of merchant use cases.

POS devices

POS devices have been prevalent in offline environments for a long time as the standard way to accept credit and debit card payments. They read the customer’s card, communicate with the banking system to authorise the transaction, and facilitate settlement into the merchant’s account. In today’s context, though, POS devices are no longer only card readers. They have evolved into checkout devices that can support cards, UPI, gift cards, vouchers, EMI, tap and pay, and in some cases limited software applications around invoicing or value added merchant functions.

POS machines cater mainly to higher ticket environments and to merchants where customers want payment choice beyond UPI. These use cases include earning card rewards, redeeming vouchers, accessing brand or bank EMI offers, paying through debit or credit cards, and handling more formal checkout needs. Merchants in electronics, mobiles, appliances, organised retail, fashion, healthcare, travel desks, hotels, and other larger format outlets still rely heavily on such devices. Even where UPI is available, the card and EMI use case keeps POS relevant.

A POS machine typically supports UPI, credit cards, debit cards, gift cards, vouchers, and EMI at checkout. Although many providers market additional features such as inventory support, payroll tools, GST related features, or loyalty tools, channel feedback suggests that most merchants still primarily value POS for payment acceptance and EMI enablement rather than for these ancillary software functions. This is an important industry reality. Merchants may appreciate add ons, but the core purchase driver remains reliable payment acceptance and transaction linked value.

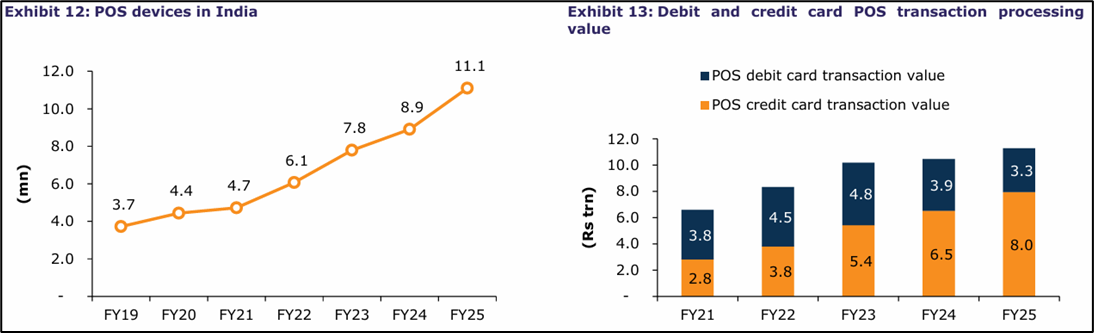

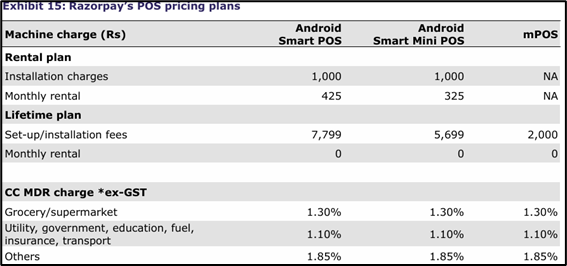

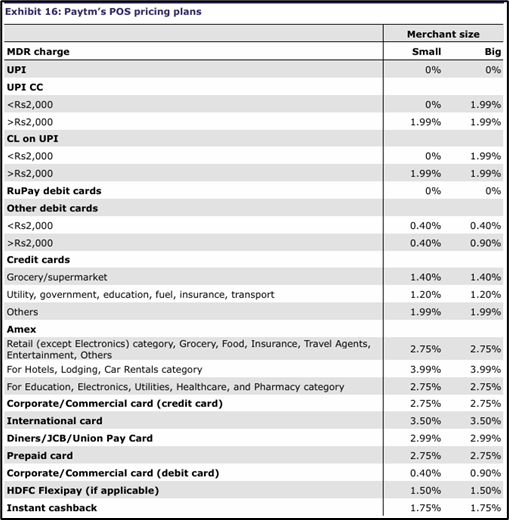

India has seen a rapid increase in the number of POS devices over the last few years, driven by digital payment adoption, government support, merchant formalisation, and better economics of device deployment. The installed base has expanded meaningfully, though growth is now becoming more normalised. Pine Labs, Paytm, Razorpay, Mswipe, Innoviti, PhonePe, Verifone, and banks are the main categories of players. Many banks offer POS devices directly or through outsourced partners. Pine Labs remains one of the largest POS players in India, with a very meaningful installed base and a strong share in enterprise and organised retail. Paytm is the second large player, and Razorpay built presence partly through acquisition. Banks also remain important in this ecosystem because in many cases they own the merchant relationship while technology providers or POS vendors power the device and service layer.

There is little hard hardware differentiation among POS providers. Multiple players use standard terminal makers such as PAX, Ingenico, and others. Typical Android based POS devices can cost anywhere from around Rs 5,000 to Rs 11,000 depending on features and configuration. This means the real differentiation is not the hardware itself but the software layer, the commercial structure, servicing, bank integrations, and merchant economics. Merchants usually judge products based on transaction success rates, pricing plans, device rentals, MDR, ease of use, and after sales support. In higher value environments, EMI capability and reconciliation also matter a lot.

The revenue model for POS devices generally combines subscription fees for hardware and software with MDR or transaction linked earnings. A high end Android POS with a printer can command monthly rentals of around Rs 400 to Rs 600, while smaller Android devices without a printer see lower rentals. Some providers also offer lifetime plans where the merchant pays an upfront one time amount and then no monthly rental. This pricing flexibility helps address different merchant segments. But one important insight from UBS is that subscription revenue alone is unlikely to be the main long term growth engine. As POS growth becomes more aligned with industry growth, the better businesses will be those that can monetise the installed base through additional services.

Form factor innovation is also reshaping this category. Large organised merchants may still use full Android smart POS devices with printing capability and broader acceptance features. Smaller merchants may use cheaper smartphone linked card devices or simpler Android form factors without printers. As credit card penetration widens and merchant needs evolve, lower cost card acceptance products are becoming more relevant. These devices are cheaper and help bring card acceptance into lower frequency use cases where a full smart POS may not be economical. However, they often involve more manual set up and are less seamless than an all in one terminal.

One former business head says Pine Labs was smart in the early years to focus on large merchants because those relationships are sticky and create a strong base. Another former executive, though, points out that this strength in large merchants also became a limitation because the enterprise segment matured while the mid market and SMB segments grew faster. That means the POS market is not uniform. Pine Labs has historically been strongest where merchant complexity is high and bank or enterprise relationships matter. It has been less dominant where high velocity merchant acquisition and broad based field sales are the main success driver. This helps explain both the company’s strength and its limits.

Plain vanilla transaction acceptance in POS is becoming tougher. Without EMI, deeper merchant integration, or differentiated services, the POS business alone can become commoditised. This means the best positioned players are not those with only devices, but those with either stronger ecosystem economics or stronger attached services.

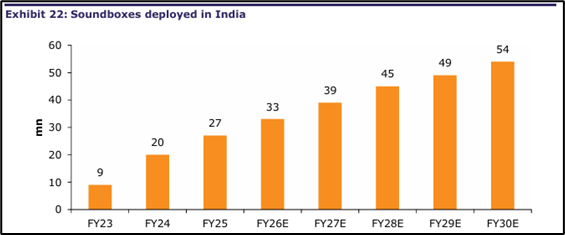

Soundbox

The proliferation of UPI has been the biggest driver of India’s digital payment revolution, but it also created an operational issue for merchants, especially at the small merchant end. Payment verification through SMS, app notifications, or manual screen checks created friction at the point of sale and increased the risk of error or fraud. The soundbox emerged as a simple but very important hardware innovation to solve this problem. By announcing payment confirmation instantly in audio form, it gives the merchant trust, speed, and operational ease without needing to constantly inspect a phone screen.

Paytm was the pioneer in popularising the soundbox at scale, and the product quickly became one of the most visible hardware categories in India’s small merchant payments ecosystem. The device combines instant payment confirmation with ease of deployment and relatively low cost. It is especially well suited to kirana stores, roadside merchants, micro retailers, pharmacies, small restaurants, and other long tail merchants where transaction ticket sizes are low, merchant sophistication varies, and fast throughput matters. Soundboxes effectively monetise the zero MDR UPI model through a subscription fee, while also creating a merchant data trail that can later support cross selling.

Adoption has been very strong and there is still a long runway, particularly outside the top metros. Penetration is already meaningful in larger cities, but tier two and tier three markets remain under penetrated. This is why the soundbox market is still seen as attractive despite rising competition. Paytm and PhonePe are currently the leading players, largely because success here depends heavily on distribution. A large feet on street team, efficient logistics, installation support, device servicing, and local market presence are all critical. This is a very different business from online gateway or enterprise POS. It is field execution heavy.

Currently, soundbox providers typically charge around Rs 100 per month, though pricing is often subsidised or discounted to gain market share and build the merchant base. But the long term strategic attraction of the soundbox is not only the rental fee. It is the ability to cross sell high margin financial services such as working capital loans, based on transaction data, merchant behaviour, and payment history. Some players have also experimented with advertising on soundboxes, though there is little evidence yet that this has become a material revenue line.

The emerging role of RuPay credit card on UPI and credit line on UPI. This can materially alter the economics of QR and soundbox based acceptance. When a merchant accepts a transaction funded by RuPay credit card or by a sanctioned credit line on UPI, MDR starts entering a category that was earlier dominated by zero MDR payments. In such transactions, the QR provider or soundbox provider can participate in payment economics alongside the issuing bank and other stakeholders. Over time, this can make QR and soundbox acceptance more similar to card acceptance in economic potential, though with much lower hardware and distribution cost. This is why these products can eventually replicate some features of card and EMI based checkout using a much cheaper acceptance architecture.

If QR and soundbox based systems increasingly support credit linked use cases, tap and pay, and richer consumer payment options, then some of the functionality that historically belonged only to POS devices can migrate to a lower cost acceptance layer. This does not mean POS becomes irrelevant, because high ticket in store card use cases, enterprise integrations, and more complex checkout will still need stronger devices. But it does mean that the lower end of the merchant acceptance market may increasingly get served through QR and soundbox rather than full POS terminals.