Still no updates on expansion that was suppose to complete H1.

4 Likes

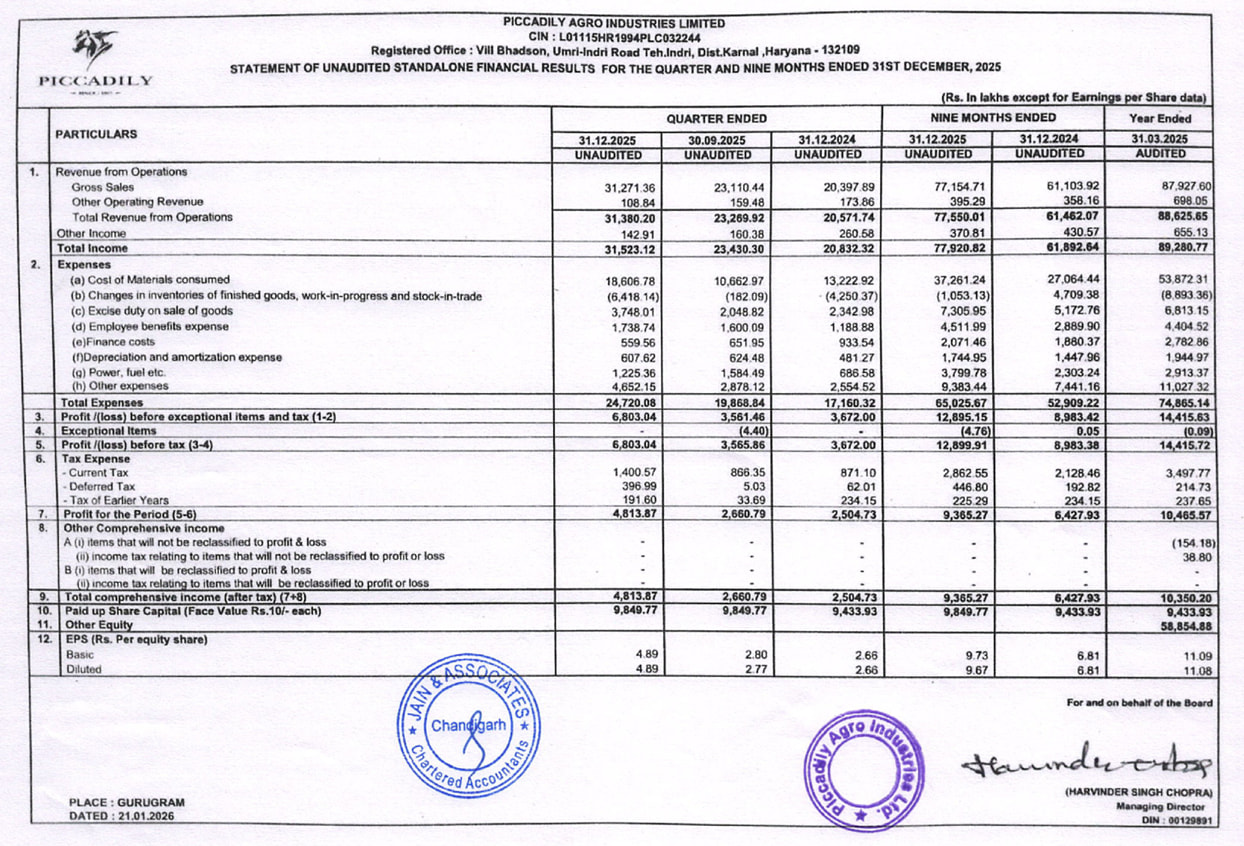

What do seniors make of modest growth of 11%?

Small scuttlebutt; recently went to a few nearby liqour store (in Nagpur) and they mentioned supply is still an issue with demand also reducing with it. Camikara and Whistler which were launched a while ago are still not available in majority of stores. Same couldn’t be said about products from Radico.

Disc- Have been invested heavily in this counter from lower levels

Excise approval is pending according to the investor presentation.

1 Like

the growth is ~ 40% qoq largely on account of the distillery performance. The distillery EBITDA margins have improved from 26.9 to 30.2%. Guess these are the only 2 positives in the performance.

As er the latest presentation

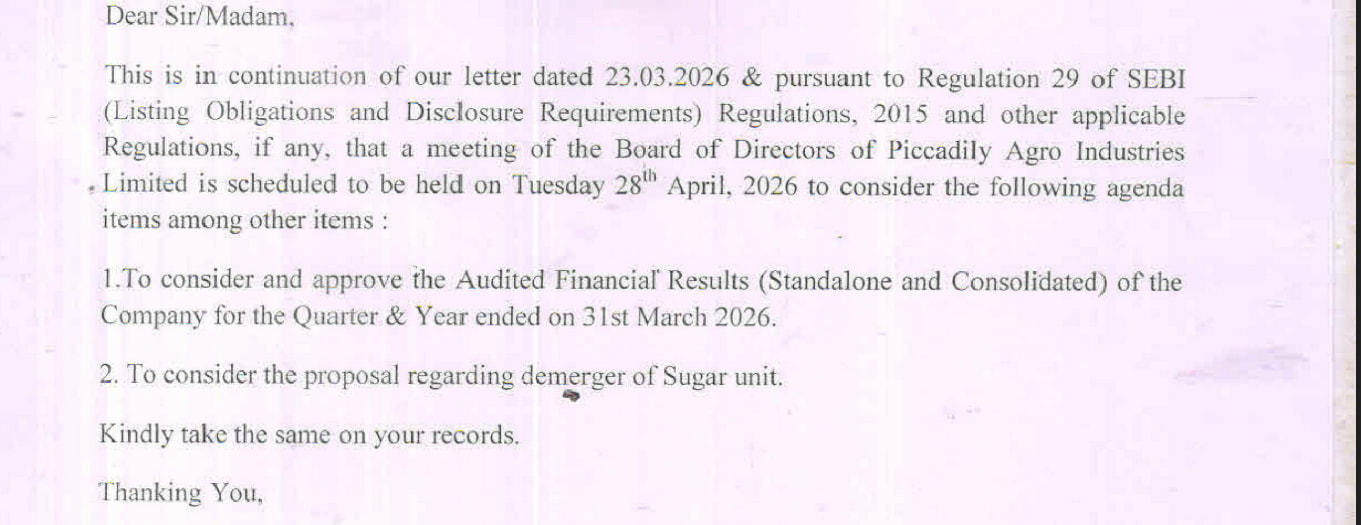

the company is exploring options for its sugar

business along with possible organic and inorganic opportunities in the alco-bev and or ready to drink (RTD) production and distribution space in

India and overseas

The sugar business is very low margin business.. I don’t know why they want go ahead with sugar business when there is huge opportunity lies in the distillery business..

@dinesh111a That sentence taken as a whole probably means they are considering options to sell or demerge the sugar business and looking for acquisition in the distillery section . Atleast thats what it looks like to me .

@DrHarshilRohit .. They clearly have limitations on increasing production right away on account of the time to mature the products even if they have extra barrels and capacity . So more time will be needed to see jump in sales . On the other hand, I have heard good reviews about Cashmir and Agneya …so things are not bleak but needs patience . I am also wishing that I had sold my holdings when it reached 1000 …then I could have increased the holding size a lot . But alas ..hindsight is of no use ,so I will hold and see when revenue grows again . Incase you have a heavy allocation, maybe it makes sense to reduce some if you see better options of quicker returns .

7 Likes

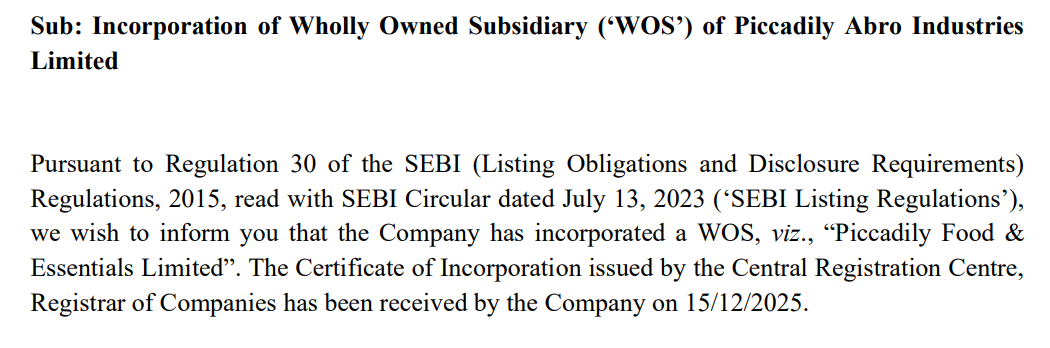

Piccadily agro incorporated a wholly owned subsidiary in the food sector as mentioned in the exchange filing.

1 Like

This could possibly be launch into coffee market. All big liquor manufacturers have their own variants of barrel aged coffee or coffee cocktails. Radico’s 1965 Spirit of Victory espresso coffee rum launched recently has good traction in metro cities.

Was wondering when Piccadily will start its own.

Maybe I am wrong here, but I think they might transfer Sugar Business to this subsidiary to initiate with their Divestment/Demerger Plan.

In last presentation they mentioned they want to enter into" ready to drink market{ manufacturing and distribution}". wos may be that purpose only?

commenced commercial production at its chhattisgarh unit having capacity 200klpd with effect from 31st december,2025.

1 Like

Q3 - Share of IMFL of Revenue from operations was at 56.1% vs 58.4% in Q3 FY25 (176cr vs 120 cr). IMFL (Indri, Camikara, Whistler and Cashmir) sales volumes grew 70% in Q3

9m Fy 26 - Share of IMFL of Revenue from operations was at 44.6% vs 48.1% in 9 mths FY26 IML Rev 9m – 346 cr vs 295cr (17.28% YoY)

1 Like

4 Likes

Latest Award Winner. Idk why they haven’t made an announcement for it. They got 2 gold in world whiskies award 2026.

I thinl Piccadily is a good bet considering the new capacities which will contribute initially with ethanol/ena segment and later with distilleries revenue.

5 Likes

On track to do 500 Crs of Revenue in FY26. At 35 - 40% EBITDA margins - this is now anywhere between 175 - 200 Crs of EBITDA. The alco-bev business alone should be at 6k Cr valuation (30x multiple vs nearly ~40x for Radico)

This excludes the ongoing spirit capacity expansion and the room available within existing malt capacities to grow

3 Likes

4 Likes

Can you help me with the maths behind this?

Is market already price in this merger?