I was looking through the financials of PI and notice that there is barely any cash flow generation in the core business, pretty much any operating cash flow is consumed in capex and finance costs, which seems a continuous and recurring feature essential to growth with no sign of operating leverage, cash flow or capacity wise.

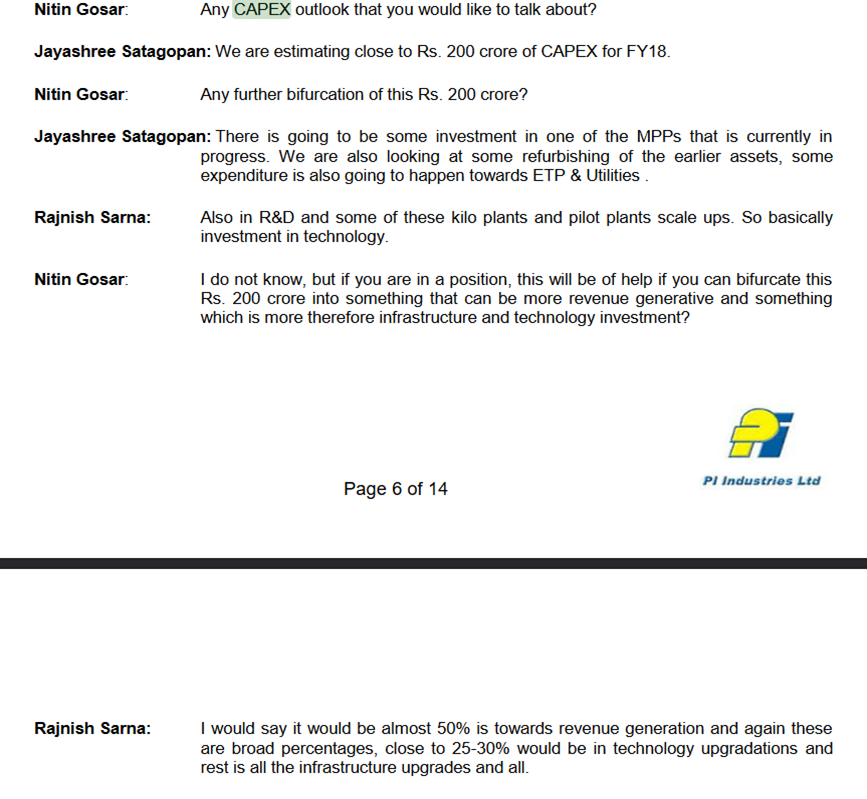

Going through investor calls from the past, the company doesn’t have a v consistent answer as to why its capex cycle always scales proportionately to growth, or when it would scale to the point of generating true free cash flow. They also never give any clear guidance on how they plan for capex, beyond growing the guidance each year. The stated reason for this is they have multi product plants with different products for different clients, and as such the capacity utilization across the product mix is not strictly comparable, and that plants can be single product or multi product as required. There are also various other reasons for capex that come up, such as for backward integration, technology upgradation, debottlenecking etc. While this may make sense, its also conveniently vague on how capex outlays are laid out.

1

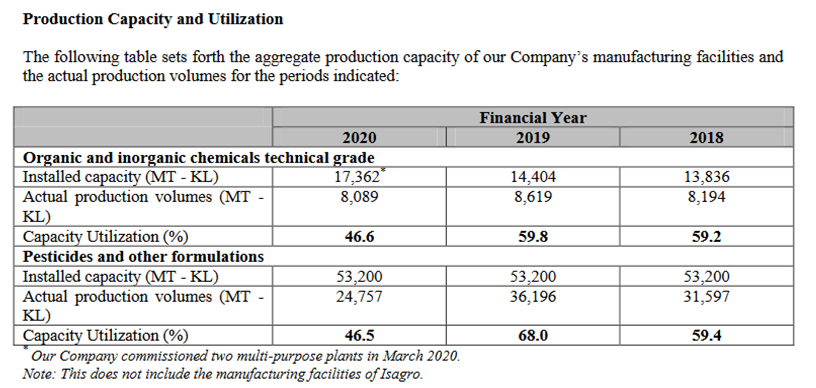

They make the same case for utilization, that product mix makes having a common standard for utilization difficult, yet guide in FY19 that many assets are at 90%+ capacity utilization, while the recent QIP document states otherwise

2

3

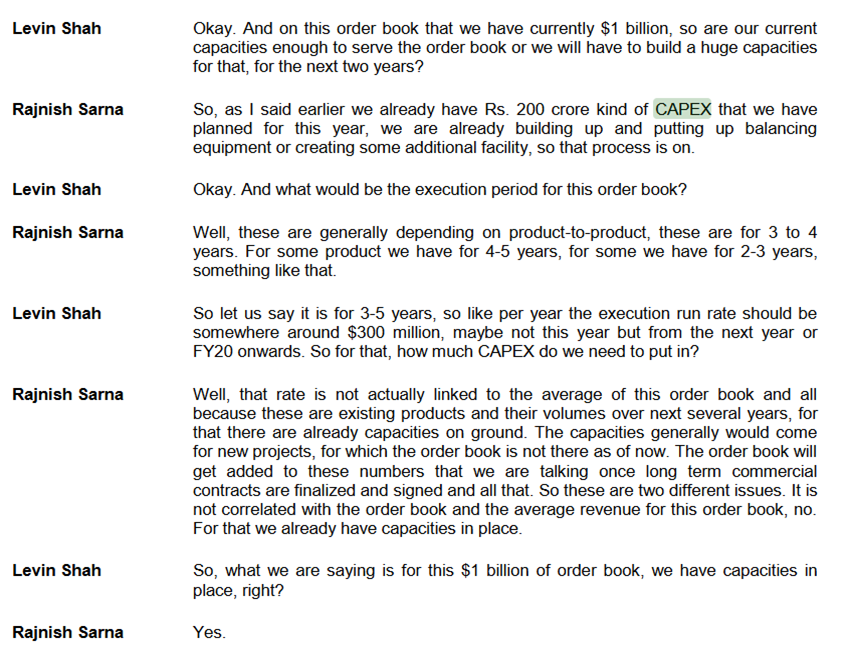

At different points, they guide that capex is planned as per the existing order book, and at another that capex is planned over and above the order book (for which capacity always exists), to account for future order flow and / or one off opportunities.

4

5

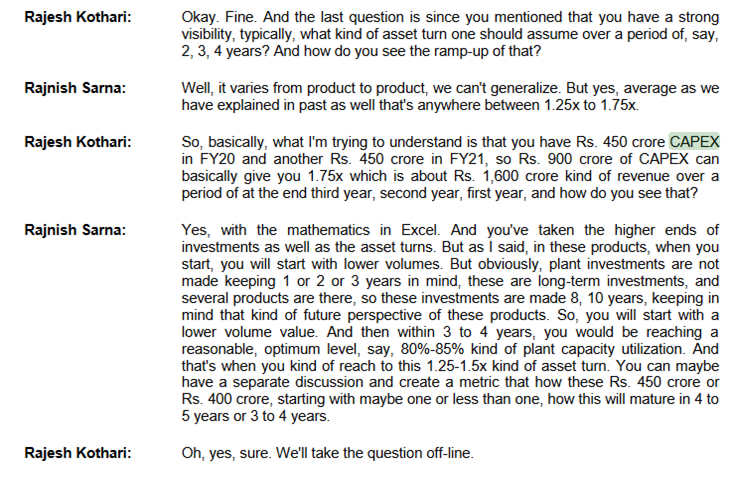

On the plant asset itself, they guide a plant may have 8-10 years of life, and a peak turns of 1.5x times investment (they clarify this is not total capex, but only the actual plant assets) building up over a 4-5 year period from commissioning. There also seems to be significant upgradation and maintenance capex, besides for debottlenecking the existing plants and for ancillary parts to these plants, so together this doesn’t look terribly efficient.

6

7

My interpretation after this is that the multi product nature of the business would make the plants rather difficult and complicated to run, which limits meaningful ability to create operating leverage through scale and specialisation. They also seem to have a product pipeline that keeps growing by 4-5 molecules a year, and at least some of these keep requiring new facilities, while the others add to the operating complexity of existing plants, requiring upgradations, debottlenecking and more tech. Besides this, they also set up one off capacities in niche molecules not based off the order book for more experimental growth. This all adds up to v large cash consumption that scales with business growth and I imagine gets more complex as the base grows. To add to this, they are now entering M&A actively and also investing into the plants they’re acquiring. The silver lining is that management has raised 2000 cr of equity via QIP rather than leverage excessively, and they are looking for pharma acquisitions which hopefully will improve cash flow substantially over the core business. Given that the capex is so recurring and consistent, it must be noted that when added to the income statement, it completely wipes out all profitability and margins. I would expect to see a few things here going ahead: earning compression as depreciation piles up, leverage build up after the QIP funds are used up in 1-1.5 years from acquisitions and capex, with further compression of earnings through increased interest cost. The positive could be a good acquisition that helps improve the cash flow profile and maybe divestment of some of the more onerous assets once their order books are done with. At current valuations, find PI Industries too richly rewarded, for earnings that I don’t feel accurately reflect the cost base of the business. Feedback from others more knowledgeable on the segment / company welcome.

Disc: not invested.