Holding Disc: 5% of portfolio, since 3 months.

The stock fell to my average buy price today maybe because of news on Mumbai malls being allowed 24 hour opening times, Phoenix said they will keep open till 5 am. Analysts think this is loss making proposition as footfalls will be low.

Good time perhaps to take advantage and add, since as per prediction from ICICI report this is going to be a boom quarter.

Only 4% of shares is held by retail, 37% institutions with increasing trend and 59% promoter.

My investment thesis:

For a consistent performing RE player, it was among the cheapest valued of the lot. I liked the diversified income from both rentals and sales. Malls could be good business and Phoenix seems to know this space well.

Numbers looked decent, strong growth consistent with valuation, PE wise and seemed this consumption story/overall trend would be a good long term play.

Cashflows are healthy, debt is fine. CPPIB is co-investor in 3 recent under-construction projects.

WARNING:

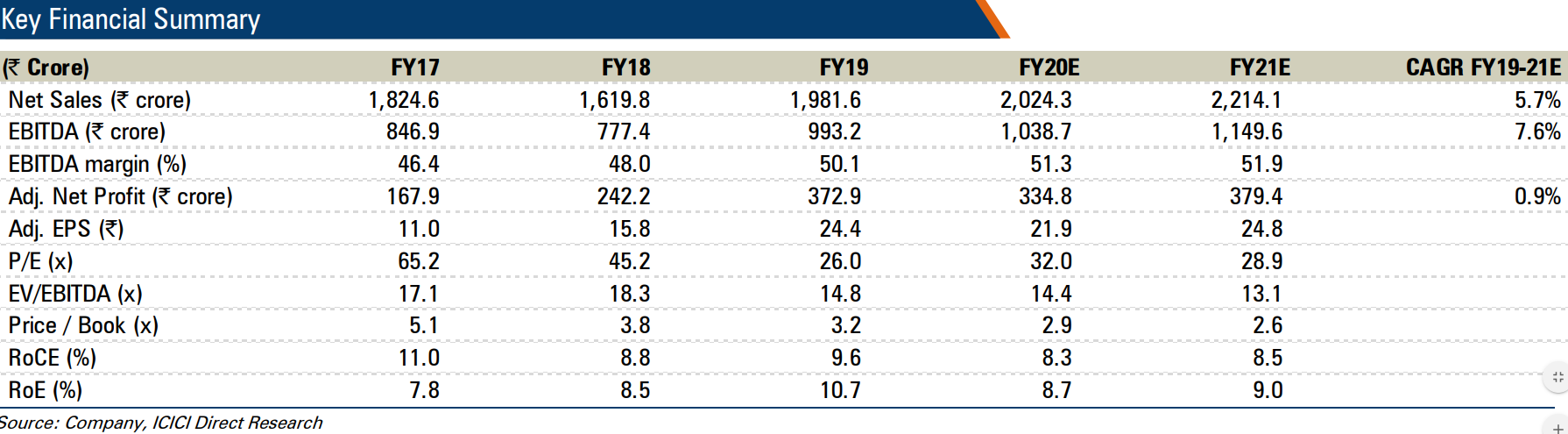

PE normally is 40-50 band, and the reason for low looking PE currently is revenue recognition from sale of residential properties in Q4 FY19 and some in Q2 FY20. Some of this recognition is now going to be a year away and not of this magnitude, about one third of these two exceptional quarters.

So all is business as usual, growth is just steady ignoring these 2 bumps, CAGR 15% expected.

4 malls to be added in 4 years, with some office spaces, with Lucknow doing well early this year.

The revenues are 80% or more based on lease/rentals, with multi-year (3-4 year) timelines looks like.

For the rest the research report of ICICI direct looked promising:

http://content.icicidirect.com/mailimages/IDirect_PhoenixMills_Q2FY20.pdf

-

Delivers steady performance in Q2FY20…

Phoenix Mills’ (PML) topline grew 2.6% YoY to 415.1 crore. Adjusting for residential business (11.2 crore), core portfolio (retail, commercial & hospitality) revenues grew 6.1% YoY to 403.9 crore. The EBITDA margin expanded 180 bps YoY to 50.8%. RPAT grew 6.0% YoY to 65.8 crore,

which includes 7.8 crore net exceptional item. Adjusting for residential business PAT, core portfolio PAT grew 14.2% YoY to 70.8 crore. Festive season consumption encouraging PML reported retail rental income growth of 7% YoY to 259.4 crore while retail consumption growth was slow at 1% YoY to 1,694.8 crore in Q2FY20. Consumption was impacted largely on account of higher area under fit outs at a couple of assets and ongoing metro work near PMC Bangalore. On a positive note, the festive month of October, 2019 saw consumption growth of more than 20% over that witnessed in last year’s festive month (November, 2018), which is encouraging. PMC Lucknow (Phoenix Palassio) is expected to get operationalised in January/February, 2020. With this and with more than 20% area coming up for renewals in FY21E, we expect retail rental income to grow at a CAGR of 14.3% at 1,690.4 crore in FY19-23E. Commercial portfolio set to expand to ~3 msf Commercial business revenues grew 64.0% YoY to 26.4 crore in Q2FY20 due to higher trading occupancy of 91% at Art Guild House and incremental revenues from Fountainhead – Tower 1. Currently, PML has 0.96 msf office portfolio under development between Fountainhead – Tower 2&3 and at Phoenix MarketCity, Chennai. Addition of these assets would take total office portfolio to ~3 msf. Also, PML plans to incrementally add 3.2 msf office assets at HSP, PMC Bangalore (Whitefield & Hebbal) and PMC Pune (Wakad). To incur 815 crore capex in FY20E; 2,000 capex post FY20E PML would incur total capex of 815 crore in FY20E (~ 230 crore incurred in H1FY20) towards the five under construction retail assets, leaving it with a balance capex requirement of ~2,000 crore by FY20E end. This would be funded through a mix of equity and debt. The company’s total debt was at 4,662.9 crore as of Q2FY20. On the tax front, PML would follow old tax regime for two SPVs – Classic Mall Development and Island Star Mall Developers (due to large MAT credit availability), while it is assessing tax implications and could migrate to the new tax regime for other SPVs. -

Valuation & Outlook

We remain positive on PML given its quasi play on India’s consumption story, quality of retail & commercial assets, healthy balance sheet & strategic expansion plans. We roll over our valuation on FY21E estimates and maintain BUY recommendation with an SoTP based TP of 870/share.