Sept 2019 Result:

Sales is down QoQ and YoY. I was not expecting this as company is shifting towards specialty chemicals.

Profit is little Up QoQ but not YoY.

I have been looking at the financials of this stock. Apart from the significant improvement in the financials in the past 3-4 years there are few things regarding their investments which I am not able to understand.

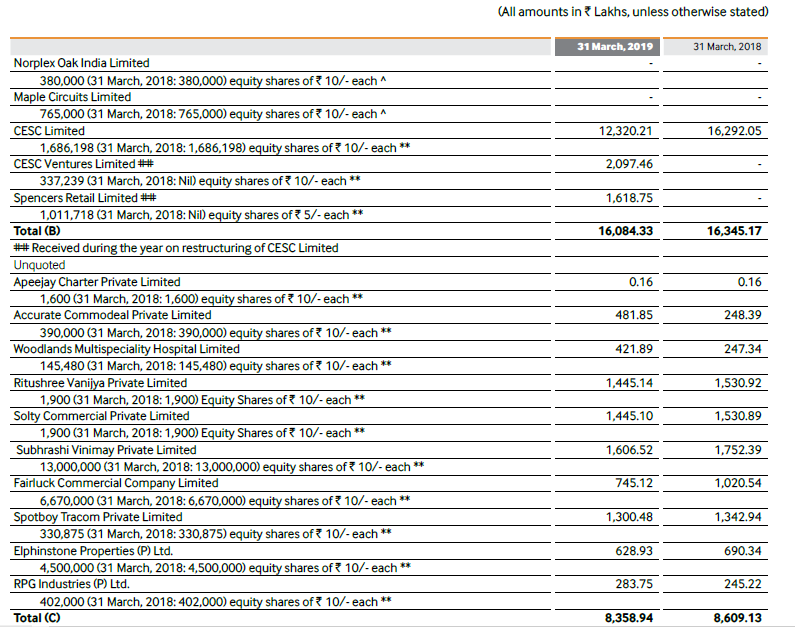

Company had around INR794cr in total debt as of March 2019. Inspite of this company has held investments in lot of group entities to the tune of 200-300 odd crores. Snapshot below from annual report 2019 pages 130/225. Group company Rainbow Investments owns around 50% stake in the company and Phillips Carbon holds 2% cumulative non convertible redeemable pref shares worth INR50cr (which is not for the benefit of the minority shareholders as investment is earning low interest) . In FY19 company also invested around INR60cr into liquid fund of ICICI Prudential. I am not able to comprehend the strategy of the company to invest into group companies and liquid funds rather than paying off debts which will help in reducing the finance costs and improve return on equity.

Can someone help with insight which I may be missing here.

1 Like

Mate, this is an RPG (Sanjeev) co, and similar to many Indian cos - these investments are very unlikely to go. Buy them if you see value, or earnings momentum. The latter is dependent on growth in pigment black (as there are literally only 2 players, including Cabot). However, we are more likely to see dip in profits, as there is moderation in spread/ cyclicality of tyre related carbon block (it is still majority of earnings). So wait to see normalised earnings, not a px to be negative or positive from near-term perspective. Waiting for Q3 results.

I see a substantial improvement in the RM cost due to the sudden fall in crude prices. Coupling this with a possible demand pick up in auto and the beaten up valuation the company is currently available, is there a good value in the medium term in PCB?

The result is ok but future expansion can be a big play here.

https://www.bseindia.com/xml-data/corpfiling/AttachLive/d4a09ad3-5587-47a4-a225-60f3f23a892c.pdf

1 Like

Its good to see that the company is working towards the capacity expansion in the south India which it had planned for last 1Yr+ and got delayed due to COVID effects in last 6-9 months. Has anyone attended the earnings concall or know of any management commentary on how they plan to fund this capacity expansion which needs ~600Cr? I see they do not have much of internal accruals (except short team cash ~150CR) on BS for now and in fact there is already some short term (~330CR) + long terms (~150CR) liabilities.

Any raising of debt for the project funding of 600 Crs means the D/E may go up to ~0.3 - 0.5. Not too bad but would expect the funding to come from internal accruals, at least partially.

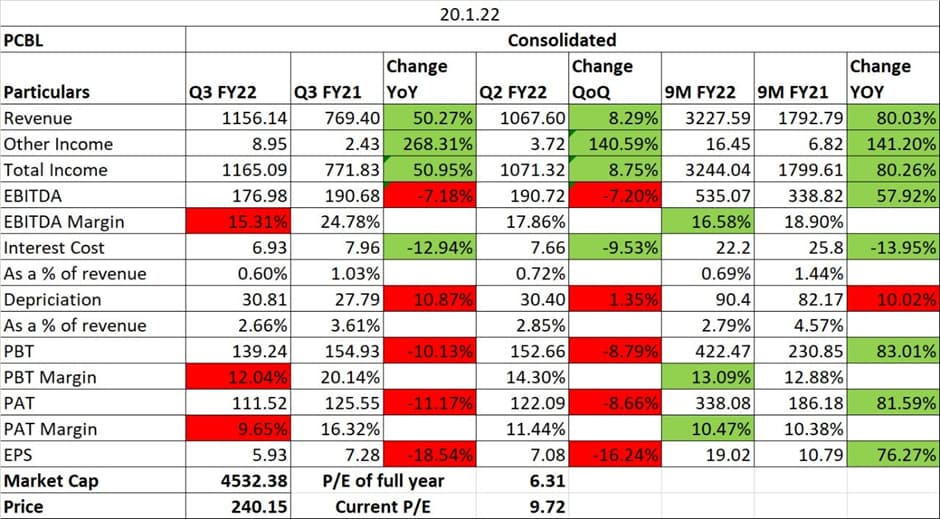

Strong Q3 numbers - the cost of sales looks significantly lower than usual - any one know the reason for the same?

Read the results here.

Declared a dividend of Rs. 7 per share as well.

Disclosure: Invested.

2 Likes

Till Nov-21 they have lower cost of raw material.

1 Like

Phillips Carbon Black AR Summary!

Automobile Industry to be the key trigger for growth!!

Disclaimer: Tracking & Planning to Invest

6 Likes

The company has raised INR 400 crore of equity through a QIP issuance earlier this month @246 per share.

Investors include HDFC Balanced Advantage Funds, Government pension fund global and ICICI Pru Life Insurance.

3 Likes

Good results

1 Like

This is cyclical commodity and there are new opportunities in this space is explored however highly capital intensive activity.

1 Like

ICICI securities coverage on PCBL (detailed report)

500% INTERIM IS SUBSTANTIAL

1 Like

- Highest sales volume of 116594 MT. Out of which 76621 MT from domestic sales and export sales of 39973 MT.

- Segment Wise: Tyres accounted for 71381 MT. Performance Chemical for 35378 MT. Specialty Black 9835 MT.

- Export sales jumped 18% QOQ. International demand is high. Selling in more than 45 countries. Established own office in various countries to not be dependent on a particular geography. Build up supply chain outside India. Also have tied up with a number of distribution partners overseas.

- Specialty black demand is very high as seen in the quarter. Have generated highest every revenue from specialty black in this quarter. Global Reach leading to addition of new customers.

- Power generation was also high this quarter. 150 million units in this quarter.

- EBITDA Margins reduced. Higher sales in export markets where there was container threat which lead to lower margins.

- In domestic demand, there was softness due to supply chain issues. OEM Production has reduced which impacts tyre demand which in turn impacts carbon black demand.

- Global Demand seems to be very optimistic. Semiconductor shortages are impacting OEM production. May normalise in Q4. May see increase in demand of Tyre as and when OEM production picks up.

- Higher logistic costs remains a challenge in export markets.

- As there is diversification of product portfolio, so change in name of company to PCBL Ltd.

- Expansion Plans: 150000 MT Greenfield project for Carbon Black, 24 MG Power in Tamil Nadu is progressing well. Brownfield expansion project of specialty black in Mundra. Also Power plants expansion in Kochi and Mundra.

- Freight cost has been higher this quarter. Availability of container ships has been a major challenge. Margins are affected because of this cost increase. Will get back to normal in Q4.

- RM costs will further increase.

- Want to create balance between domestic markets and export markets in the next 4-5 years. Don’t want to be completely dependent on one market.

- They have started developing different grade specialty black and performance chemicals which helps them get higher margins as they are customized to a particular customer.

- There is some kind of price arrangement in about 70% of the customers and there is an impact in the pricing when it comes to the rest 30%.

8 Likes

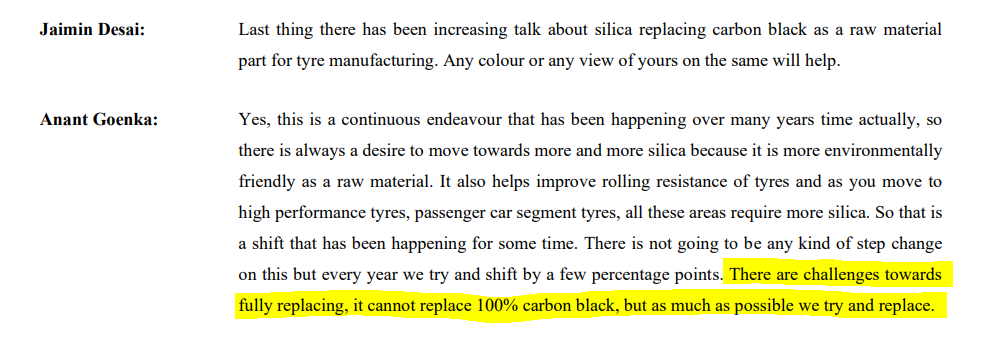

Anti-thesis pointer for PCBL.

"CEAT, he added, is looking at recycled rubber to make the product greener as well as using silica instead of carbon black"

3 Likes