Think we can add very generic kind of news on sectors in this thread. Request admin to move it to appropriate section if needed.

The news is about the DPCO (Drug Price Control Order).

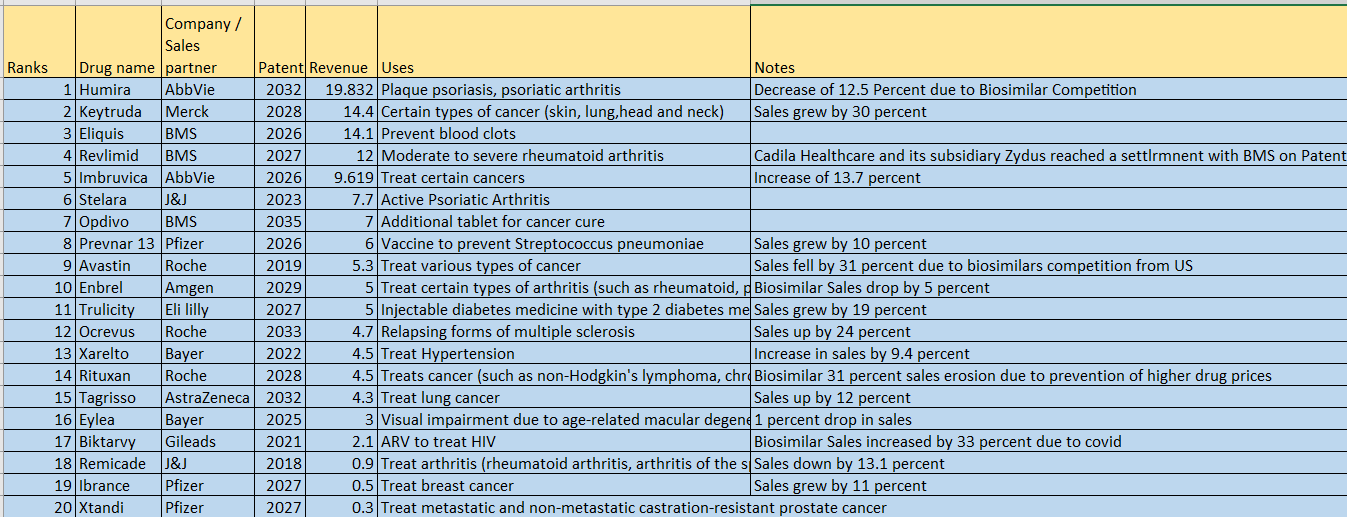

Finally the ball seems to be rolling, and govt. has passed the DPCO. Some important sections reproduced here. Now the moot question is which drug companies are impacted by this and which will not be. Any idea ?

The government on Thursday issued the long-pendingdrug price control order, paving the way for the implementation of national pharmaceutical pricing policy, which will lead to a reduction in prices of medicines on an average by 20-25%, and in some life-saving ones, by up to 80%.

Prices of 652 formulations under 27 therapeutic areas like anti-allergic (cetrizine), cardiac (aten), gastro-intestinal medicines (ocid), pain-killers (paracetamol) and anti-diabetic drugs (insulin) are expected to come down. Others in the list include anti-fungal, anti-tuberculosis, anti-leprosy, anti-hypertensives and cancer drugs. In certain cancer drugs, prices may come down by up to 80%.

Over the next few weeks, drug pricing regulatorNational Pharmaceutical Pricing Authorityis expected to announce in tranches the ceiling prices of 652 formulations, which will serve as the benchmark for companies. The industry will be given 45 days to clear the existing stock, and make the relevant changes in their prices.

The policy uses a market-based pricing method: ‘the simple average method’ for determining the ceiling price of all the molecules (drugs) under a particular therapeutic area with over 1% market share. The price to the consumer will be determined by adding 16% margin (to the retailer) as well as the local taxes to the average price (ceiling price).

Addressing the concern of public health NGOs, the DPCO clarifies that companies will not be able to increase prices, in case the ceiling price fixed by the government, is higher than their price. In cases, where existing manufactures, selling the formulations at a price higher than the ceiling price, will have to revise the prices downward.

Prices of formulations will be frozen for a year, and will be revised in line as per the annual wholesale price index, in April every year.