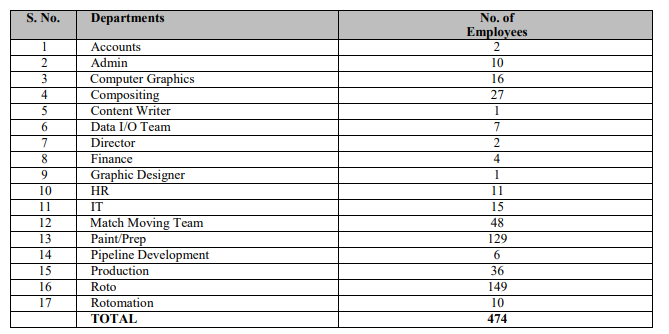

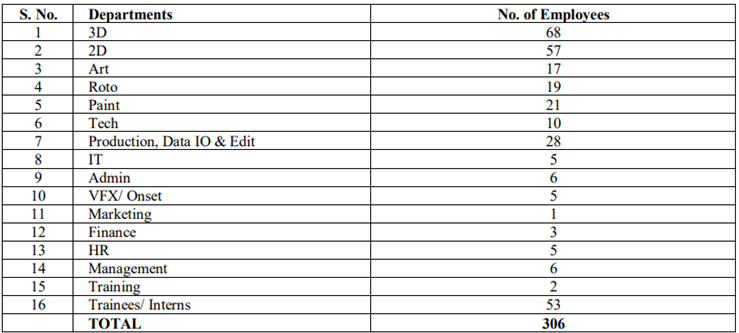

Clearly we can see Basilic has more of the Roto/Paint guys. Another thing if you notice is the work which phantom does (creative) requires them to train employees , hence they have people under trainees.

Project size

Basilic

They generally do smaller projects which is a quality of non creative business. Please see the number of clients they have worked for and compare to number of projects.

Phantom

They have worked with more number of clients but less projects. This indicates that they take up larger projects which is a quality of creative business.

Ayalaan movie project is held by 5 years. Initially phantom agreed to work on vfx for that project. They did some pre production work too. But after some time producer stucked with cash problem. So phantom stucked with them too. So phantom realised that without movie releasing they can’t get their payment. So in april this year they announced to produce the project (highly likely vfx work only).

Their are few positive as well as negative outcome possibilities there

Ayalaan project is to be made by more than 4500 vfx shots. One of the highest vfx shots indian movies. So if the movie became hit then there brand image will become more popular. They could easily charge premium for their upcoming projects

If the movie is further dropped or flop then they will be hit by 20 to 30 crores odd.

Since the time PhantomFX studios got added to the posters of Ayalaan, I was bit worried about this move and had slight fear.

My fear was this scenario…KJR Studios wasn’t able to pay PhantomFX, and there was a internal deal to do the VFX work at discounted rates. In return Phantom was given a stake in it.

Instead this is quite opposite to what I feared, Phantom has given 17 Crs to buy distribution rights…if you think, who else other than Phantom will be the best judge of the success of the film

Phantom is involved in this project right from the beginning and knows the whole story…they are handling entire VFX for the film which is one of the biggest in Indian film with VFX shots anywhere between 4000-5000 …Plus they have the full output in front of them before deciding to take a bet on this…a early bet at a discount

On top of it, since this is a sci-fi / Alien movie, content would appeal for Pan India…I guess there are couple of Bollywood heroines and AR Rehman is the music director…Also this movie director has prior experience in sci-fi movies and has given a hit before in association with PhantomFX as VFX company (Indru Netru Naalai with 8/10 IMDb rating)

In all probability this looks like more than a safe bet to me … won’t be surprised if this turn gold like KGF

@RocketMan If you remember my message in June that receivables will be an issue for this company. But you had shared a video that all issues are resolved. Now you see from this issue of KJR Studio what I meant. This is a very common issue in the film line. So again I will reiterate my point of view. A very high risk high reward bet.

I am holding for long term,

Given the company has very high margins,

High revenue growth,

Low attrition,

In Sunrise Sector,

Debt Free,

Authentic promoter,

Decent valuation,

Small in size.

Vman ji…As an investor, I was trying to assess the risk reward of this investment…Whether PhantomFX will be able to recover this 17 Crs investment partially or fully or more than that …

I had presented some points on why the movie probably might do well…and I might be right or wrong on each of these points…like for example 4000-5000 VFX shots doesn’t guarantee a hit like we saw it from Adipurush, Brahmastra kind of movies but our expectation is always to the likes of Avatar, Dune or any VFX heavy Hollywood movie… similarly AR Rehman music could be a let down…or it could be totally other reason which none of us as thought about

As an Investor, we need to get into the shoes of Promoters…what we would have done if you are running the show and got into this situation…and see if this step makes sense to you or it’s too risky … its also not that whatever I think will happen as is

If you have different views, please share it for the benefit of all investors

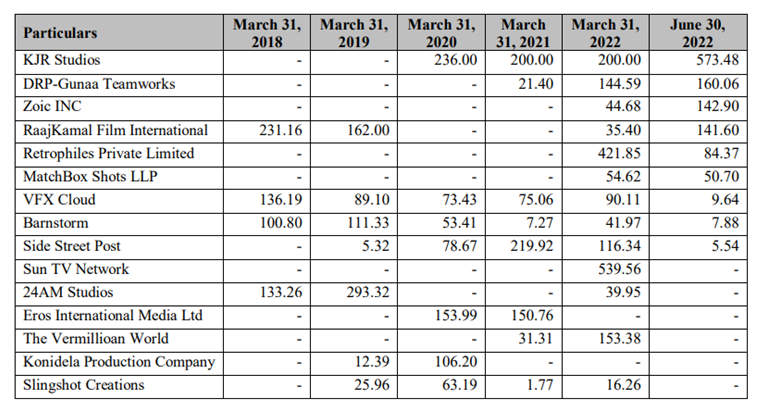

In my opinion, the right question to ask is why was this necessary and is this likely to be a one-off? In all the euphoria around the stock and storification of the business and its prospects; we as investors ignored the clear risks to the business model. If you strip out everything, this business effectively provides unsecured financing to one of the riskiest segments in the country (albeit at a high margin): film production; which are known to have delays, production risks, marketing risks, etc! In my opinion, receivables issues are likely to be a feature of the business model as long as the clientele includes mainly Indian and regional film producers. Just for reference; the amount “invested” in the production of this film is 33% of the company’s total networth! Doing VFX work for internationally reputable clients like Disney, Netflix, Amazon Prime, etc is very important, and one of the main differentiation factors will be share of business that comes via them rather than from local move producers.

@Venky_Thiriveedhi Its always important to invert always invert and see what could go wrong. So If I am in your place I will assume that this 20 -30 crores is gone down the drain. Then I would try to value the company and decide what is the right price to pay for it. That’s the best approach when you invest in stocks.

All your points are valid. Same was valid in case of Prime Focus when it had got listed. So just trying to invert and see what could go wrong and what is the right price to pay. Surely the management will do its best to resolve this sooner or later. But we need to be vigilant.

When prime focus listed it was 3D Animation company not VFX company only when it acquired DNEG it became a VFX company .

Things have changed since than lot of creative vfx work is now outsourced to India which was not the case 5 years ago.

Just look at the numbers of all indian vfx company they have skyrocketed in last 2 years.

@Vman ji …there are many things which could go wrong in any business… instead of focusing on what and all things could go wrong and fearing about the probability of its occurrence…mostly we will not be able to invest in any company with this mindset… Instead, I would prefer to bet on the team / management who could handle any situations irrespective of whether they are knowns or unknowns …and handle it in the best possible way with the resources available to them at that point of time

My request was to think from the point of view of promoter / CEO and see what could be the best step forward at that point of time …In the end, I was expecting that you would put up some reasons on why this is a bad step and understand why this investment is bad …Looks like you had made up your mind that this is going to be a complete loss or even more than that and it’s fine to have a different opinion

For all the investors who are following this thread, please note that apart from the factors I had mentioned in my previous post there are many other things we need to look into to assess the risk involved… Like for example things like, whether this distribution rights is for Theatre or Satellite or OTT…In case of Theatre, whether it is for all regions or for a particular region and for which language version…Is this an outright purchase or on profit sharing basis and any terms in case of movie not doing well etc;

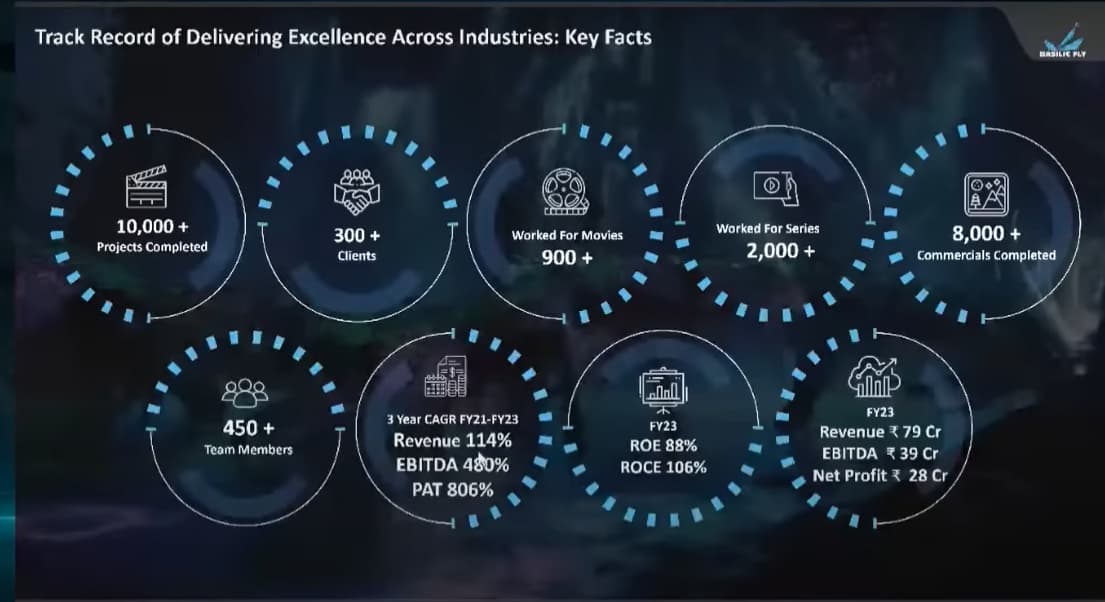

It is more clear that 90% of their work is sub contract and they are looking to add more direct work

Interesting thing is that even with sub contract work they were able to get such a high margins of around 35% …assuming these direct premium contractors are having a markup of 10-20% on top of it, so they will be getting around 45-55% margins

I guess PhantomFX is not yet in a position to command such a premium rates and would be aspiring to get into this league at some stage

This is kinda being made out to be either-or discussion past few days. An industry which has grown > 50% in recent years and will continue the trajectory, has plenty of room for multiple players. Just imagine Indian IT service Industry in late 90s.

In my view when it comes to skills or the kind of work these companies do, it wouldn’t vary drastically. Even if it is different, the clarity to average investors would only emerge after a certain scale when companies start defining a more formal structure with clear distinction of verticals along with revenue breakup, future plans and so on.

In the beginning these companies are small and subjective monoliths.

So if you are convinced with the future of this industry, do invest in both if you can. If you don’t have money for both due to their ticket size, pick one. If you are a beginner and can’t risk 1-3 lakhs in one stock, wait till they move out of SME board. Liquidity would be a problem till then.

@Venky_Thiriveedhi I appreciate your thought process. But we have to understand that we are investors. We are still not going to run the show. We have to pay a price for the stock and whenever you purchase a stock you want it at best possible price where you can get high conviction that the stock is to be bought at a particular price from where our returns will be alpha. In order to have that mindset you will have to take worst case scenario and value the company. What you are building in is a best case scenario. That is the reason I am assuming this money is gone down the drain.

@RocketMan I appreciate your macro view on the sector but getting paid in time isn’t related to any industry. As an industry there may be norms of payment but issue is more related to quality and stability of your customers and your bargaining power against them.

@Venky_Thiriveedhi Also let me clarify that I have never said its a bad investment. I was trying to see what is the right price to buy this stock or whether I should ever buy this stock given the fact that customer payments in this industry have been an issue since long now.