I agree with your views

I have been studying about INVITs and REIT’s and other instruments with some predictable cashflows.

After reading above thread and doing my independent thinking, I seem to gravitating to the following, (the views are tried to be elaborated in a context of geopolitical risks and other asset class yielding dividends or delivering particular returns )

Pros for PG INVIT

-

Good Visibilty of cash flow.

At a price of 86.7rs per share on 18/11/2024 closing basis and assuming 10rs as DPU annually the yield would be around 11.57% . -

Having low debt on it BS, the company is well positioned to acquire good assets than its peers.( other listed player’s seem to have lot more debt )

-

with current geopolitical uncertainty , this seems to be a good place to diversify.

4)Again, if one believes in mean reversion, equities at current valuations also, are more prone to time and price correction at this time.

Whereas other assets like gold, bonds ,Reits, Fractional Investments in realestate, Bonds and FD’s are offering much lower returns than the DPU offered now ( and likely to offer over longer period of 5years or so) to retail investors.

Here I am not even comparing the risk associated with other asset class as I compare it to investment in PG Invit.

-

Many in contributer to this thread, have expressed that rate cut seems eminent in near future.

Moreover the trend of rate cuts seems to be less doubted over a decadale of period. Thus, if the Invit is looked upon as a bond( assuming no growth in asset) the cupon rate offered likely to kick in demand sooner or later. -

Unlike other assets, the demand for power transmission looks to remain strong and residual life of assets of about 29 years offers a good longterm visibility of cashflows.

-

With just 3 Invit’s and 3 to 4 Reit’s in our market, these assets need to perform and create opportunities for other players to unlock value and tap the markets.

-

At some or other point,these instruments is likely to find chase and catch fancy of Insurance companies and mutual funds ( with rush of sustained flow to capital markets).

An individual investor has liberty to invest, cash out, keep some gunpowder dry, unlike MF’s who beyond a point cannot sit of cash and need to hunt for opportunities with less drawdowns.

Cons

1)During the latest concall, company mentioned, its first priority is acquire the balance stake from Powergrid which is likely to have lower contribution to enhance DPU.

Thus low growth in asset portfolio and or misallocation seems to be the risk.( but such risk exists for any other listed non-invit company)

My conclusion

Thinking in terms of probability, at current juncture reward outweighs risk…

Discoslure:

Invested and looking to build more position

6 Likes

Excerpts from Rating agency

The InvIT has acquired 26% stake in four special-purpose vehicles (SPVs) - POWERGRID KalaAmb Transmission Ltd, POWERGRID Jabalpur Transmission Ltd, POWERGRID Warora Transmission Ltd and POWERGRID Parli Transmission Ltd, from Power Grid Corporation of India Ltd (PGCIL; ‘Crisil AAA/Stable/Crisil A1+’) on December 30, 2024, for a consideration of Rs 506.63 crore. The acquisition was funded through additional debt of Rs 506 crore raised at the InvIT level. With this acquisition, PGInvIT holds 100% stake in all five assets (including Vizag Transmission Ltd).

PGInvIT acquired five operational transmission SPVs from PGCIL in fiscal 2022. The assets have an operational track record of over six years with healthy transmission system availability above the normative level of 98%. Collection efficiency was 101% for the first six months of fiscal 2025 as all SPVs are interstate transmission system (ISTS) licensees, falling under the point of connection pool mechanism.

The reaffirmation reflects the stable revenue profile of the trust, with all underlying transmission SPVs operating under the Central Electricity Regulatory Commission (CERC) Sharing of Inter-State Transmission Charges and Losses Regulations, 2020. This, along with their healthy track record of maintaining line availability higher than the normative level and remaining life of ~28-year under transmission service agreements (TSAs), ensures steady cash flow. The rating also reflects the strong financial risk profile of the InvIT.

The financial risk profile is supported by low leverage, with debt of Rs 567.73 crore as on September 30, 2024, and ratio of net debt to assets under management (AUM) of -0.13%. Post debt-funded acquisition of 26% stake in the four SPVs, ratio of net debt/AUM will increase to around 6%, against 70% cap prescribed by the Securities Exchange Board of India for InvITs that are rated ‘AAA’ and have made at least six continuous distributions. This provides sufficient headroom for debt-funded acquisitions. Additionally, the long debt tenure (till fiscal 2041) leads to a comfortable debt service coverage ratio (DSCR).

Full link here Rating Rationale

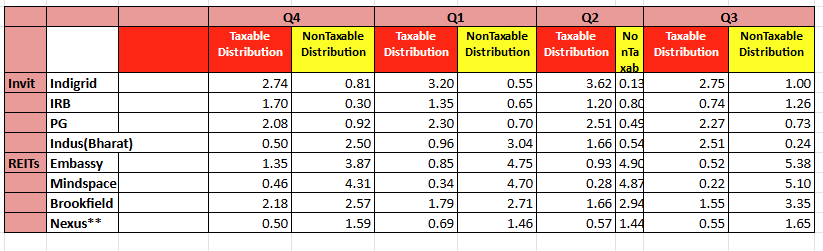

Can anyone tell me about detail taxation on PGINVIT. So, out of 3 rs. which you get every quarter, how much is taxable at investor level. At what percentage? As per tax slab or any special rate?

Because they are showing bifurcation as

Interest - 1.88 rs.

Taxable dividend - 0.39 rs.

Exempt dividend - 0.07

Repayment of SPV debt - 0.65

Trasury income - 0.01

total amount - 3 rs.

So, out of 3 rs., only 0.39 (Taxable dividend) is taxable ?

1 Like

Above two also is income and should be taxed per me.

Exempt Dividend, if its really exempt (not sure under which rule), then can be excluded.

Repayment of SPV debt, can be considered as loan repaid, so no taxation here, per me.

Someone can correct me on above with their understanding.

Although I don’t own this Invit, I can advise based on my other Invits.

PGINVIT will share with you Form 16 A detailing all TDS deductions made and accordingly elements where there is NO TDS, can be the Tax free amount. Same will also get captured in your Form 26 AS and start reflecting in IT portal.

I see below as Tax Free and all other elements will have tax implication

Exempt dividend - 0.07

Repayment of SPV debt - 0.65

Listen at the 45th minute, when an investor asks the Question on why Powergrid is not transferring assets to Powergrid Invit ?

Apparently, due to NMP (national monetization plan) guidelines…also, listen to the GST bomb that follows…

So, unless PGINVIT wakes up to reality and does something, …

PS - not invested/ not sebi registered/ not a buy/sell reco

5 Likes

Correct!

This actually shows the “adhoc” approach the bureaucracy operates. Some guy writes a guideline that assets can only be transferred on “returnable” basis, (without thinking of GST angle) and entire babudom follows it. No one even bothered to correct the lacuna/mistake for years.

Now it’s clear why the Entire drive of government to “free up” funds via monetisation of infrastructure has failed. Monetisation through

“Securitization” of cash flow is a mockery. Large chunk of precious and scarce banking liquidity is used/blocked in “securitization” of AAA assets of government, This liquid by banks should have been effectively used to provide liquidity in actual job generating and capex business while AAA assets could have been monetized by public funding which was the basic concept of InvITs.

2 Likes

I don’t like the sound of it. What are the GST obligations for PGINVIT or will it have to be paid by Powergrid using the money they raised while selling the transmission assets to the trust?

My understanding is that the GST obligations are for PowerGrid and not for PGINVIT - that’s what the guy is saying in the earnings call. I guess he is hinting that PGInvIT has to lobby to change the policy so that there is no such obligation on PowerGrid. As far as PowerGrid is concerned, they seem to be happy to securitize (for which GST doesn’t apply as I can understand) instead of dealing with such issues. As @praveen_sham says, it’s just ridiculous.

1 Like

Did PGINVIT held the conference earning call for Q3. Can anyone share the link. I am not able to fina any on the internet or on the website.

Nothing new ever happens in PGInvit. All that needed to be said has already been stated. Management needs to challenge GST laws so that Powergrid can continue giving assets to PGINVIT than relying on Securitization.

1 Like

Does anyone have any information by how much would the DPU be reduced going forward? For FY 25, the management has given a guidance of Rs.12/- which @ CMP of 80 translates into a 15% return which is pretty good IMO for a fixed return. Even if the DPU falls down to lest say Rs.8, its still a 10% return which makes its a compelling bet for someone looking at an alternative to FDs etc. provided the stock doesn’t correct further. Or am I missing something?

1 Like

Only rationale behind investing in PGINVIT, is Central Government backing and possible turnaround. Rest is all black in future for them.

1 Like

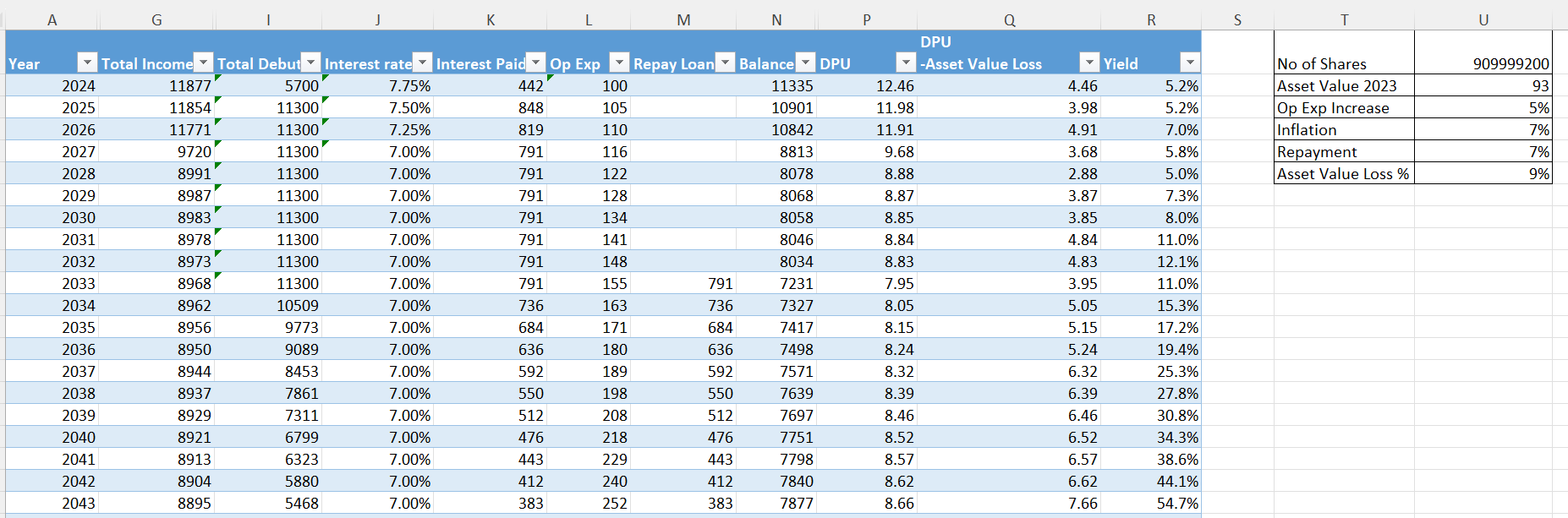

Here is the latest Yield calculations, if you have to buy the units as of closing prices today. It is the same running 4 qtrs based (3 quarters of this FY plus 1 Q from last FY, as of now)…I am also attaching the underlying calculation table of DPU…Qs/Comments are welcome, as always…

PS - Not claiming this to be perfect calculation. Taxation is a complex subject and hence do your due diligence,.,.,

1 Like

I have calculated based on my understanding and assumption that there won’t be any additional asset in the future. Kindly share your thoughts or point out any mistake in the assumptions or calculation.

1 Like

What is asset value loss ? How did u calculated it? If u don’t mind

Is revenue going to drop by 30% by fy27?

PGINVIT upload those infomation regularly. This is part of yearly asset value depreciation and more over this is mentioned as asset value, based on that the price of this INVIT goes down on yearly basis, so i have removed that loss from regular DPU to understand the yield after that loss.

I have pulled this data (income from 5 asset) from IPO prospect only, so we will see this dip in 2027 if they don’t add more asset.