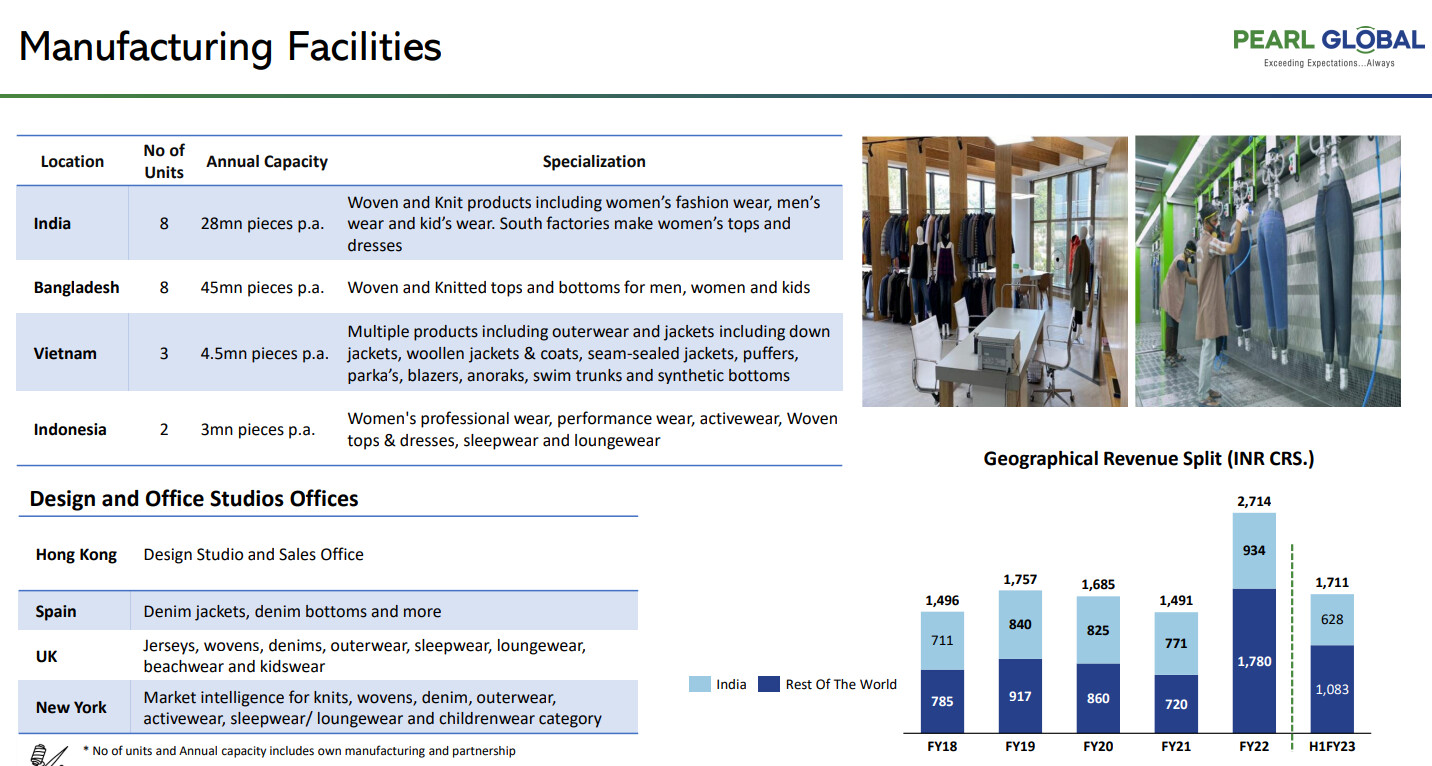

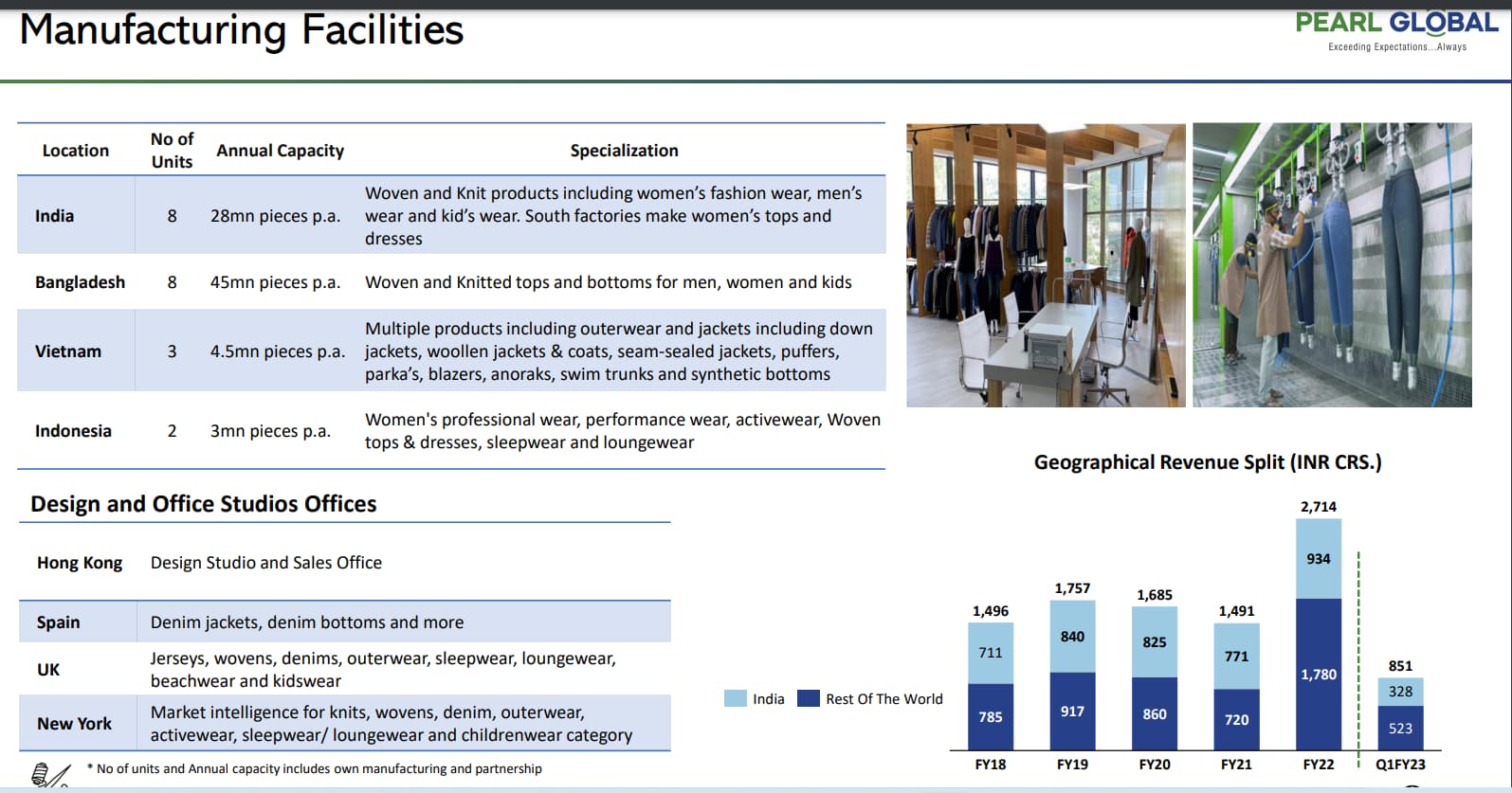

Pearl Global Industries Ltd established in 1987 by Mr. Deepak Seth is a multinational apparel manufacturing company that provides end to end supply chain solutions to brands across the globe. PGIL have presence Across 8 countries such as India, Indonesia, Bangladesh, Vietnam, USA, Spain, Hong Kong & U.K. It have well diversified and de-risked manufacturing base with 22 manufacturing units across 8 countries. Total capacity to manufacture is around 82 millions unit per year.

It have marque clientele -**KOHL’S , MACY’S TOMMY HILFIGER, GAP , OLD NAVY, NEXT, NORDSTORM ** among others.

In May 2014 PDS LTD was demerged from PGIL. The Sourcing, Marketing & Distribution (SDM) business was entrusted with PDS Ltd and PDS Ltd ceased to be a subsidiary of the company. PDS Ltd is now a successful multinational platform company delivering stellar results.

PGIL’s manufacturing facilities along with capacity and items produced.

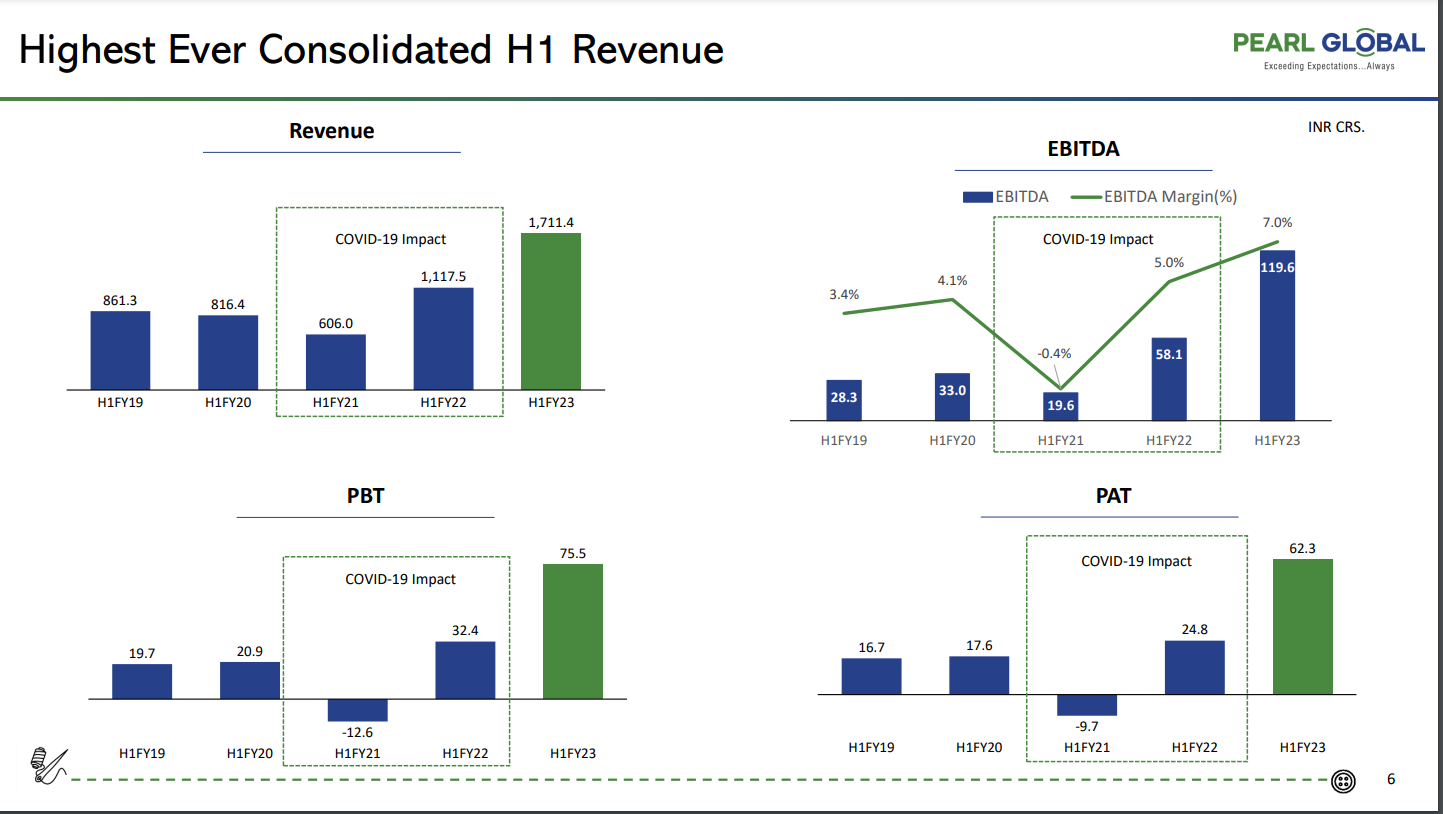

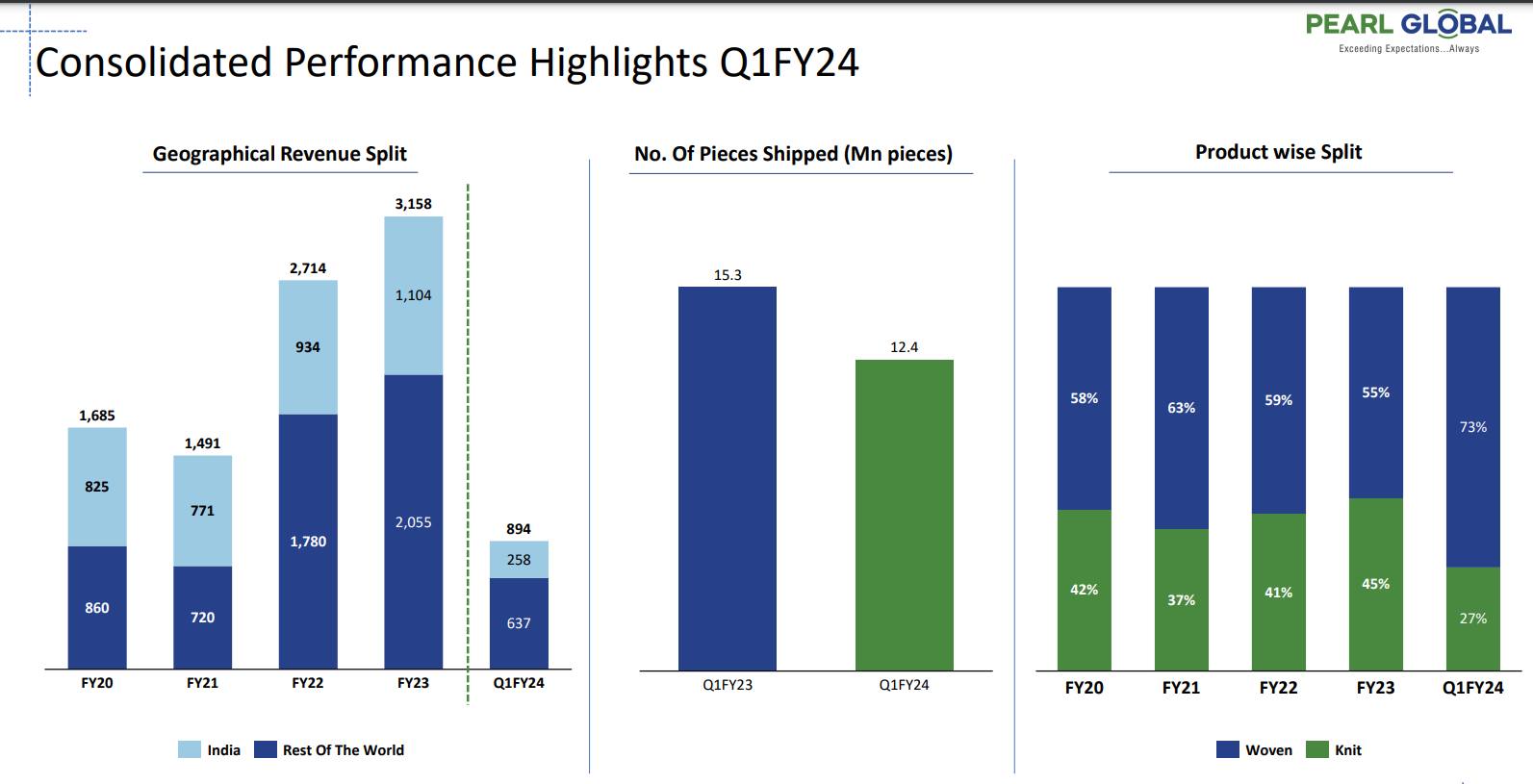

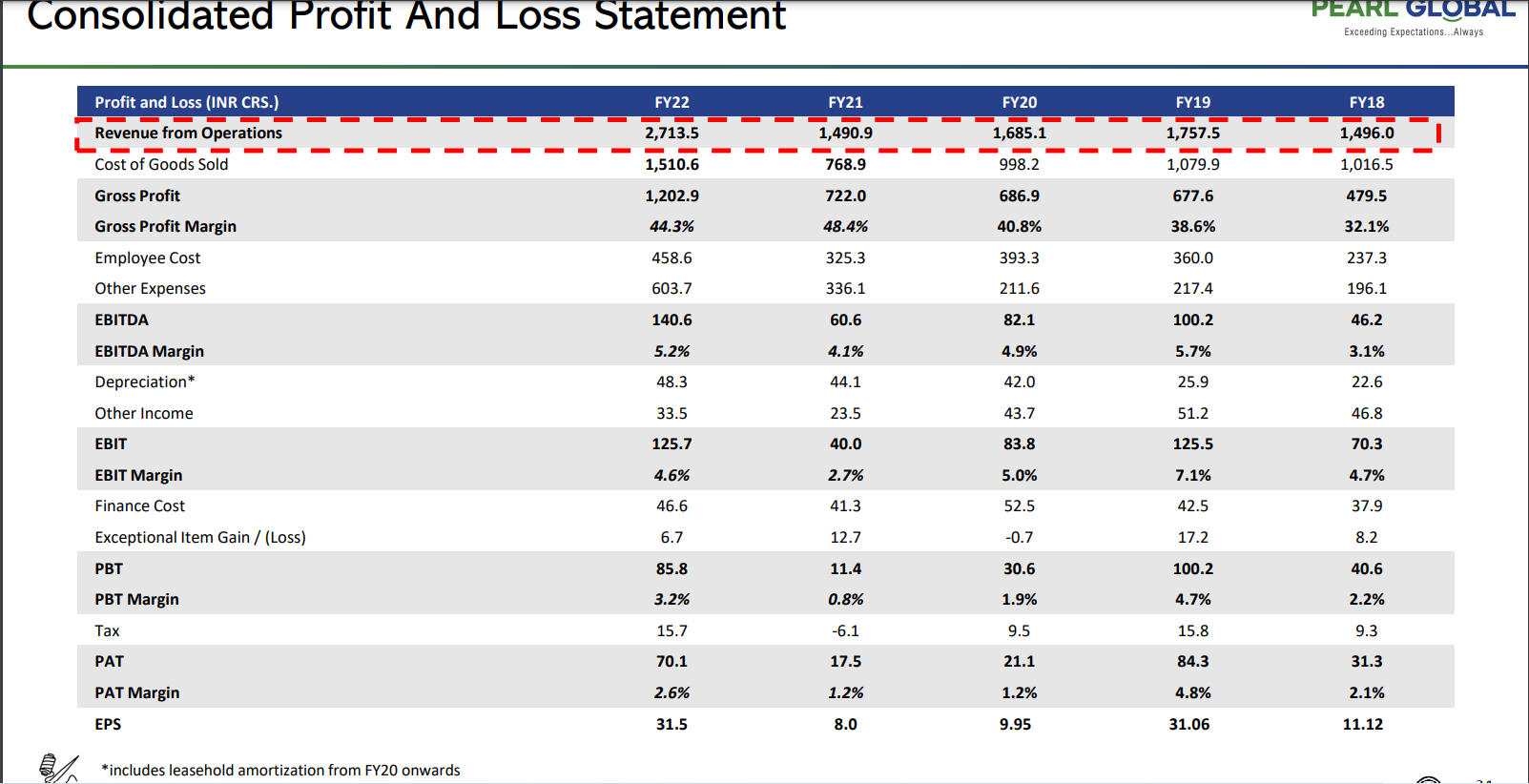

PGIL sales are growing rapidly consistently from 2018 onwards with GP margin in sync with sales with the exception of 2020-2021 due to covid.

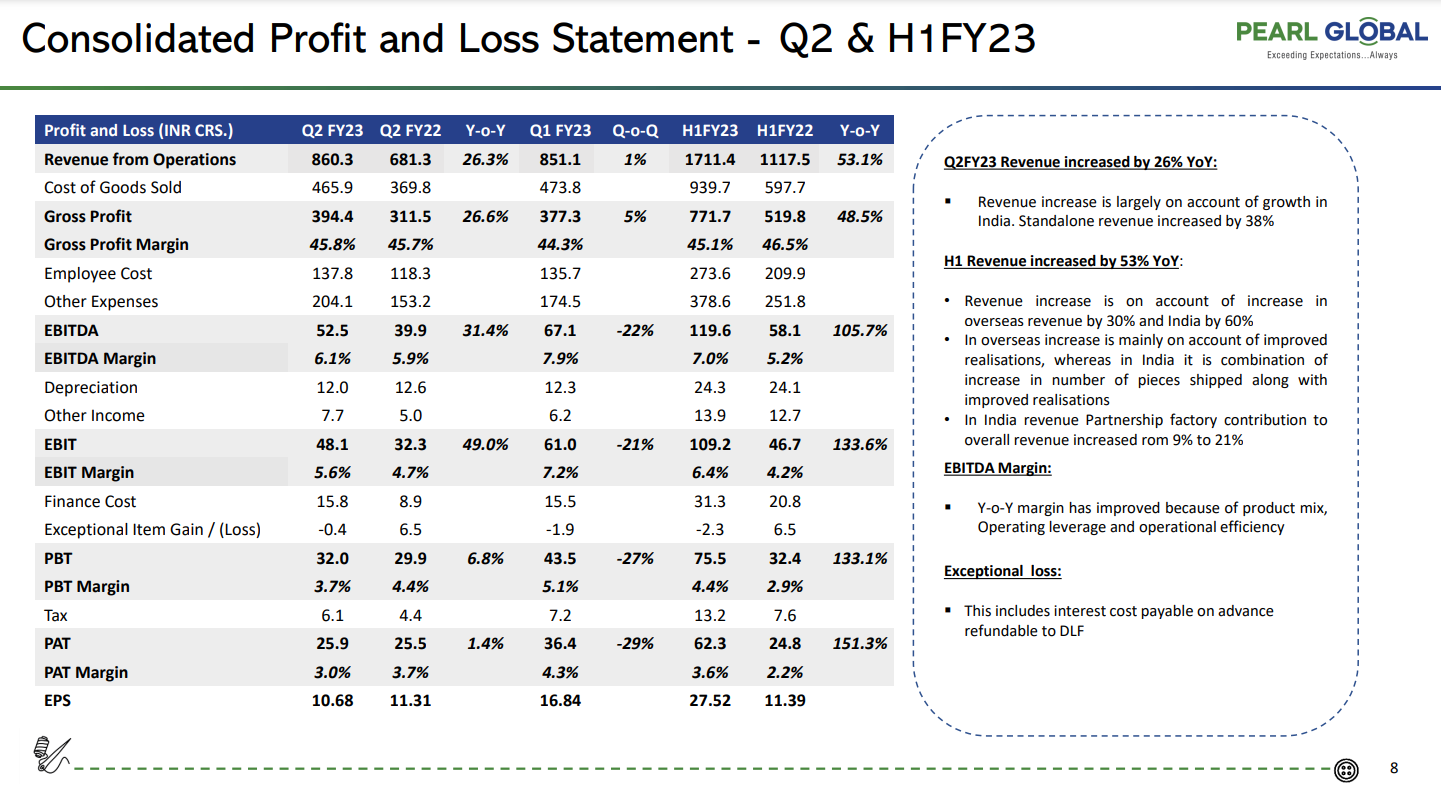

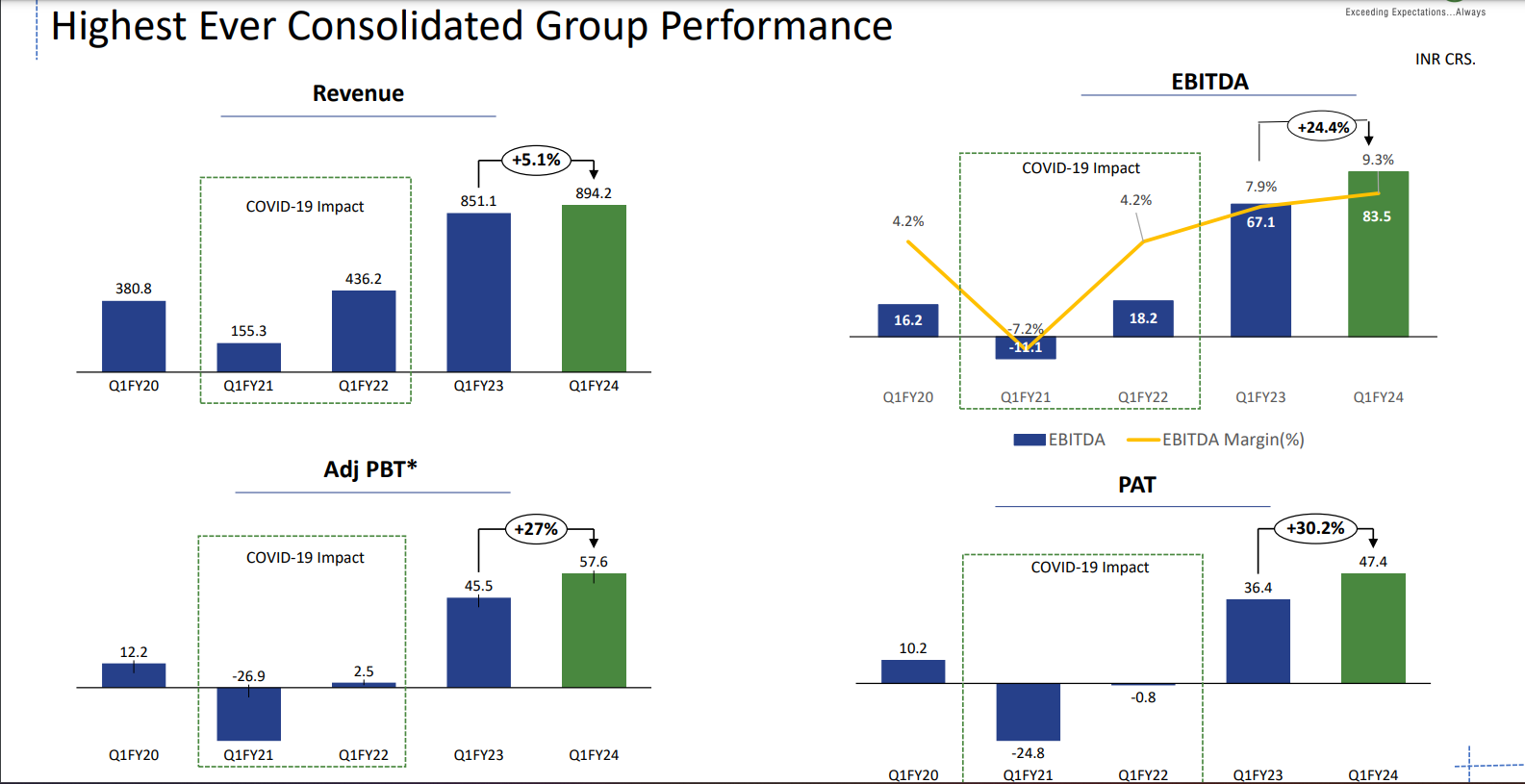

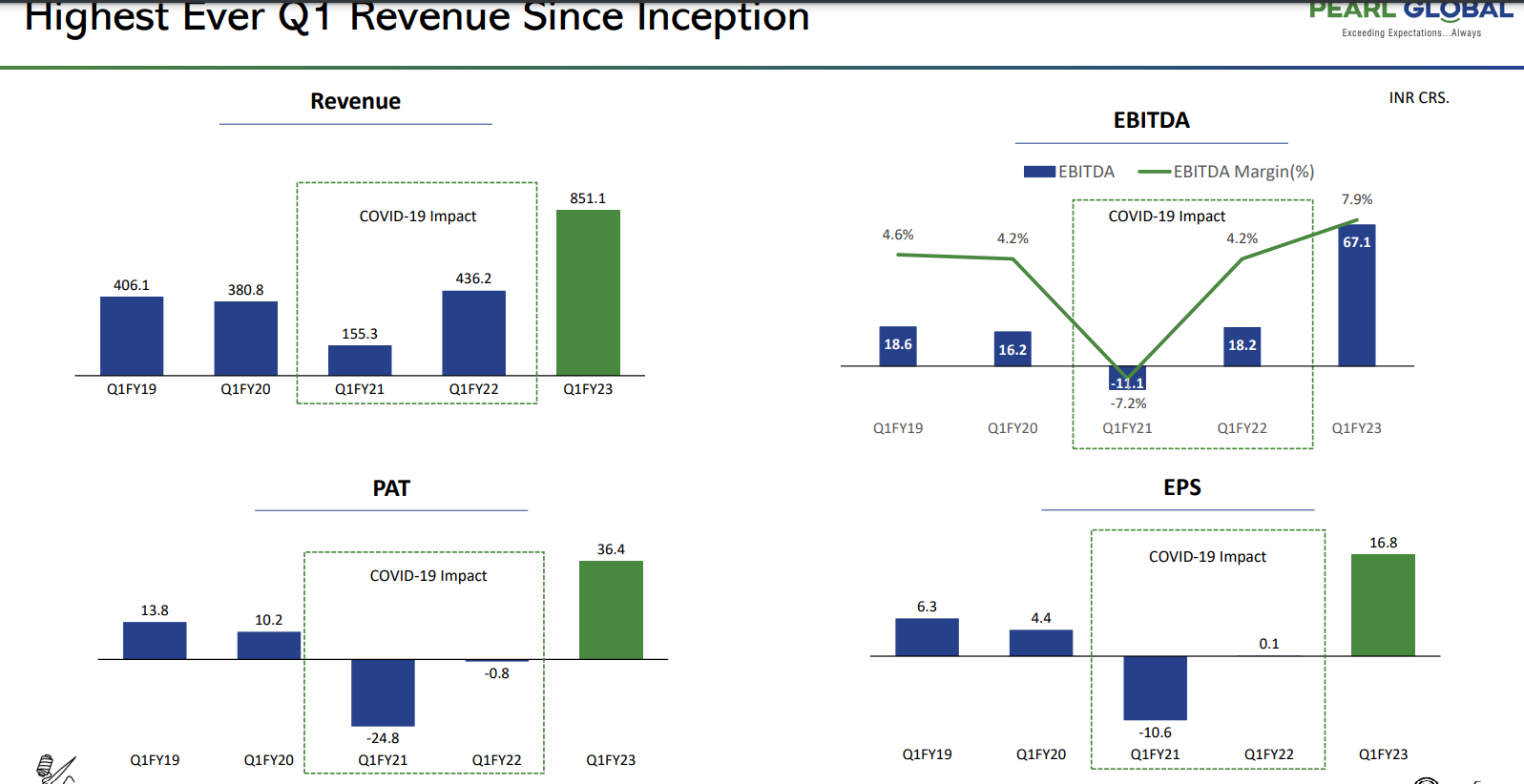

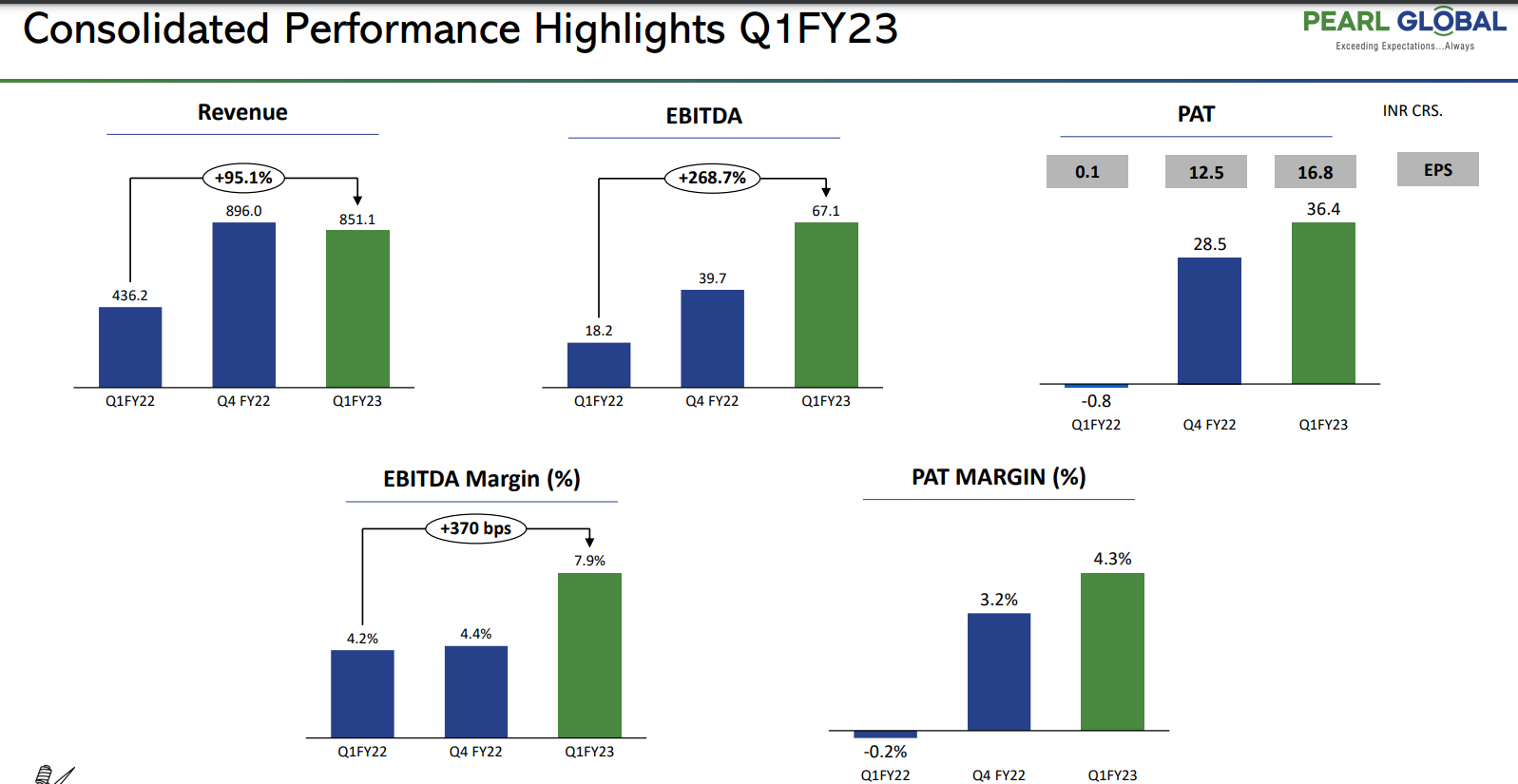

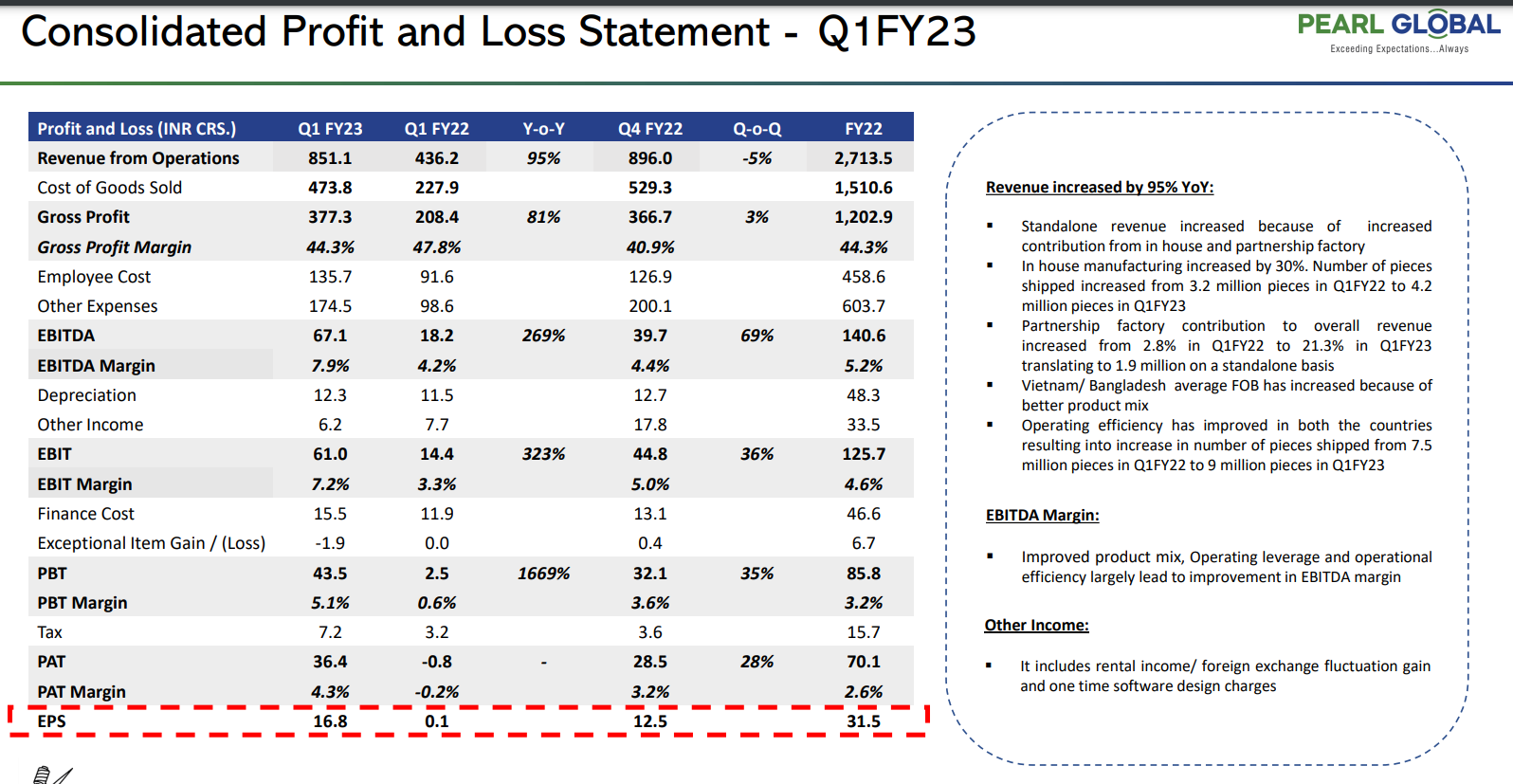

Now coming to QTR 1 FY 23. The results were steller with highest ever QTR 1 revenues since inception.

Positives

Company is consistently growing its sales and profits

Company is having multiple manufacturing facilities in low cost countries which makes it competitive

Increase in capacity utilizations for inhouse and partnership factories in India , Bangladesh and Vietnam with better product mix paints a brighter future.

PGIL can gain over the medium to long term on the back of China + 1 adoption

Promoter Holding is consistent about 67 % with no pledged shares.

Low market cap to sales ratio

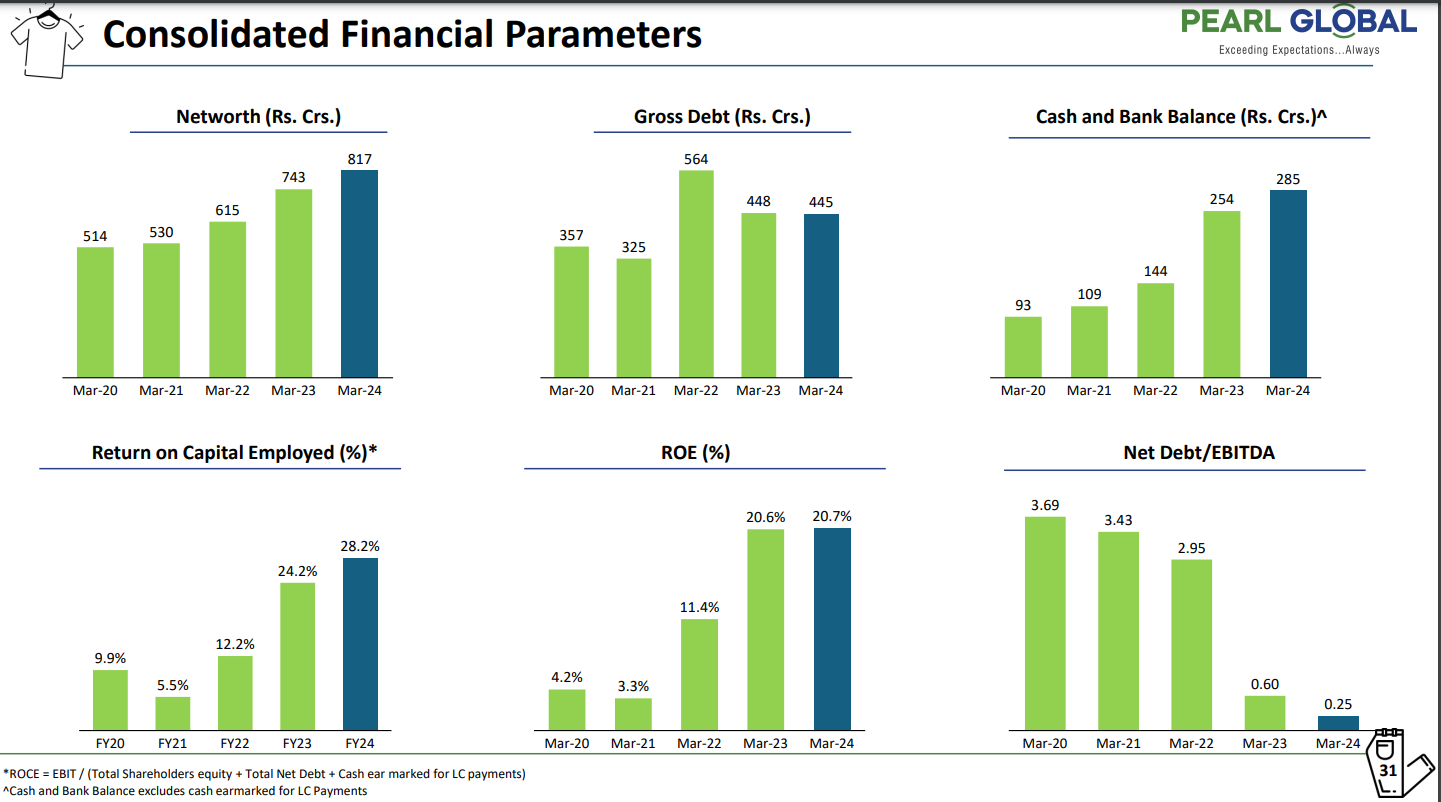

Debt Equity Ratio below 1

No of Subscribed Shares is 2.17 crs with very low floating shares

Famed investor Mukul Agarwal having 3.46 % shares as on June 2022.

Negatives.

Promoter having sister company PDS Ltd in the same line of Business

Cotton prices can have major impact on profitability.

EBITDA margins are fluctuating from -0.2 % in FY 18 to 4.4 % in FY 22.

Disclosure:- Having Position (This is not a investment advise. Please do your own due diligence)