Has constantly increased revenue and profits over the years and a debt free company

Honest Management. Probably the only IT Company which came out in even before the quarterly results and stated that it will not be able to meet the earning estimate. In common stocks uncommon profits it is well stated the good management will always not share only good news but also the bad news. This shows the integrity and honesty of the management

Well invested and equipped in next growth phase of IT Industry- SMACK and should help it out perform its peers in terms of growth, Since the size of the company is small compared to large peers it can grow faster than some of the large IT Companies.

Trading at around 20 PE and does not seem expensive at current valuation.

I see the company to be easily be a 30000 Cr Market cap company in 5 years .

Please let me know your thoughts or any other information that you might have about persistent systems

I remember in one of the Sanjoy Bhatta show that he too commented on the high MQ (management quality) of Persistent team. That said, this space is not necessarily about that alone. It has become a highly competitive field and there is a lot of poaching of middle tier talent. People keep moving and it is difficult to establish moats, in a consistent manner. My 2 cents -All said and done, might become a little more attractive, if there is at least some more correction, overall in IT space.

PS - This is not a recommendation and I am not a certified analyst. Pl do your due diligence

Most the information about persistent can be got through the website. They have an investor day meet presentation which gives lot of what the company is planning to do and gives good insight into the company.

This is no doubt a fantastic company. But it is richly valued at 21x IMHO. Especially, comparw it with Infosys which is trading at 18x and HCL Tech which is trading at 19x PE. HCL Tech’s Mkt Cap is 22 times that of Persistents and Infy’s is 40 times.

What I am trying to say is, it will surely give market beating returns. But it is no longer a hidden gem. FII and DIIs together hold 35+% in the company, so the story is already well reasearched and known to Mr Market.

Seems like a strong company except for the 2009-2010 revenue growth. With the current drop in prices, the company seems to be a worthwhile buy but I’ll wait a bit more before I make a decision to buy.

Thank you for putting it on my radar Karthik. Under valued, high growth and low debt companies are a hard find.

Most of the good companies in India are owned by DI and FII’s and have been great compounding machines. Classic example is HDFC. I feel its time retail investor get smarter and own these good companies . I feel mid cap IT companies can grow faster than the large cap companies. The couple reason is that larger companies like infosys have been focusing on margin and have not been keeping pace with the industry changes. The midcap companies are more nimble and more focused on growing revenue with lesser margin and exploring newer avenues to generate revenue. If we compare the stock chart of infosys and persistent this difference should be clearly visible. For instance just see the way cognizant has grown compromising on margin and focusing on attaining greater market share. The second reason is that mid cap IT’s handle talent better than large cap due to the size . I could be wrong in my assessment but hoping i would be right .

Some of the points above are very generic. Lets get to more specific questions. It is the hard-earned money which is going to be at stake(if one invests into this).

So…

Usual VP style questions:

What is the revenue distribution from various industries(Banking, Insurance, Healthcare, Manufacturing, etc)?

i) Is the company deriving majority of its revenue from a slow growing industry?

ii) Projected growth rate of each of these industries.

How does the company fare on Client concentration? (too much of revenues concentrated among too few clients?)

What about newer technologies like Cloud? - does the company have execution capability on this front?

Operating profit margin - A very important parameter to me. (need not be in the high 30s, even a mid to low 20s is fine). But what is going in(revenues) and out(expenses)?

There are many more questions. But these could good starters from where we could take it forward.

I can chime in with a lot of inputs from my side, if we have good start in the above discussion points.

Thanks,

Ravi S

Disc: Not invested into Persistent Systems

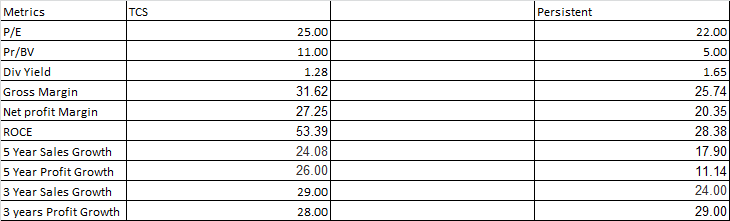

Above is some comparison that i had done between TCS and Persistent.

Persistent being a small company definitely has reliance on its top clients and has 35 % of its revenue from its top client based on the reports that i have read. On the industries contribution majority of their revenue comes from Infrastructures and systems.

The reason i invested in persistent is because of the third question you asked me. The SMAC is the happening thing in the IT industry and as per gartner this is next billion dollar opportunity in the IT Space. Persistent from the beginning has been a company which was working with many product companies like Saleforce etc to enhance thier product and started investing in SMAC capabilities from 2007. It has also acquired 2 companies in Clould Space in last couple of years .Peristent as company has done this whole digitization within their company for thier employees itself which i fell even bigger company like Infosys has done to that exent, which proves it defiantly has execution capabiltiies

Persistent sales is around 310 millions and with the growth in SMAC sector it will have a good growth rate. The question i asked myself was with TCS around 16 Bn revenue and persistent with 310 million revenue who can double itself revenue faster. I feel because of the investment in SMAC persistent will be able to grow faster than TCS in next 3- 5 Years because of sheer size .

I would like to know your thoughts or any other parameters that we would have to look at

I am waiting for 500s, where the safety net might be better. May become elusive though and that is a risk. I think, a couple of big red days, this will drift further

The price fall is a knee jerk reaction to the letter they shot off to exchanges. It is already at 15% discount to its fair p/e. You may not get Rs 500/- as it is the bottom p/e value. You will see a jump from Rs600/-.

@ks16, Hi Kalyan, the link pertains to Nitin Spinners thread. Pls find Persistent results, fact sheet and other info in below link-

The profit margin has come down as expected, but because of profit warning, there is big correction in stock price.

The company is selling more to Enterprises than ISVs now (19.7% in Q1FY’15 to 24.6% in Q1FY’16). Quick questions (any software/IT guys pls answer):

Shifting from ISVs to Enterprises : Isn’t it like moving up the value chain from subcontracting to direct bidding?

The company’s revenue mix shows around 82% from Services and 18% IP led. What’s the difference between these two? Does this mean Persistent is just like another software services company?