CMP : INR 111 (As on 4th Jan 2019)

Market Cap : INR 29.87 Cr.

TTM P/E Ratio : 7.83

Pee Cee Cosma Sope Limited is a Agra based company engaged in manufacturing of laundry soap, detergent powder, detergent cake and utensil cleaning cake. The company has three manufacturing units in Madhya Pradesh, Uttar Pradesh and Rajasthan. The company sells its products under ‘Doctor’ brand and enjoys good brand value. The company is not witnessing any growth in topline. The topline is same as it was five years ago in FY 2013-14. However, company‘s margins are improving. The company is managing its working capital very efficiently. It seems that the company does not sell its products on credit or the the credit is given for ultra short term period and the payment terms are very strict This is reflected from the fact that during last five years, the amount of receivables does not exceed 2-3 days ‘revenue of the company This fact may be the reason for no growth in topline. Low level of receivable also indicates the continuous demand of company’s products.

Financials:-

Company’s performance is satisfactory on bottom line front. The company has posted disappointed set of results for quarter ended 30th Sep 2018.

| (in Cr.) | Sep-18 | Jun-18 | Mar-18 | Dec-17 | Sep-17 | FY 17-18 |

|---|---|---|---|---|---|---|

| Income Statement | ||||||

| Revenue | 18.84 | 20.57 | 17.69 | 20.27 | 19.74 | 78.51 |

| Other Income | 0.01 | 0.01 | 0.02 | 0.00 | 0.00 | 0.02 |

| Total Income | 18.85 | 20.57 | 17.71 | 20.27 | 19.74 | 78.53 |

| Expenditure | -17.82 | -19.09 | -16.29 | -17.88 | -18.24 | -72.29 |

| Interest | -0.02 | -0.03 | -0.03 | -0.06 | -0.05 | -0.23 |

| PBDT | 1.03 | 1.49 | 1.41 | 2.39 | 1.50 | 6.24 |

| Depreciation | -0.14 | -0.14 | -0.19 | -0.16 | -0.17 | -0.68 |

| PBT | 0.89 | 1.35 | 1.22 | 2.23 | 1.33 | 5.57 |

| Tax | -0.28 | -0.46 | -0.46 | -0.74 | -0.44 | -1.90 |

| Net Profit | 0.61 | 0.89 | 0.77 | 1.49 | 0.88 | 3.67 |

| Equity | 2.65 | 2.65 | 2.65 | 2.65 | 2.65 | 2.65 |

| EPS | 2.30 | 3.30 | 3.10 | 5.60 | 3.30 | 13.90 |

| CEPS | 2.83 | 3.87 | 3.62 | 6.23 | 3.99 | 16.42 |

| OPM % | 5.47 | 7.23 | 7.99 | 11.79 | 7.59 | 7.95 |

| NPM % | 3.21 | 4.31 | 4.34 | 7.37 | 4.48 | 4.67 |

Source : www.bseindia.com

Company’s share is trading at trailing PE of less than 8 which is very reasonable for the company engaged in FMCG business with good brand value. Any slight improvement of performance will result in rerating of the company

Share Holding:-

The promoters’ holding is 74.70% which is very excellent. Rest 25.30% is held by public. Around 1/3 of total public shareholding is in physical form. It is interesting to note that small cap investor Mr. Dheeraj Kumar Lohia is continuously increasing its stake in the company since 3rd quarter of FY 2017-18.

Dividend History:-

Company is regularly and generously paying dividend. The company is continuously increasing dividend payout since FY 14-15.

| S.No | Financial Year | Rate of Dividend | Dividend Amount Per Share (Rs.) |

|---|---|---|---|

| 1 | 2013-14 | 12% | 1.2 |

| 2 | 2014-15 | 15% | 1.5 |

| 3 | 2015-16 | 18% | 1.8 |

| 4 | 2016-17 | 25% | 2.5 |

| 5 | 2017-18 | 30% | 3.0 |

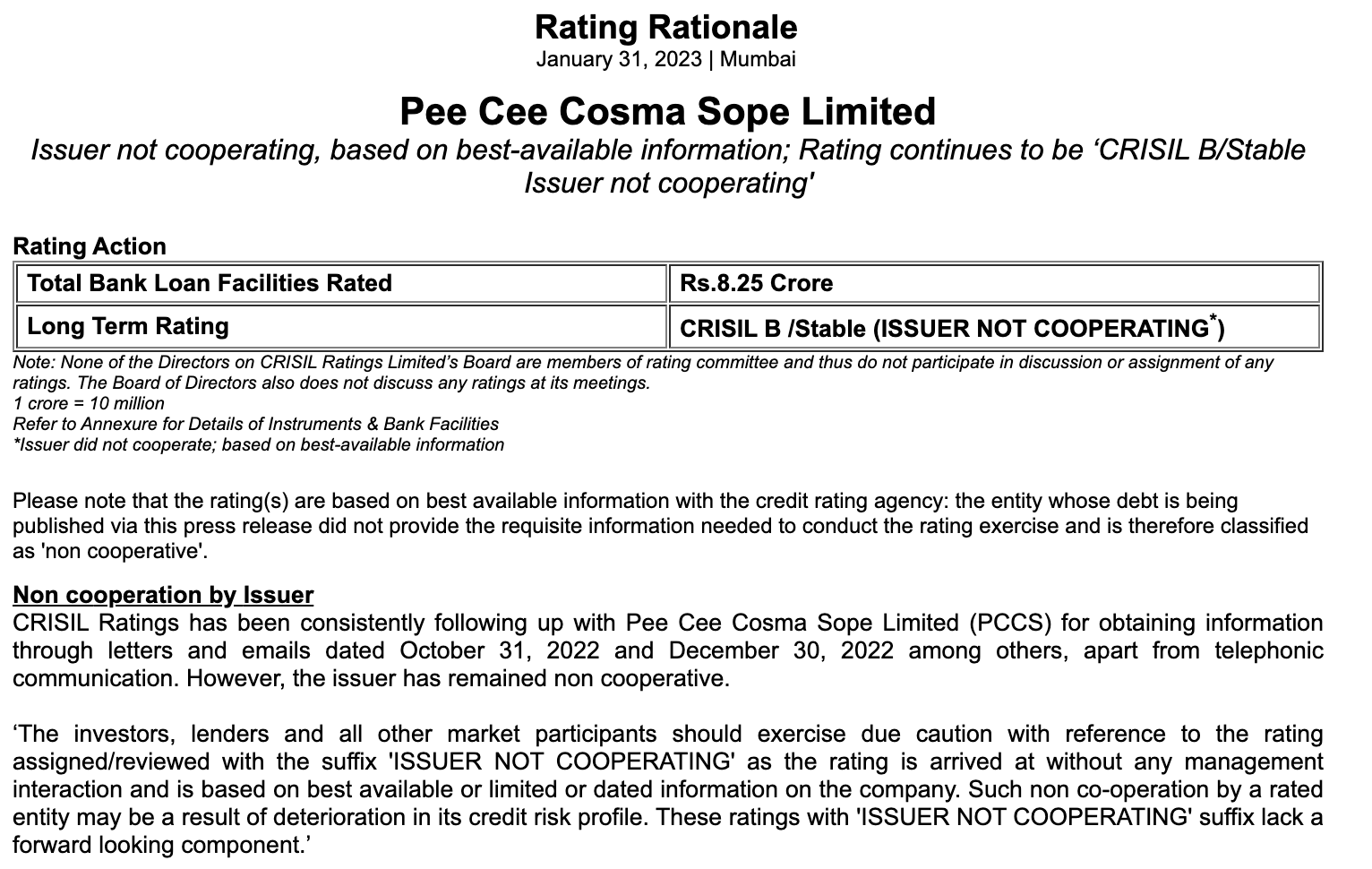

Credit Rating:-

Crisil has assigned ‘BBB-/Stable’ as long term rating with the suffix 'ISSUER NOT COOPERATING’. Since the company has negligible debt, this rating does not have any significance.

Summary:-

Positives:

- Well Experienced Management

- FMCG product with strong brand value

- Strong balance sheet with negligible leverage. Debt equity ratio is 0.07 as on 30th Sep 2018

- Efficient working capital management

- Very low equity base

- Return on equity is 18% in FY 17-18 and is expected to improve considering the continuous debt reduction and increasing dividend payout.

- Negligible Receivables

- Regular and generous dividend payment

Negatives:

- No growth visible in topline

- Increased competition from large players

- Illiquid Share

Disclosure: - Invested