At today’s price, PCJ market cap is Rs.7,000 crores. The buyback quantum is 424 crores, i.e. 7%. The non promoter holding is 42%. Hence, as a non promoter, the proportion of shares that will get bought back is ~17% at 350/share. So, if bought 100 shares at 170/share (yesterday) and tendered 17 shares at 350/share. Then the implied acquisition price per share is 133/share. Implying a market cap of Rs4740 crores (post buyback). This is 0.6x reported FY17 sales and 11x FY17 PAT. The real question hence is, EVEN IF there is an issue, the question is how much!!

Are you saying post buyback stock will fall to 4770 crores (133 rs per share) market cap from 7000 crore market cap. What I understood is you are not talking the profit that you have got by selling 17 shares in buyback and decreasing the cost of remaining shares owned. But that does not mean , market cap/share price will fall to 4740 crores / 133 rs per share (just because of buyback.). Let me know if I misunderstood anything

I am saying that 133/share is the implied purchasing price for 1 share post buyback and hence implied market cap is 4740 crores. The math is (100170-17350)/83=133/share. (assuming 17% acceptance as detailed in earlier comment).

Also, if boarders can highlight in all previous cases of scams/governance issue, if any management has ever come forward with a Cash Buyback OR Dividend that the promoter said he wouldn’t participate in! I am just wondering if we are undermining the actions/facts for fears of unknown.

The math is (100 multiply 170 minus 17 multiply 350) divided by 83 shares = 133/share

Buyback size is around 3 percent of the outstanding shares. Calculation needs to be revised.

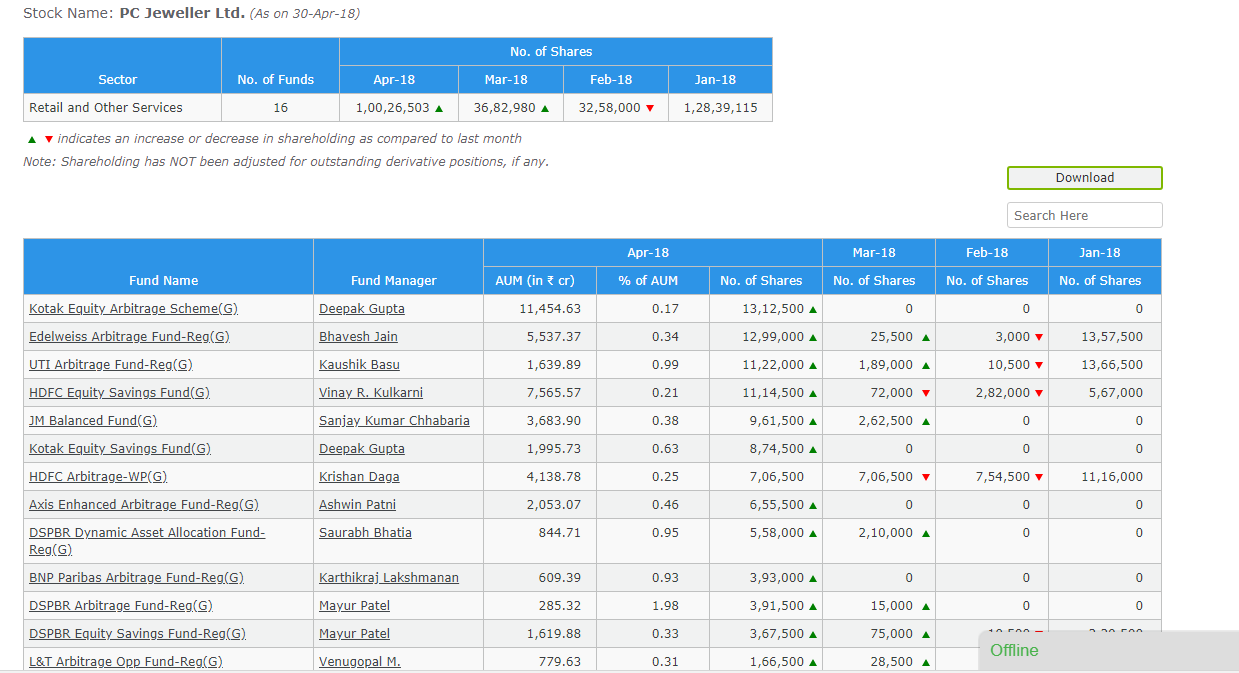

Just see the way mutual funds have aggressively bought PCJ in April 18. There holding has increased 3X !. While retail guys like us have been panicking and selling our holdings at a loss - MF have been buying it. Writing on the wall appears to be very clear now.

4 Likes

where can we find the above data. Please share us the source of the info

Most of them have arbitrage in their fund names i.e. just short term bet for them.

This one from valueresearchonline.com gives you overall picture. https://www.valueresearchonline.com/funds/comres.asp but won’t give you month wise.

Arbitrage schemes may have bought the stock in spot and sold it in future market for a small spread. So there is no risk for them if price goes down as future contract will be enforced.

3 Likes

If promoters have not increased their stake after such a massive fall , why anybody else should invest in the company?

1 Like

Promoters are increasing stake by not participating in buyback.

That’s true. But it is company’s money being used for buyback. I guess promoters are wealthy enough to have bought some shares on their own. The whole episode shows lack of confidence in promoters.

1 Like

In the PCJ Board meeting of May 10, they have announced the quantum and the price of the buy back. However, is there a time line within which the company has to complete the buy back process? Also, can the buy back offer be “withdrawn”? Would be great if someone can share SEBI guidelines ( I am assuming there would be some) for his area. Thx

Source of MF data: https://www.rupeevest.com/Mutual-Fund-Holdings/223032

PCJ employee cost is quite low = 1% of revenue. TITAN employee expense is close to 5% , that of Thangamayil Jewellery is nearly 2 % and for TBZ the figure is over 4%. Does this data say something. Its important in the context that PCJ has many company owned stores.

PC Jeweller posted flattish nos:

Profit up 7.3% : Rs 118.3 cr Vs Rs 110 cr (YoY)

Revenue (net sales) down 2.5% : Rs 2,103.2 cr Vs Rs 2,158.1 cr (YoY)

Segment wise breakdwon:

-Exports down ~45%: Rs. 302.76 cr vs Rs.551.93 cr (YoY)

-Domestic up ~12.5%: Rs.1,800.46 cr vs Rs.1,606.19 cr (YoY)

Details:

Guys, heard the con call for q4 2018. Management seems to have answered most of the questions we discussed in this forum for the last few months. I agree, one can say that it is still status quo, because one has to still trust the management’s word and it has not come out from a formal enquiry, but i feel they have given at least some confidence to the street.

They clarified the below points:

Interest payments: they gave a detailed breakdown of their debt tranches and corresponding interest rates. They have a significant off balance sheet debt “gold lease” ~3,000cr, which lead to 300cr. if annual interest

Why the promotors are not buying from the market, if they feel the co. is undervalued: admist voilent swings in share price, promotor’s direct buying might be preceived in a wrong light (~price manipulation). Despite showing interest in market purchase, the board decided for the buyback, which automatically inc. promotor’s stake

Also, they expressed confidence that the co. will complete the buyback soon

Why do they have 1,000+ cr. cash with 1,000+ cr debt. shouldn’t they repay the debt to save interest cost: they have excess cash now as they expect to grow using franchise model which does not require lot of wc debt, so they have decided to repay all the 1,000 cr of long term debt on the books in the next 3 months

They plan to open 30 stores in 2019, 90% of which will be on a franchise model

Drop in exports: due to crisis in middle east, and mainly due to vat/ import duty (or some other tax i cannot recall) in their main export markets

2% stake gifted to daughter in law

Why is the company not doing anything about the traders beating the stock heavily: the company has clarified to the investors and done their part, now it is the job of the exchange to take actions against the miscreants.

I might have missed out on some of the other important points, as i heard it on the go. Would appreciate if some of the seasoned VPs listen to the call and give their take on it

I expect a gap up opening on Monday and see at least some optimism around the company after the disclosures made in the concall and the investor presentation.

3 Likes

Can you please explain what is “off balance sheet debt “gold lease” ~3,000cr” ?

Hi, thanks for pointing out.

Actually, it is not off balance sheet. It is shown as trade payables worth 3,622 cr. as of q4 2018.

It is basically gold loan. Not 100% sure about this, but positive. Experienced guys can help clarify this.

So basically, we thought that the implied interest rate was too high ~30% as we did not consider a/c payables item in the denominator as usually it is non interest bearing liability. But in this case it is interest bearing as pointed out by the management and hence should be included. Actual implied interest rate is about10%, which seem normal.