There is no transparancy about how much will Axis Bank pay Paytm for this arrangement. Axis is getting a huge number of accounts with this, they are very likely to be paying a big sum

1 Like

Paytm is applying for Third Party Application Provider / TPAP license from NPCI which it is likely to get in time.

However, Paytm does not have Prepaid Payment Instrument / PPI and Payment Aggregator / PA licenses, which its competitor PhonePe has (and Google Pay?). These require approval from RBI. It may not be easy to get these licenses from RBI, considering its application for PA was already rejected.

Full list PA license holders: Reserve Bank of India - Database

If Paytm doesn’t get the PA license, then it can simply buy out an existing PA license holder and swap tech. Not all of them are anyways going to be successful.

3 Likes

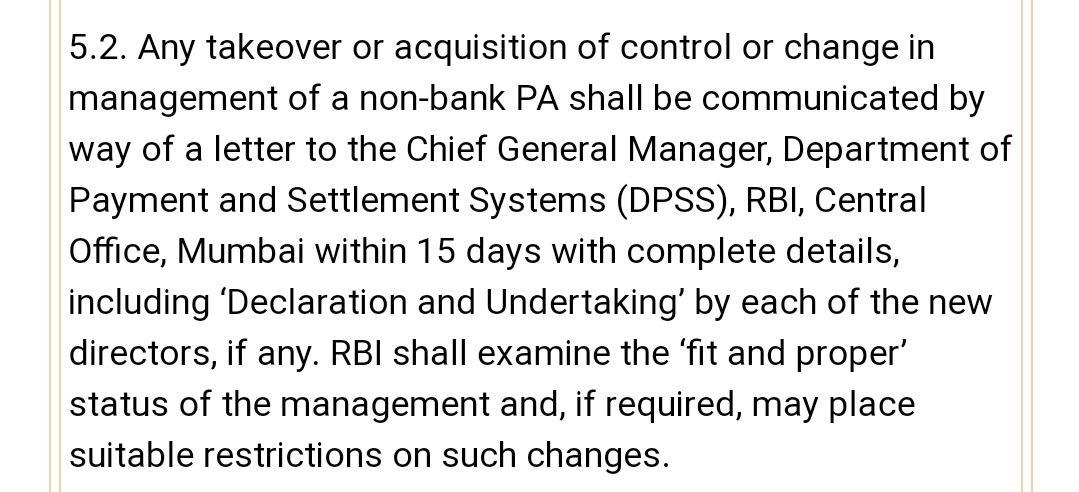

one cannot outright buy PA/PG license that easily as per RBI’s circular. attached notif.

link - Reserve Bank of India

1 Like

Very simply, the Paytm subsidiary that buys this PA co… will have to hire some senior leader from a major bank as “management”.

Tamal Bandyopadhyay, a seasoned banker and an excellent columnist, on Paytm-RBI saga.

I have just anecdotal evidence. I have not seen merchants switching from Paytm QR or soundbox till now. My guess is that the competition does not have enough soundboxes or salespeople to poach majority of merchants that Paytm serves. Paytm has 1.06 crore soundbox merchants. And Paytm manufactures the soundbox in India itself. Paytm even does all the software itself. In my opinion the major window which the competition had to spread misinformation was before the RBI FAQ came out. And even in that short window they did not have enough soundboxes or salespeople to deliver those soundboxes. But to be sure that this is happening we need to wait for more information from Paytm in its exchange filings .

Your understanding is correct in my opinion. The soundbox continues to work as is, only the bank account to which the money gets settled is changed.

5 Likes

(I flooded this thread with several of my posts already. But couldn’t help adding one more, due to the benefits of thinking in the open.)

This is the follow-up to my earlier assessment when there was much negativity about Paytm. My conclusions were mainly positive:

- The current crisis is temporary in nature.

- Paytm Payments Bank was the weakness, not strength. This weakness is going away.

- Execution skills is the real strength, which stays with the company.

Now, the negativity tide seems to be turning around. Tracking the situation brings in new perspectives.

I came across reports of Paytm management’s dealings with Ramesh Abhishek who is being investigated by CBI and ED. To be fair, Paytm was not the only company in question here. But Paytm Payments Bank’s role in relation with this, may imply that the management is/was bent on growth at any cost (GAAC), including providing kickbacks where required. This could partially explain, rather negatively, the execution skills alluded above.

Banker Tamal Bandyopadhyay, mentions the following in his column, which seems to confirm the GAAC mindset:

On many occasions, PPBL has allegedly submitted false compliance reports, fooling the regulator.

These are disturbing indeed. Is GAAC a strength or weakness for a fintech? I think it is a strength in the short term, but definitely weakness in the long term. The breakneck growth and eventual steep fall of Paytm Payments Bank is the striking proof.

At this juncture, as an investor with the long term mindset, the following are the key trackables:

WHAT MANAGEMENT DOES FROM HERE

For now, the management seems to have realized this lesson that GAAC does not help in the long run. Management now says that Paytm will make compliance as its top most priority.

Accordingly, they formed Group Advisory Committee on Compliance and Regulatory Matters. We can assume that they’re doing what they’re saying, at least for now.

In my opinion, this is a step in the right direction. We can assume that the likelihood of compliance is high in the future.

COMPLIANCE VS GROWTH

On the other hand, if this committee’s approval is required for each and every decision, which we in the tech circles deride as Committee-Driven Development, it could become the bottleneck for the company.

In my experience, the culture of agility is key for tech companies for innovation and growth. Having a compliance committee in itself is not a negative, actually positive. But the growth of Paytm is highly dependent on how this committee works without impacting the agility of the company.

REGULATORY EVOLUTION

Yet another aspect to keep in mind is: Regulation. It is double-edged. It could set things right, but it could also stifle innovation and ease of doing business.

RBI must have envisioned Payment Banks as tiny where the number of customers and transactions would be very small. In case of Paytm Payments Bank, I don’t think RBI had foreseen a payment bank becoming this big and significant so fast w.r.t number of customers and transactions.

It will be interesting to see how regulations evolve with respect to fintechs.

In the meantime,

- one would hope that Paytm management does not take shortcuts that could endanger the future of the company in the long term, once again

- another hope is whatever mitigation plan they have should not impede innovation and growth.

Disclosure: Invested. I always consider myself as a novice investor. No recommendations here. I welcome opposing views.

4 Likes

My conspiracy mind is perhaps working overtime.

Past few days paytm hitting UC

Then GS downgrades the stock and another round of panic selling follows

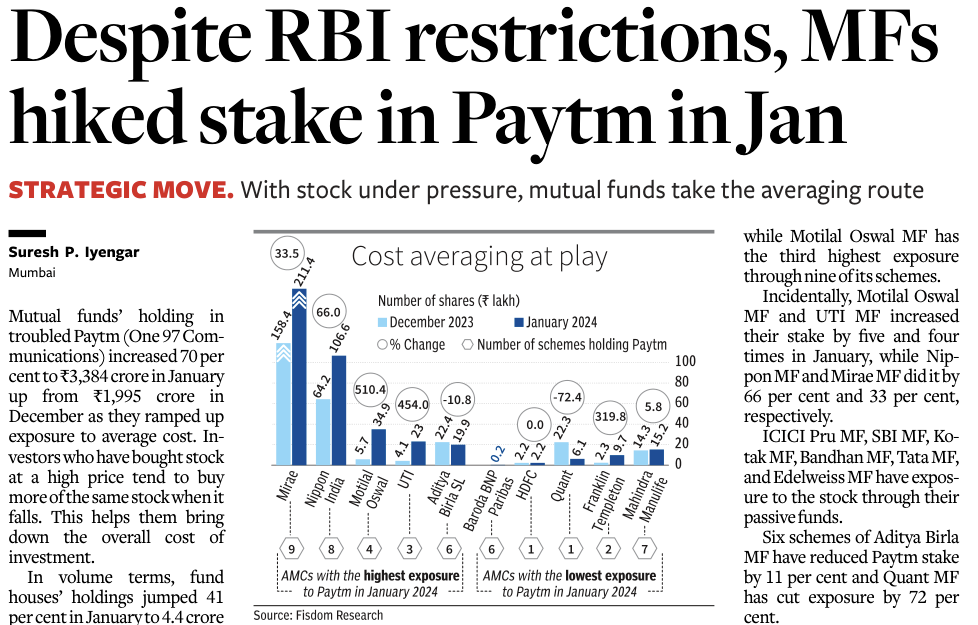

Now i find that many MFs are buying

1 Like

Hi. Which MF has bought? Any confirmed source of this news?

My suggestion is not to decide your buy and sell based on someone’s actions. It is a mistake. Do own analysis and take independent decisions.

All The Best.

PS: We never know why others are doing transactions.

5 Likes

Considering cash on the book I think paytm is here to stay.

In most segments it might not be no-1 but comes to close 2nd or third.

(-disc I use it as an all in one app → from stock investing to booking irctc tickets, hotels etc.)

In a country like India network effect plays for more than one player.

I always thought that paytm bank business is somewhat hampering it to reach larger audience - reason for lagging behind in UPI.

It has a vertical integration in gateway.

I see it as a holding company with many underlying businesses.

If everything is great why would market give you any opportunity.

This is my thought process.

Disc - caught the falling knife. Let’s see what will happen.

4 Likes

Why do you think Paytm bank was the reason for it lagging behind in upi

This was my thought process initially.

I was fundamentally against payment banks. PBs just stick to deposit taking and was not allowed to take any loans. Loans are assets for any financial company. Why would any company apply for such a license - many of those who applied withdrew. Also one97 comm holds stake in ppb and same time disbursing loans, cards etc. I saw blurriness in ppb and paytm. Being associated with ppb comes with significant restrictions to what a payment aggregator or what a UPI stack player can do. But I never thought RBI would do what it did. That is why I’m scared of banks and nbfcs (especially small ones). Though reasons may be kyc, etc. being a financial company and aspiring for aggressive growth certainly attracts more scrutiny from regulator. If any small mischief is seen you are punished.

1 Like

I would have considered ppb as strength if it was 100% subsidiary of one97 but shareholding itself was problem. There was certainly conflict of interest and this kind of structure would have been a problem sooner or later. Glad it happened earlier ( though i would have preferred ppb as 100% subsidiary of one97 ). Now i think there is no complexity with respect to structure, interest and hope VSS and team can focus on core strengths which is merchants loans and there are cherries on top like sound box subscription, ticketing, broking, insurance so on and so forth…

Having said that if RBI would have allowed to start opening ppb accounts and if ppb would have got small finance bank license in near that would have been a game changer (if this would have happened many people specially small merchants would have preferred to keep money in ppb. And that would been kind of moat to have many people in paytm ecosystem). But now this has zero chance of happening and as I said there was a conflict of interest and now VSS and team can focus on one business.

1 Like

2 Likes

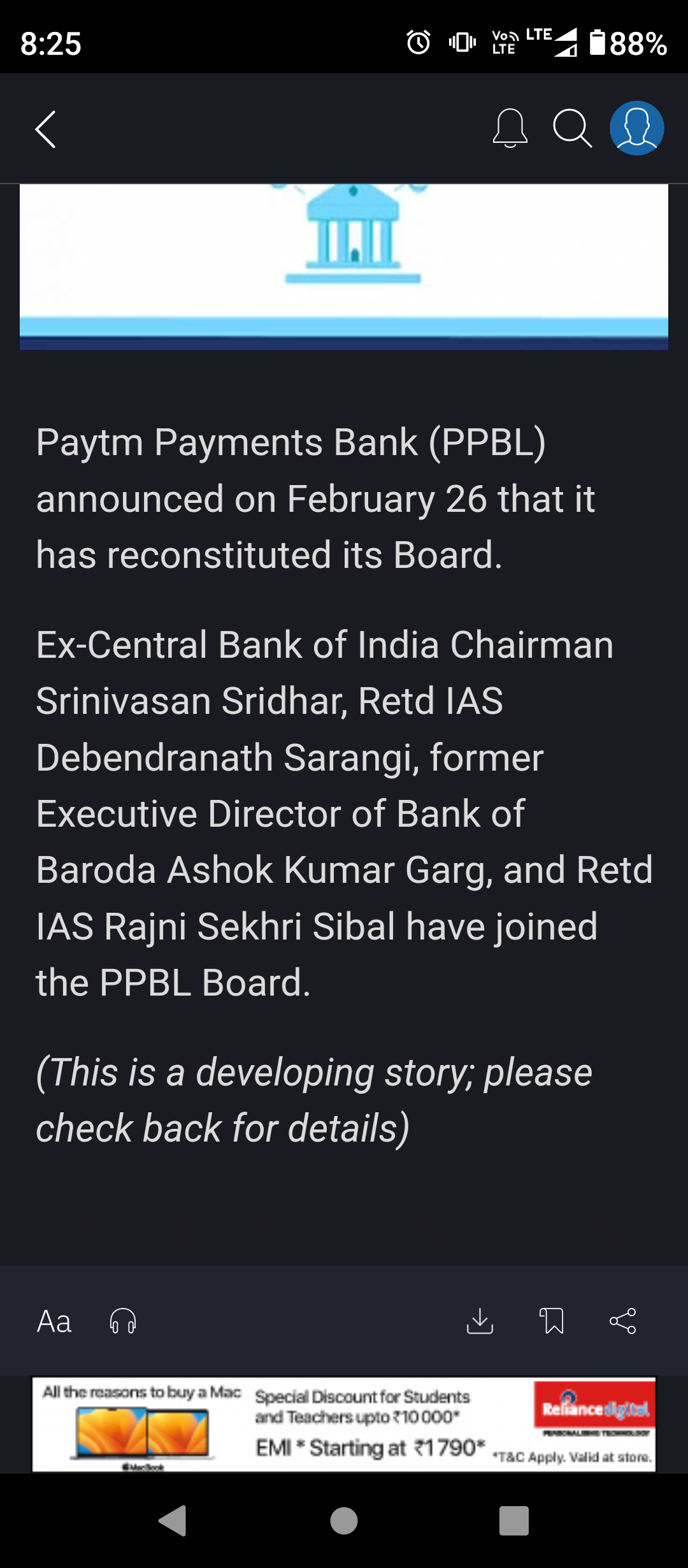

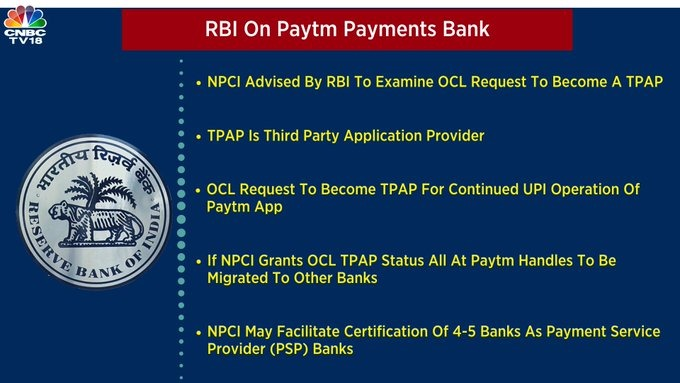

The above is a summary of this Press Release by RBI on “Additional Steps”: Reserve Bank of India - Press Releases

2 Likes